Answered step by step

Verified Expert Solution

Question

1 Approved Answer

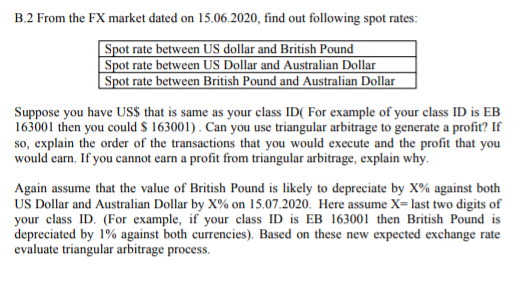

B.2 From the FX market dated on 15.06.2020, find out following spot rates: Spot rate between US dollar and British Pound Spot rate between US

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Art Of M And A A Merger Acquisition Buyout Guide

Authors: Stanley Foster Reed, Alexandria Lajoux , H. Peter Nesvold

4th Edition

0071714952, 9780071714952