b. What are the significant differences in the cost structures of the three companies and why are they different? Financial Policy at Apple, 2013 (A)

b. What are the significant differences in the cost structures of the three companies and why are they different?

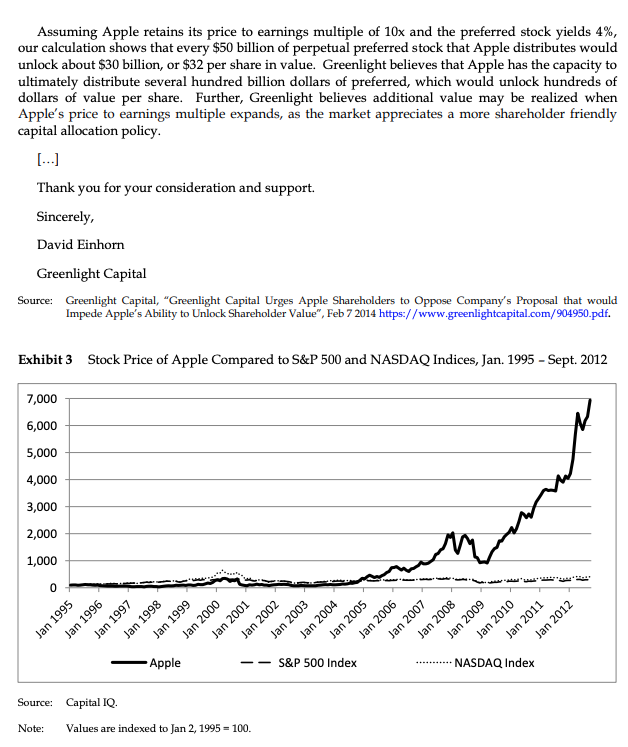

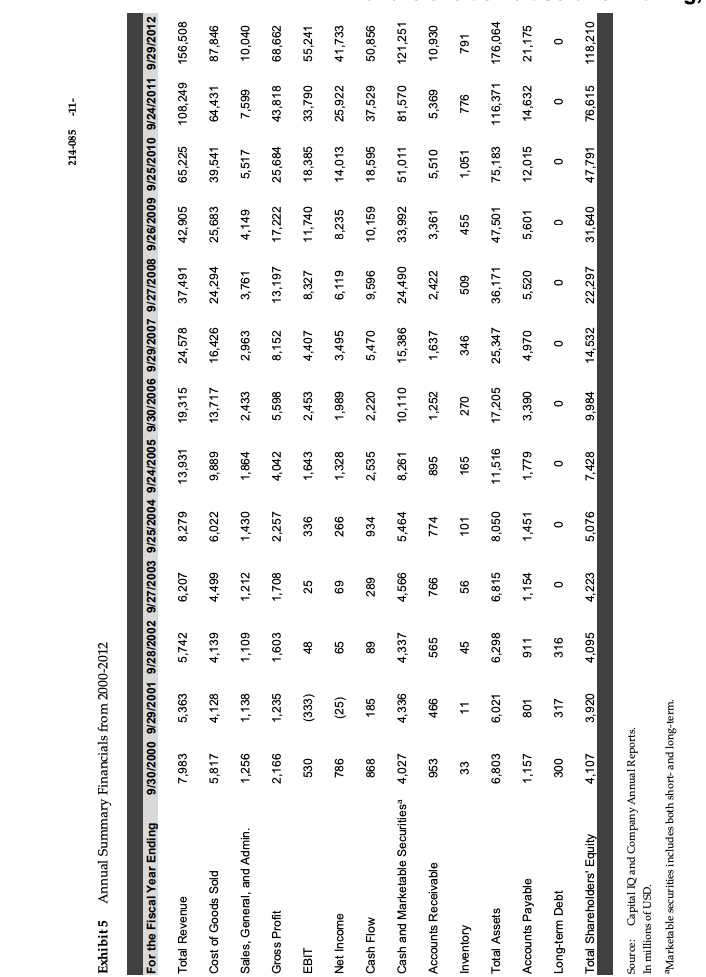

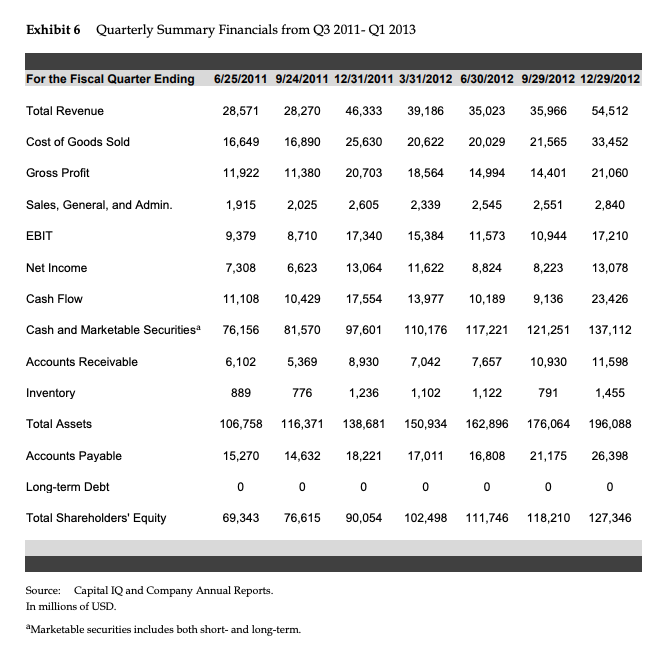

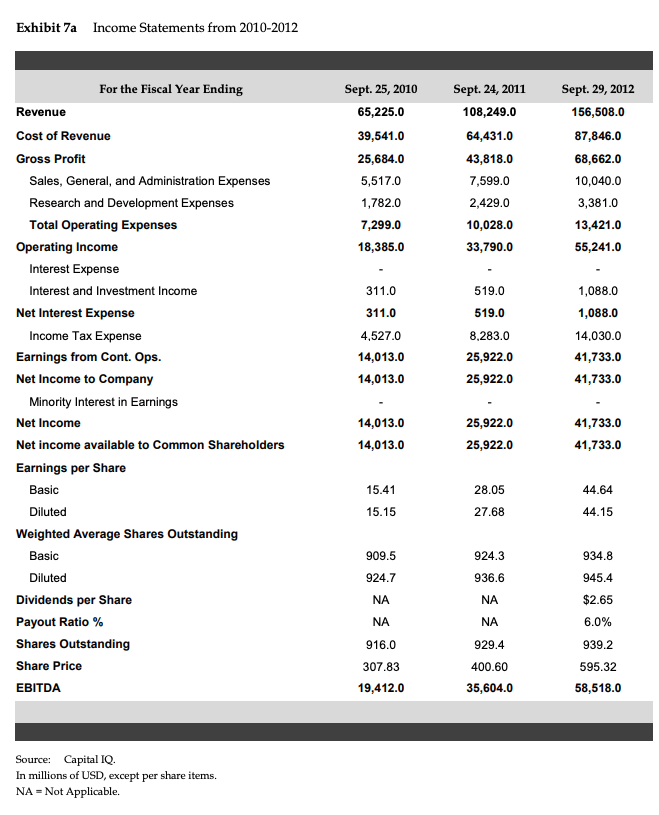

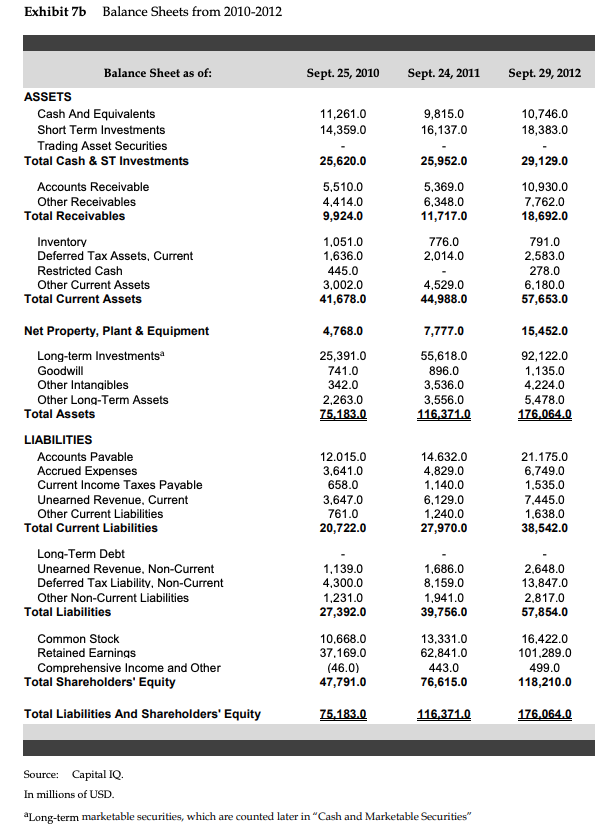

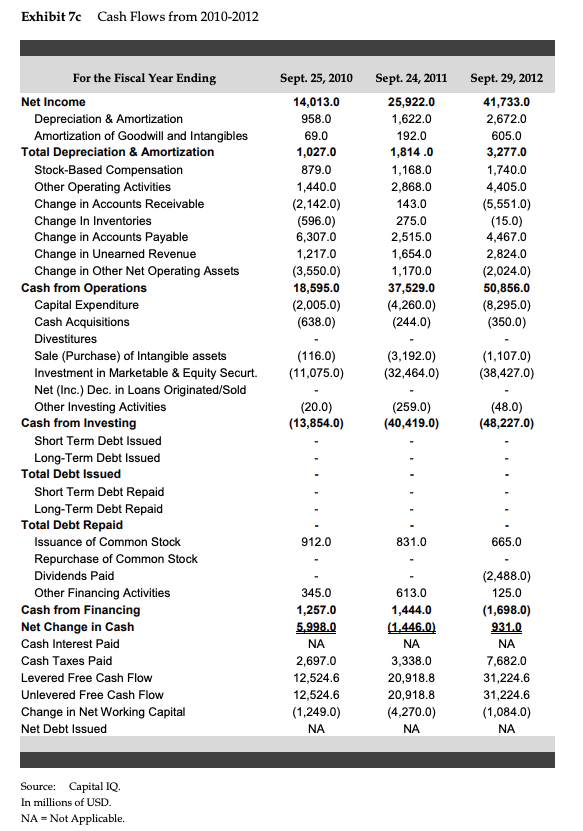

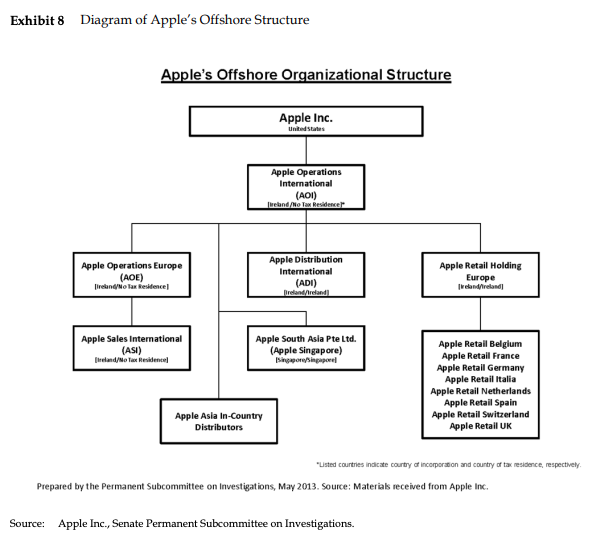

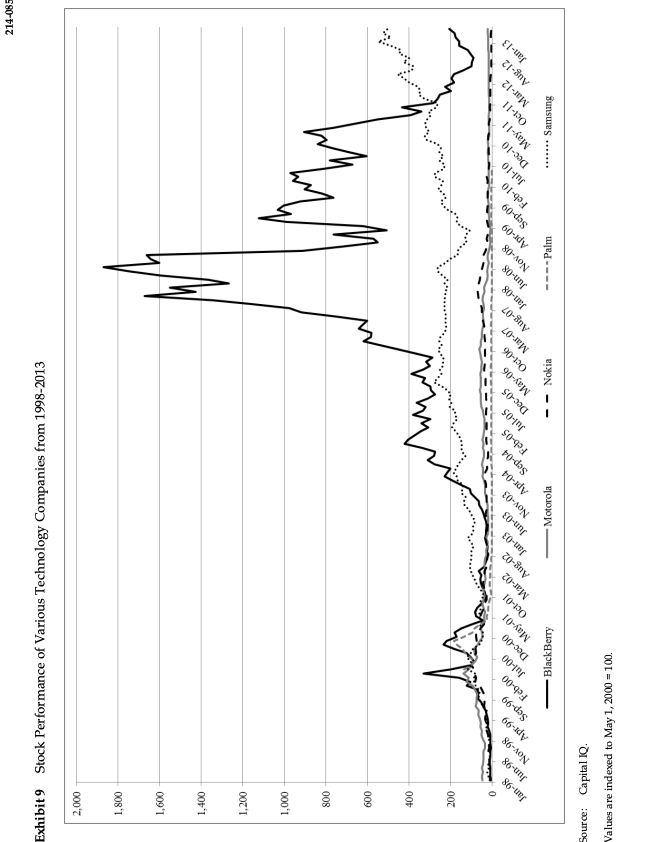

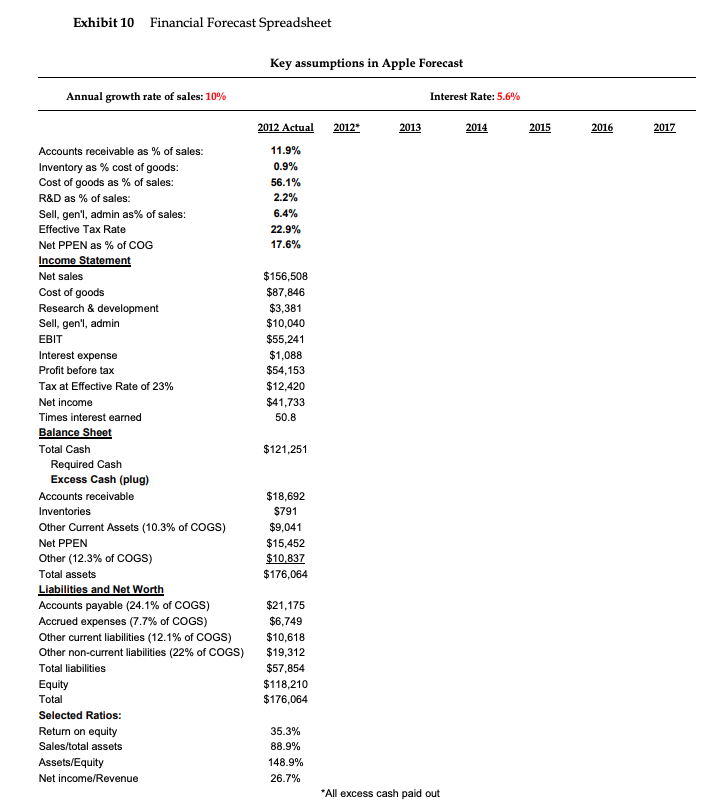

Financial Policy at Apple, 2013 (A) On April 12th 2013, Tim Cook, the CEO of Apple, and Peter Oppenheimer, the company's CFO, came together for a meeting in their Cupertino, California ofce. They had been confronting shareholder concerns over the level of cash Apple was holding and Apple's second-quarter press conference was less than two weeks away. Steve Jobs, the co~founder of Apple and its CEO from 1997 until 2011, had passed awayr only a year and a half prior and the pressure from stockholders to continue innovating was very high. They were particularly concerned about the amount of cash that Apple held, which amounted to 513? billion at Apple's first quarter filing, especially as Apple's stock price plummeted from a high ofjust over $700 in September to around $420 in April (see Exhibit '1 for Apple's recent stock price.)u David Einhorn, the president of Greenlight Capital, was fomenting the discontent of shareholders by voicing his belief that Apple should return most of its $13? billion in cash to the shareholders rather than let it sit unused. In particular, Einhorn had been pushing for a new class of preferred stock, which he dubbed \"iljrel',\" iat awarded holders $2 a year, or 50 cents per quarter.3 Einhorn's frustration with the matter had led him to sue Apple a few months prior for bundling a shareholder vote iat included a proposition to remove the company's ability to issue preferred stock (see Exhibit 2 fm excerpts of Eirllwrn's letter to the sharel'lolder's.)'1 This suit was ultimately dropped in March after Greenlight won an injunction and Apple withdrew the proposal. Cook and Oppenheimer had to make a decision about how to react to these cotncems. Should they begin to return more cash to the shareholders? If so, how much and through what method? They could issue a dividend, but were uncertain whether to issue a large special dividend or commit to one over time. They could authorize a share repurchase using some or all of their cash. They could also listen to Eirlhorrl's suggestion and issue preferred stock to each current stockholder. On die other hand, they could choose to keep their cash given the need to continue to invest in new technologies and the uncertainties of their product markets. To further complicate this situation, they also had to consider the fact that most of their cash was held overseas and could face a repatriation tax of up to 35% depending on the choice they made_5 A History of Apple6 Apple Computer was founded on April 1'\the first time, consumers could purchase digital versions of many of their favorite songs or albums in one place. These songs could be immediately synced to their iPods. Over the next several years, various versions of the ipod were released, some with huge storage capabilities, some designed without screens. Around this time, Steve Jobs was diagnosed with pancreatic cancer. He kept this news secret for quite some time, but underwent surgery in July 2004, appointing Tim Cook as his temporary replacement while he was on medical leave. When he returned, he immediately brought his attention to the success of the iPod. Since it accounted for 45% of Apple's revenue in 2005, it was important that they stay at the cutting edge. "The device that can eat our lunch is the cell phone," he remarked." While at first they tried to just modify the iPod, the scroll wheel was too difficult to use to make calls. Instead, they developed their well-known touch screen, which uses a technology called multi-touch. The iPhone was a huge success, with 270,000 units sold in the first thirty hours alone. 