Answered step by step

Verified Expert Solution

Question

1 Approved Answer

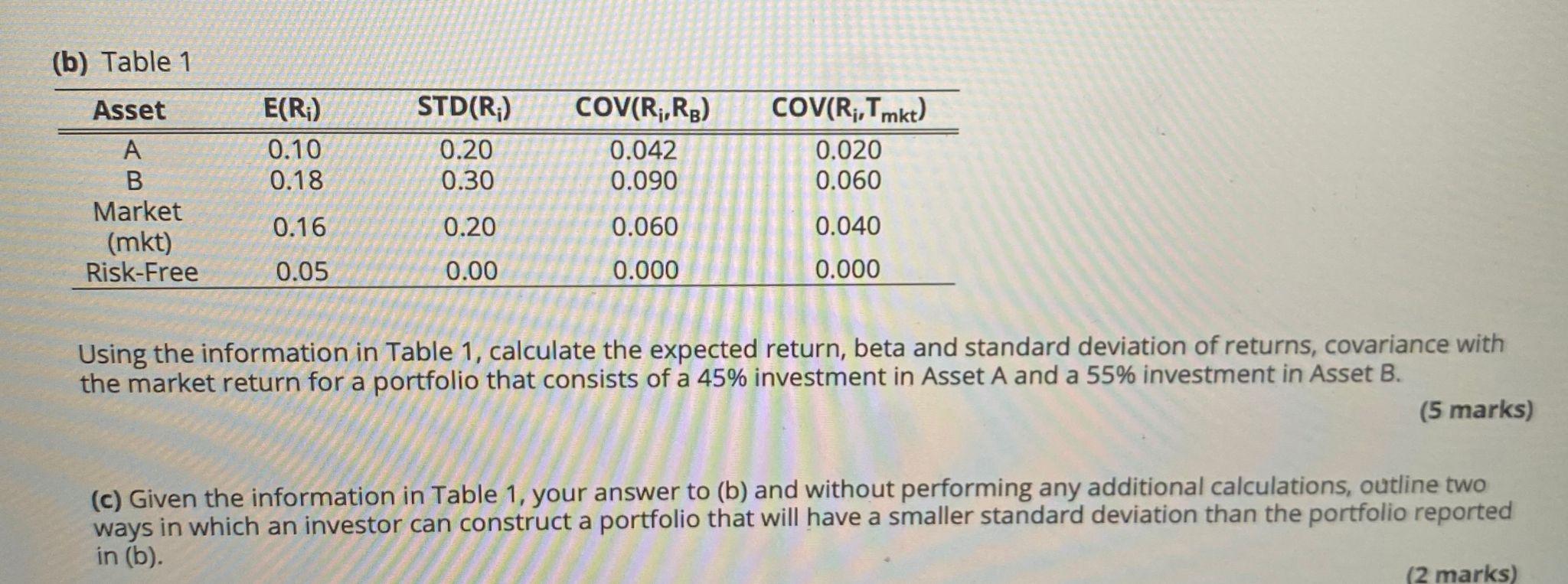

(b) Table 1 Asset E(R) STD(R) COV(R,RB) COV(Ri,Tmkt) 0.10 0.18 0.20 0.30 0.042 0.090 0.020 0.060 A B Market (mkt) Risk-Free 0.16 0.20 0.060 0.040

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

An Introduction to Investment Banks, Hedge Funds, and Private Equity

Authors: David P. Stowell

1st edition

978-0123745033, 0123745039, 978-9380931074