Question

b. Write a persuasive note convincing all production department staff at Becko Ltd of the value of ABB over their traditional method of setting a

b. Write a persuasive note convincing all production department staff at Becko Ltd of the value of ABB over their traditional method of setting a budget. As part of your answer you need to specifically refer to your table in (a) above to reinforce your argument. (10 marks)

Q from Chegg website:-

becko-ltd-production-department-

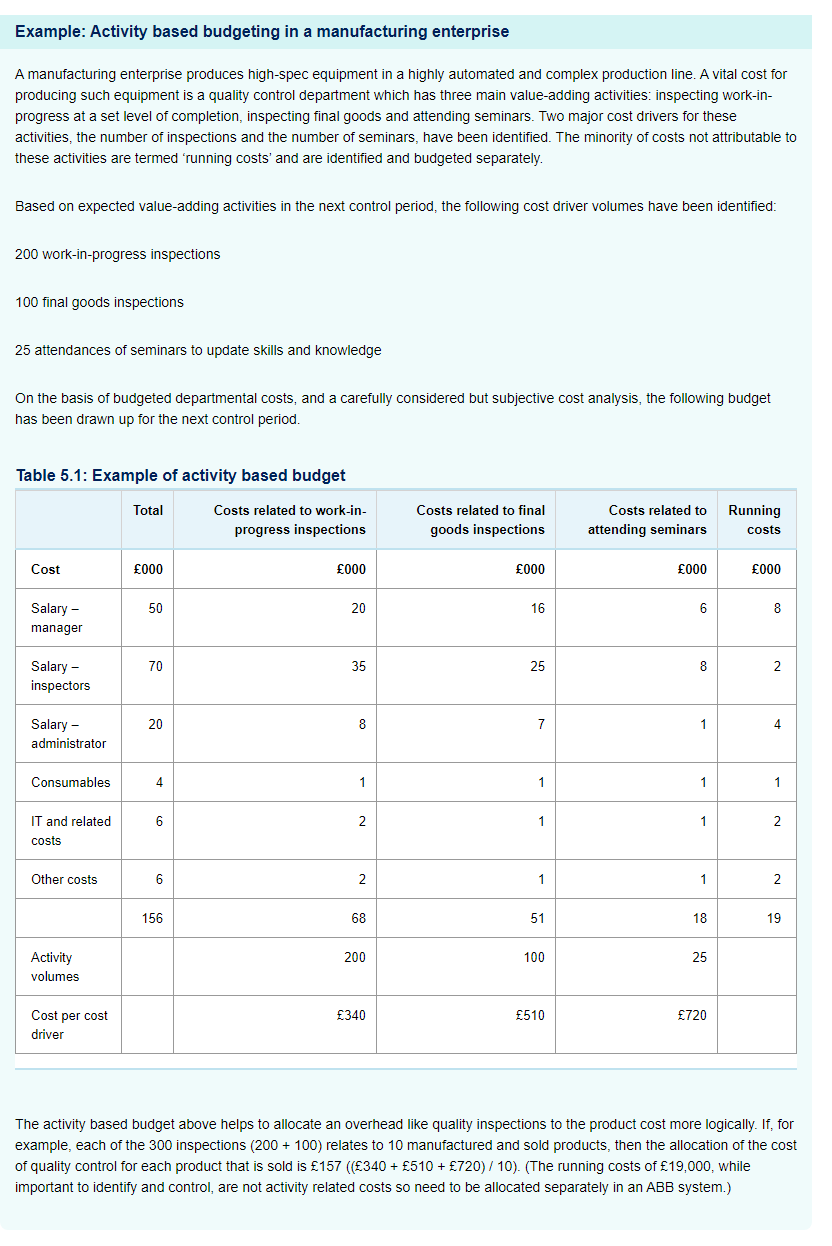

Example: Activity based budgeting in a manufacturing enterprise A manufacturing enterprise produces high-spec equipment in a highly automated and complex production line. A vital cost for producing such equipment is a quality control department which has three main value-adding activities: inspecting work-in- progress at a set level of completion, inspecting final goods and attending seminars. Two major cost drivers for these activities, the number of inspections and the number of seminars, have been identified. The minority of costs not attributable to these activities are termed running costs' and are identified and budgeted separately. Based on expected value-adding activities in the next control period, the following cost driver volumes have been identified: 200 work-in-progress inspections 100 final goods inspections 25 attendances of seminars to update skills and knowledge On the basis of budgeted departmental costs, and a carefully considered but subjective cost analysis, the following budget has been drawn up for the next control period. Table 5.1: Example of activity based budget Total Costs related to work-in- progress inspections Costs related to final goods inspections Costs related to attending seminars Running costs Cost 000 000 000 000 000 50 20 16 6 8 Salary - manager 70 35 25 8 2 2 Salary - inspectors 20 8 7 1 4 Salary - administrator Consumables 4 1 1 1 1 6 2 1 1 2 IT and related costs 2 Other costs 6 2 1 1 2. 156 68 51 18 19 200 100 25 Activity volumes 340 510 720 Cost per cost driver The activity based budget above helps to allocate an overhead like quality inspections to the product cost more logically. If, for example, each of the 300 inspections (200 + 100) relates to 10 manufactured and sold products, then the allocation of the cost of quality control for each product that is sold is 157 ((340 + 510 + 720)/10). (The running costs of 19,000, while important to identify and control, are not activity related costs so need to be allocated separately in an ABB system.) Example: Activity based budgeting in a manufacturing enterprise A manufacturing enterprise produces high-spec equipment in a highly automated and complex production line. A vital cost for producing such equipment is a quality control department which has three main value-adding activities: inspecting work-in- progress at a set level of completion, inspecting final goods and attending seminars. Two major cost drivers for these activities, the number of inspections and the number of seminars, have been identified. The minority of costs not attributable to these activities are termed running costs' and are identified and budgeted separately. Based on expected value-adding activities in the next control period, the following cost driver volumes have been identified: 200 work-in-progress inspections 100 final goods inspections 25 attendances of seminars to update skills and knowledge On the basis of budgeted departmental costs, and a carefully considered but subjective cost analysis, the following budget has been drawn up for the next control period. Table 5.1: Example of activity based budget Total Costs related to work-in- progress inspections Costs related to final goods inspections Costs related to attending seminars Running costs Cost 000 000 000 000 000 50 20 16 6 8 Salary - manager 70 35 25 8 2 2 Salary - inspectors 20 8 7 1 4 Salary - administrator Consumables 4 1 1 1 1 6 2 1 1 2 IT and related costs 2 Other costs 6 2 1 1 2. 156 68 51 18 19 200 100 25 Activity volumes 340 510 720 Cost per cost driver The activity based budget above helps to allocate an overhead like quality inspections to the product cost more logically. If, for example, each of the 300 inspections (200 + 100) relates to 10 manufactured and sold products, then the allocation of the cost of quality control for each product that is sold is 157 ((340 + 510 + 720)/10). (The running costs of 19,000, while important to identify and control, are not activity related costs so need to be allocated separately in an ABB system.)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cost Accounting Foundations and Evolutions

Authors: Michael R. Kinney, Cecily A. Raiborn

8th Edition

9781439044612, 1439044619, 978-1111626822