2 10 In 2008, Jobs' cancer returned; when he attended the launch of the iphone 3G in June, his physical appearance overshadowed the new product. Journalists and investors began to demand answers regarding his health. The company issued a response that he was just suffering from a common bug. Apple's stock price began to sink (see Exhibit 3 for Apple's long-run stock price.) In January 2009, Jobs took yet another medical leave. The cancer had spread to his liver and his health was deteriorating quickly. In March 2009, Jobs received a liver transplant, although the cancer had spread beyond his liver at this point and the doctors were pessimistic about his health. Jobs recovered, however, and returned to Apple in May. During the period Jobs was away, Apple's stock price recovered, and this made Jobs wonder exactly how important he was to the company now. Still, Jobs threw himself back into his work and was there to launch the iPad in January 2010. Apple's stock price began to soar. Revenues were up over 65% that fiscal year compared to the previous (see Exhibits 5-7 for financial data). One year later, the cancer returned. Jobs was forced to take his third medical leave in January 2011, leaving Tim Cook in charge again. This time, he would not return. On October 5th 2011, Steve Jobs passed away, leaving Tim Cook in charge as the new CEO of Apple. Apple since 2012 "How does one follow in the footsteps of a genius?" - Sam Gustin, regarding Steve Jobsll By late 2012, Apple shareholders and fanatics were growing restless, as no new groundbreaking devices had been launched since the iPad in 2010. The stock price had continued to decline from its high point in September 2012. Apple's market share in both the phone and tablet industries was steadily decreasing, mostly due to Android-powered devices. While Apple's cash had grown for the past decade, shareholders were starting to become concerned that Apple was not using it or returning it to the stockholders. But how did Apple get so much cash in the first place? Some attribute Apple's cash accumulation as "a living memorial to Steve Job's paranoia" but in reality the fact that Apple was able to amass so much so quickly is due to their high profitability, the reduction of product costs, and efficient management of Apple's capital structure. 12Apple's reluctance to return cash, 'l'im Cook claimed, was not because iey were concerned that shareholders would see it as a bad sign. He reassured shareholders that returning cash would not be r'waving a white flag on innovation."13 As Steve Jobs put it in Apple's Q4 2010 earnings call: We strongly believe that one or more very strategic opportunities may come along that we can take advantage - that we're in a unique position to take advantage of because of our strong cash position. 1 think, we've demonstrated a really strong track record of being very disciplined with the use of cash. We don't let it burn a hole in our pocket and we don't allow it to motivate us to do stupid acquisitions. So, I think that we'd like to continue to keep our powder dry because we do feel that there are one or more strategic opportunities in the future. That's the biggest reason. There is other reasons as well that we could go into but that's the biggest one.\" Some shareholst became frustrated by Apple's tight-vlipped approach to managing its excess cash, as evidenced by their quarterly earnings calls: Operator: Toni Sacconaghi, Sanford Bernstein. Toni Sacconaghi - Sanford Bernstein: Peter or Tim, I'd like to follow-up on your comment that you are actively discussing uses of cash. Is that any different, quite frankly, than what you've been doing historically or is that statement meant to suggest that you are thinking more constructively about cash than you have historically? Peter Oppenheimer - SVP and CFO: Toni, it's Peter. We have always discussed internally as a management team and with our Board our cash. We recognize that the cash is growing for all the right reasons and I would characterize our discussions today as active about what makes the most sense to do with the cash balance. We don't have anything to announce specically today. Toni Sacconaghi - Sanford Bernstein: Is there a timeframe or will you actually tell us that you've finished those discussions or is there a process for which there is an ending and you will inform us about that? Peter Oppenheimer - SVP and CFO: When we something to announce Tony, we will announce it, but I want to say again that we are actively discussing the best uses of our cash balance 1- --l Operator: Keith Bachman, Bank of Montreal. Keith Bachman - Bank of Montreal: Peter, to start with you, when you talked about the cash balances that you'll announce - something when you'll announce it, but could you give us a little perspective on how at least you're framing the differences, opportunities in terms of dividends and buybacks? Peter Oppenheimer - SVP and CFO: Keith, we're examining all uses of our cash balance, what we might do in a supply chain, what we can do from an acquisition perspective and otherwise. But I don't have any perspective to share with you today, specically on dividends or buybacks other than again, we are actively discussing the cash balance and in the meantime, we're not letting it burn a hole in our pocket.15 The United States government was also interested in Apple's cash management practices; they saw these cash levels as an example of a company abusing corporate tax law. The Senate Permanent Subcommittee on Investigations called Apple to testify in the second part of its hearing on Offshore Profit Shifting and the U.S. Tax Code. As Senator Carl Levin, the chairman of the hearing, commented: \"Apple wasn't satisfied with shifting its profits to a low-tax offshore tax haven. Apple sought the Holy Grail of avoidance. It has created offshore entities holding tens of billions of dollars, while claiming to be tax resident m1where."15 D'shore Cash Apple's global operations made their organizational structure multi-tiered (see Exhibit 5 for a diagram of Apple's offshore organization.) The majority of their cash was held in Ireland, which had a low corporate tax rate. In the United States, profits earned by American companies abroad are taxed but not until the money is repatriated to the United States. When it is repatriated, it is subject to a repatriation tax of the difference between the US. rate and local, foreign tax rates. If the foreign income was not taxed at all, this rate could be as high as 35%. Many American companies keep foreign prots abroad in response to these incentives. Considering that approximately 69% of Apple's cash is held abroad, a 35% repatriation tax on all of their foreign reserves would amount to just under one-quarter of their total cash reserves. In the United States. a company's tax residence is determined by where the company is based. This means that profits from Apple's foreign subsidiaries are not taxed by the United States government, :I'll.' are profits transferred from these subsidiaries to Apple's Irish subsidiaries. On the other hand, Ireland determines a company's tax residence based on where it is controlled. Since the Irish subsidiaries are run by executives in California, their profits are not taxed by the Irish government either. This means diat three of Apple's subsidiaries: ADI, ACE, and A51 do not have any tax residence.\" Apple executives maintained that these overseas divisions were a necessity due to Apple's vast overseas operations: 61% of Apple's revenues came from foreign earnings in 2012' while approximately 69% of all cash was held overseas.IS Despite complaints from the US. government, Apple maintained that it \" complies fully with both the laws and the spirit of die laws" and \"pays all its required taxes, both in dlis country and abroad."\" In fact, Apple fully supported changes to the corporate tax code, even ifit meant they'd end up paying more: Apple has always believed in the simple, not the complex. You can see it in our products and the way we conduct ourselves. It is in this spirit that we recorrunend a dramatic simplification of the corporate tax code. This reform should be revenue neutral, eliminate all corporate tax expenditures, lower corporate income tax rates and implement a reasonable tax on foreign earnings that allows the free flow of capital back to the US. We make this recommendation with our eyes wide open, realizing this would likely increase Apple's U.S. taxes. But we strongly believe such comprehensive reform would be fair to all taxpayers, would keep America globally competitive and would promote US. economic growth.\" According to Apple's testimony before the Senate, they were likely die largest corporate tax payer in the United States, paying $16 million per day. In other words, approximately $1 of every $40 of corporate income taxes collected by the US. Treasury in 2012 was paid by Apple. 2012 Share Repurchase Program In March 2012, Apple announced a quarterly dividend of $2.65 per share (a dividend yield of approocirnately 0.4% on the date the dividend was paid) along with a 3-year share repurchase plan of $10 billion. Peter Oppenheimer expected that the share repurchase program along with the dividends would cost Apple $45 billion in domestic cash for the first three years. This was the rst time Apple had authorized a dividend since 1995.21 Despite their efforts to boost shareholder confidence. Apple's stock price continued to fall from its high in September 2012, especially in relation to the NASDAQ index. Even with this program, several large and vocal stockholders were still unhappy. At the same time, Cook was aware of the volatile fortunes of predecessors to Apple, including Palm and Blackberryr (see Exhibit 9 for a graph of indexed technology stocks). iPrqf In February 2013, David Einhocrn, president of Greenlig'ht Capital, wrote an open letter to Apple shareholders demanding that Apple finally do something to \"unlock shareholder value" and stop Apple's cash hoard from growing at such a high rate.22 Einhorn had suggested a type of perpetual preferred stock, which Apple was trying to ban through a proxy provision A few weeks later, he gave a presentation on behalf of Greenlight Capital on this perpetual preferred stock, which he dubbed \"iPref.\" With Einhorn's method, Apple would issue five preferred shares per common share to all current shareholders. These preferred shares would each have a face value of $50 and would pay a 50 cent quarterly dividend. Einl'mrn was well aware of Apple's corporate tax conundrum and made sure that the cost of these dividends would be covered by free cash flow. Apple could issue ve iPrefs per common share without having to spend any of their cash reserves. Einhom estimated that this iPref distribution of five iPrefs per share would urIlDCk $150 of value for each share, or approximately 33% of the Q1 2013 stock price of WEED. Einhorn claimed that this was higher than the value unlocked from either a share repurchase program or a special dividend, even when all excess cash was used in either program. Unlike a share repurchase or dividend, the iPref would solve the repatriation problem since only free cash flows would be used. With approximately 939.1 million shares outstanding in Q1 2013, the program would cost approocimately $9.4 billion dollars for the first year. The proxyr proposal, Proposal 2, whid'l would limit Apple's ability to issue preferred stock. was blocked by a judge due to a separate issue, meaning that Einhom's suggestion was still a possible solution to Apple's problem.B Conclusion Apple held the largest cash reserves of any non-financial institution. The next largest cash reserve held by a non-nancial institution was Microsoft, which had just over half the amount Apple did.24 Cook and Oppenheimer had to nd a solution that would please shareholders but would also leave the company room to ilu'lovate. Cook and Oppenheimer rst had to decide whether to return any money to shareholders, and if so, how much. In order to do so, Cook and Oppenheimer began by creating a nancial forecast to see how much cash Apple would accumulate in five years if they had returned it all in 2012 (see Exhibit 10 for the financial forecast spreadsheet). They were a little weary about Einhorn's calculations regarding dividends. repurchases. and iPref and decided to try the calculations themselves. With such a large amount of cash and the pressure it was generating, Cook and Oppenheimer were reminded that high-class problems were still problems. nominal share repurchase program, we believe that there is much more that the Board should do for shareholders. We believe that it is important for shareholders to send Apple's Board the message that the current capital allocation policy is not satisfactory, and that after considering all options, Apple's Board should act to unlock the latent value of Apple's balance sheet and franchise. If you share our frustration, please join us in blocking Hie Companfs effort to restrict its value creation options by voting AGAINST Apple's plan to amend its corporate charter in Proposal 2 to eliminate preferred stock. Send Apple And Its Board A Message That We Want Apple to Change Its Capital Allocation Policy To Unlock Value For Shareholders - VOTE AGAINST PROPOSAL 2 At a May 2912 investlnent corlference, Greenlight introduced the idea that Apple could unlock several hundred billion dollars of shareholder value by distributing to existing shareholders a perpetual preferred stock. Since then, Greerllight has had discussions with Apple encouraging the Company to distribute perpetual preferred stock as an innovative method of rewarding all shareholders for the Company's strong balance sheet and substantial cash flows. Put plainly, Greenlight is encouraging Apple to distribute a perpetual, high-yielding preferred stock direcy to shareholders at no cost. This would enable shareholders to own and separately trade the new preferred shares and Apple's existing common shares. Importantly, Greenlight believes these preferred shares represent a simple, low-risk way to reward shareholders without compromising the financial and strategic flexibility of the Company, or forcing the company to incur tax on repatriating its offshore cash balances. Greenlight suggested an initial preferred share distribution, whereby dividends could be funded on an ongoing basis by a relatively small percentage of die Company's operating cash flow. Apple rejected the idea outright in September 2012. Yesterday, after Greenlight notified Apple of its intention to vote against Proposal 2, Apple said it would reconsider the idea, but refused to withdraw the proxy provision where Apple seeks to eliminate preferred stock from its charter. The recent, severe under-performance of Apple's shares, which are down approximately 35% from their peak valuation, underscores the need for the Company to apply the same level of creativity used to develop revolutionary technology for its consumers to unlock the value of its strong balance sheet for its shareholders. We believe our suggestion of distributing perpetual preferred stock, while innovative, is also quite simple. Apple could distribute high-yielding, tax efcient preferred stock to existing shareholders at no cost. This new type of easily tradable preferred security would allow Apple to take advantage of the market's appetite for yield while preserving future operating and strategic exibility. lmportantly, we believe this strategy would require no immediate use of cash other than the ongoing dividend, and would not pose any maturity, re-financing, balance sheet, or default risk. For example, Apple could initially distribute to existing shareholders $50 billion of perpetual preferred stock, with a 4% annual cash dividend paid quarterly at preferential tax rates. Once a trading market is established and the market recognizes the attractiveness of a highly liquid, steady yielding instrument from an issuer backed by Apple's unmatched balance sheet and valuable franchise, the Board could evaluate unlocking additional value by distributing additional perpetual preferred stock to existing shareholders. With this conservative action, Greerllight believes the Board could unlock hundreds of billions of dollars of latent shareholder value. Assuming Apple retains its price to earnings multiple of 10x and the preferred stock yields 4%, our calculation shows that every $50 billion of perpetual preferred stock that Apple distributes would unlock about $30 billion, or $32 per share in value. Greenlight believes that Apple has the capacity to ultimately distribute several hundred billion dollars of preferred, which would unlock hundreds of dollars of value per share. Further, Greenlight believes additional value may be realized when Apple's price to earnings multiple expands, as the market appreciates a more shareholder friendly capital allocation policy. [...] Thank you for your consideration and support. Sincerely, David Einhorn Greenlight Capital Source: Greenlight Capital, "Greenlight Capital Urges Apple Shareholders to Oppose Company's Proposal that would Impede Apple's Ability to Unlock Shareholder Value", Feb 7 2014 https://www.greenlightcapital.com/904950.pdf. Exhibit 3 Stock Price of Apple Compared to S&P 500 and NASDAQ Indices, Jan. 1995 - Sept. 2012 7,000 6,000 5,000 4,000 3,000 2,000 1,000 001 2006 Jan 1995 Jan 1997 Jan 1998 Jan 1999 Jan 20 Jan 2002 Jan 2003 Jan 2004 Jan 2005 Jan 2007 Jan 2008 Jan 2009 an 2010 Jan 2011 an 2012 Jan Apple S&P 500 Index "-" NASDAQ Index Source: Capital IQ. Note: Values are indexed to Jan 2, 1995 = 100.214-085 -11- Exhibit5 Annual Summary Financials from 2000-2012 For the Fiscal Year Ending 9/30/2000 9/29/2001 9/28/2002 9/27/2003 9/25/2004 9/24/2005 9/30/2006 9/29/2007 9/27/2008 9/26/2009 9/25/2010 9/24/2011 9/29/2012 Total Revenue 7,983 5,363 5,742 6,207 8,279 13,931 19,315 24,578 37,491 42,905 65,225 108,249 156,508 Cost of Goods Sold 5,817 4, 128 4,139 4,499 6,022 9,889 13,717 16,426 24,294 25,683 39,541 64,431 87,846 Sales, General, and Admin. 1,256 1, 138 1,109 1,212 1,430 1,864 2,433 2,963 3,761 4,149 5,517 7,599 10,040 Gross Profit 2,166 1,235 1,603 1,708 2,257 4,042 5,598 8,152 13,197 17,222 25,684 43,818 68,662 EBIT 530 (333) 336 1,643 2,453 4,407 8,327 11,740 18,385 33,790 55,241 Net Income 786 (25) 266 1,328 1,989 3,495 6, 119 8,235 14,013 25,922 41,733 Cash Flow 868 185 289 934 2,535 2,220 5,470 9,596 10, 159 18,595 37,529 50,856 Cash and Marketable Securities* 4,027 4,336 4,337 4,566 5,464 8,261 10,1 10 15,386 24,490 33,992 51,011 81,570 121,251 Accounts Receivable 953 466 565 766 774 895 1,252 1,637 2,422 3,361 5,510 5,369 10,930 Inventory 56 101 165 270 346 509 455 1,051 776 791 Total Assets 6,803 6,021 6,298 6,815 8,050 11,516 17,205 25,347 36,171 47,501 75,183 116,371 176,064 Accounts Payable 1,157 801 911 1,154 1,451 1,779 3,390 4,970 5,520 5,601 12,015 14,632 21,175 O Long-term Debt 300 317 316 Total Shareholders' Equity 4,107 3,920 4.095 4.223 5,076 7,428 9.984 14,532 22,297 31,640 47,791 76,615 118,210 Source: Capital IQ and Company Annual Reports. In millions of USD "Marketable securities includes both short- and long-term.Exhibit 6 Quarterly Summary Financials from Q3 2011- Q1 2013 For the Fiscal Quarter Ending 6/25/2011 9/24/2011 12/31/2011 3/31/2012 6/30/2012 9/29/2012 12/29/2012 Total Revenue 28,571 28,270 46,333 39,186 35,023 35,966 54,512 Cost of Goods Sold 16,649 16,890 25,630 20,622 20,029 21,565 33,452 Gross Profit 11,922 11,380 20,703 18,564 14,994 14,401 21,060 Sales, General, and Admin. 1,915 2.025 2,605 2.339 2,545 2,551 2,840 EBIT 9,379 8,710 17,340 15,384 11,573 10,944 17,210 Net Income 7,308 6,623 13,064 11,622 8,824 8,223 13,078 Cash Flow 11,108 10,429 17,554 13,977 10,189 9,136 23,426 Cash and Marketable Securities 76,156 81,570 97,601 110,176 117,221 121,251 137,112 Accounts Receivable 6,102 5,369 8,930 7,042 7,657 10,930 11,598 Inventory 889 776 1,236 1,102 1,122 791 1,455 Total Assets 106,758 116,371 138,681 150,934 162,896 176,064 196,088 Accounts Payable 15,270 14,632 18,221 17,011 16,808 21,175 26,398 Long-term Debt 0 0 0 0 0 Total Shareholders' Equity 69,343 76,615 90,054 102,498 111,746 118,210 127,346 Source: Capital IQ and Company Annual Reports. In millions of USD. "Marketable securities includes both short- and long-term.Exhibit 7a Income Statements from 2010-2012 For the Fiscal Year Ending Sept. 25, 2010 Sept. 24, 2011 Sept. 29, 2012 Revenue 65,225.0 108,249.0 156,508.0 Cost of Revenue 39,541.0 64,431.0 87,846.0 Gross Profit 25,684.0 43,818.0 68,662.0 Sales, General, and Administration Expenses 5,517.0 7,599.0 10,040.0 Research and Development Expenses 1,782.0 2,429.0 3,381.0 Total Operating Expenses 7,299.0 10,028.0 13,421.0 Operating Income 18,385.0 33,790.0 55,241.0 Interest Expense Interest and Investment Income 311.0 519.0 1,088.0 Net Interest Expense 311.0 519.0 1,088.0 Income Tax Expense 4.527.0 8.283.0 14.030.0 Earnings from Cont. Ops. 14,013.0 25,922.0 41,733.0 Net Income to Company 14,013.0 25,922.0 41,733.0 Minority Interest in Earnings Net Income 14,013.0 25,922.0 41,733.0 Net income available to Common Shareholders 14,013.0 25,922.0 41,733.0 Earnings per Share Basic 15.41 28.05 44.64 Diluted 15.15 27.68 44.15 Weighted Average Shares Outstanding Basic 909.5 924.3 934.8 Diluted 924.7 936.6 945.4 Dividends per Share NA NA $2.65 Payout Ratio % NA NA 6.0% Shares Outstanding 916.0 929.4 939.2 Share Price 307.83 400.60 595.32 EBITDA 19,412.0 35,604.0 58,518.0 Source: Capital IQ. In millions of USD, except per share items. NA = Not Applicable.Exhibit 7b Balance Sheets from 2010-2012 Balance Sheet as of: Sept. 25, 2010 Sept. 24, 2011 Sept. 29, 2012 ASSETS Cash And Equivalents 11,261.0 9,815.0 10,746.0 Short Term Investments 14,359.0 16,137.0 18,383.0 Trading Asset Securities Total Cash & ST Investments 25,620.0 25,952.0 29,129.0 Accounts Receivable 5.510.0 5,369.0 10,930.0 Other Receivables 4,414.0 6,348.0 7.762.0 Total Receivables 9,924.0 11,717.0 18,692.0 Inventory 1,051.0 776.0 791.0 Deferred Tax Assets, Current 1,636.0 2.014.0 2.583.0 Restricted Cash 445.0 278.0 Other Current Assets 3,002.0 4.529.0 6.180.0 Total Current Assets 41,678.0 44,988.0 57,653.0 Net Property, Plant & Equipment 4,768.0 7,777.0 15,452.0 Long-term Investments 25,391.0 55,618.0 92,122.0 Goodwill 741.0 896.0 1.135.0 Other Intangibles 342.0 3,536.0 4.224.0 Other Long-Term Assets 2,263.0 3,556.0 5,478.0 Total Assets 75,183.0 116,371.0 176,064.0 LIABILITIES Accounts Pavable 12.015.0 14.632.0 21.175.0 Accrued Expenses 3.641.0 4.829.0 6.749.0 Current Income Taxes Payable 658.0 1.140.0 1.535.0 Unearned Revenue. Current 3,647.0 6,129.0 7.445.0 Other Current Liabilities 761.0 1,240.0 1.638.0 Total Current Liabilities 20,722.0 27,970.0 38,542.0 Long-Term Debt Unearned Revenue. Non-Current 1.139.0 1,686.0 2.648.0 Deferred Tax Liability, Non-Current 4,300.0 8, 159.0 13.847.0 Other Non-Current Liabilities 1,231.0 1,941.0 2.817.0 Total Liabilities 27,392.0 39,756.0 57,854.0 Common Stock 10.668.0 13.331.0 16.422.0 Retained Earnings 37.169.0 62.841.0 101.289.0 Comprehensive Income and Other (46.0) 443.0 499.0 Total Shareholders' Equity 47,791.0 76,615.0 118,210.0 Total Liabilities And Shareholders' Equity 75,183.0 116.371.0 176,064.0 Source: Capital IQ. In millions of USD. "Long-term marketable securities, which are counted later in "Cash and Marketable Securities"Exhibit 7'1: Cash Flows from 2010-2012 For the Fiscal Year Ending Net Income Depreciation 3. Amortization Amortization of Goodwill and Intangibles Total Depreciation S Amortization Stock-Based Compensation Other Operating Activities Change in Accounts Receivable Change In Inventories Change in Accounts Payable Change in Unearned Revenue Change in Other Net Operating Assets Cash from Operations Capital Expenditure Cash Acquisitions Divestilures Sale (Purchase) of Intangible assets Investment in Marketable & Equity Securt. Net (Inc) Dec. in Loans OriginalediSold Other Investing Activities Cash from Investing Short Term Debt Issued Long-Term Debt Issued Total Debt Issued Short Term Debt Repaid Long-Term Debt Repaid Total Debt Repaid Issuance of Common Stock Repurchase of Common Stock Dividends Paid Other Financing Activities Cash from Financing Net Change in Cash Cash Interest Paid Cash Taxes Paid Levered Free Cash Flow Unlevered Free Cash Flow Change in Net Working Capital Net Debt Issued Sept. 15, 2010 14,0150 953.0 59.0 1,027.0 579.0 1,440.0 (2,142.01 (595.0} 5,507.0 1,217.0 (5,550.0) 13,5950 (2,005.01 (533.01 (115.01 (1 1,075.01 (20.01 (13,354.01 NA 2,597.0 12,5245 12,5245 (1,249.01 NA 551,524,201: 25,9220 1 ,5220 192.0 1,514 .0 1 ,1 55.0 2,355.0 143.0 275.0 2,515.0 1 ,5540 1 ,1 70.0 37,5290 (4,250.01 (244.01 (5,1 92.01 (32,454.01 (259.01 (40,410.01 NA 3,333.0 20 .91 8. 5 20 .91 8. 5 (4,2?00] MA 55111. 29, 2012 41,7330 2,572.0 505.0 3,277.0 1 ,7400 4,405.0 (5,551 .01 (15.0} 4,457.0 2,324.0 (2,024.01 50,5550 (5,295.01 (350.01 (1 ,107.01 (55,427.01 (43.01 (45,227.01 555.0 (2,455.01 125.0 (1 ,59501 NA 7,552.0 51.2245 51.2245 (1 ,05401 NA Source: Capital IQ. In millions of USD. NA = Not Applicable. Exhibit 8 Diagram of Apple's Offshore Structure Apple's Offshore Organizational Structure Apple Inc. United states Apple Operations International (AOI) chand /Wo Tan Residence] Apple Distribution Apple Operations Europe Apple Retail Holding International (AOE) Europe (ADI) Dredand findand Apple Sales International Apple South Asla Pte Ltd. Apple Retail Belgium (ASI (Apple Singapore) Iucland/No Tax Residentel SingaporeySingaporel Apple Retail France Apple Retail Germany Apple Retail Italia Apple Retail Netherlands Apple Retail Spain Apple Asla In-Country Apple Retail Switzerland Distributor Apple Retail UK "Listed countries indicate country of incorporation and country of tax residence, respectively. Prepared by the Permanent Subcommittee on Investigations, May 2013. Source: Materials received from Apple Inc. Source: Apple Inc., Senate Permanent Subcommittee on Investigations.2,000 008'T 009'T 1,400 1,200 Exhibit 9 Stock Performance of Various Technology Companies from 1998-2013 OOD'I 008 009 QOF 007 Jan~98 Jun-98 Nov-98 ource: Capital IQ. Apr-99 Sep-99 Feb.00 Jul-00 'alues are indexed to May 1, 2000 = 100. Dec.00 - BlackBerry May-01 Oct-01 Mar-02 Aug-02 Jan-03 Jun-03 Nov-03 214-085 Motorola Apr-04 Sep-04 Feb-05 Jul-OS May Oct~ BLYON Mar-07 Aug-07 Jan-08 Jun-08 Nov-08 Apr-09 Sep-09 Feb-10 Jul-10 Dec-10 May-1 1 Oct-11 Runsties ....... Mar-12 Aug-12 Jan-13Exhibit 10 Financial Forecast Spreadsheet Key assumptions in Apple Forecast Annual growth rate of sales: 10% Interest Rate: 5.6% 2012 Actual 2012* 2013 2014 2015 2016 2017 Accounts receivable as % of sales: 11.9% Inventory as % cost of goods 0.9% Cost of goods as % of sales: 56.1% R&D as % of sales: 2.2% Sell, gen'l, admin as% of sales: 6.4% Effective Tax Rate 22.9% Net PPEN as % of COG 17.6% Income Statement Net sales $156,508 Cost of goods $87,846 Research & development $3,381 Sell, gen'l, admin $10,040 EBIT $55,241 Interest expense $1,088 Profit before tax $54,153 Tax at Effective Rate of 23% $12,420 Net income $41,733 Times interest earned 50.8 Balance Sheet Total Cash $121,251 Required Cash Excess Cash (plug) Accounts receivable $18,692 Inventories $791 Other Current Assets (10.3% of COGS) $9,041 Net PPEN $15,452 Other (12.3% of COGS) $10.837 Total assets $176,064 Liabilities and Net Worth Accounts payable (24.1% of COGS) $21,175 Accrued expenses (7.7% of COGS) $6,749 Other current liabilities (12.1% of COGS) $10,618 Other non-current liabilities (22% of COGS) $19,312 Total liabilities $57,854 Equity $118,210 Total $176,064 Selected Ratios: Retum on equity 35.3% Sales/total assets 88.9% Assets/Equity 148.9% Net income/Revenue 26.7% "All excess cash paid out

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance