Question

BACKGROUND : Blue Ridge Manufacturing is one of a dozen companies that produces and sells towels for the U.S. sports towel market. A sports towel

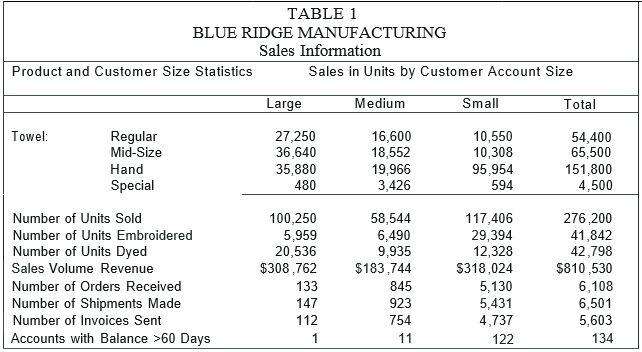

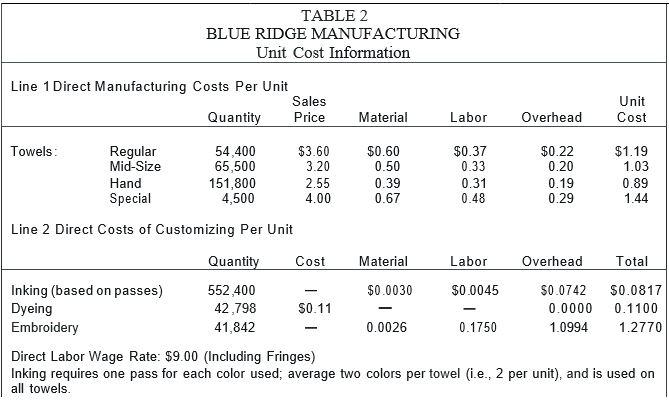

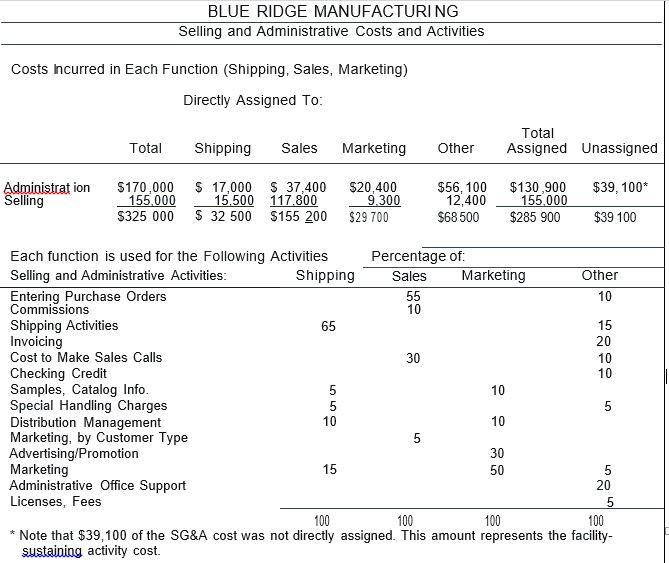

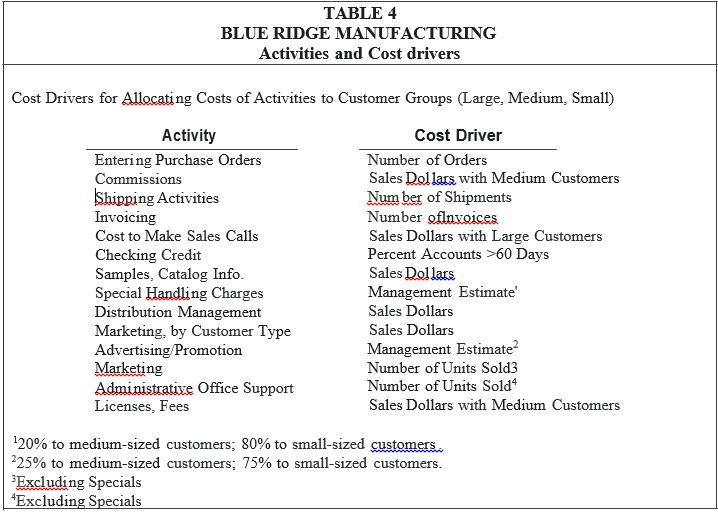

BACKGROUND: Blue Ridge Manufacturing is one of a dozen companies that produces and sells towels for the U.S. "sports towel" market. A "sports towel" is a towel that has the promotion of an event or a logo printed on it. They're called sports towels because their most popular use is for distribution in connection with major sporting events such as the Super Bowl , NCAA Final Four, Augusta National Golf Tournament and the U .S. Open Tennis Tournament. Towels with college, NBA and NFL team logos, and promotions for commercial products such as soft drinks, beer , fast food chains, etc., are also big sellers. The firm designs, knits, prints and embroiders towels. The firm knits al l the towels it sells and tracks costs for towel production separately from the cost to customize the towels. Seventy-five percent of its orders include logo design , while the balance are print only and require the payment of a license fee for the logo used. However, about 15% of its orders i nclude embroidery. Towels are made in three sizes: regular ( 1 8" x 30"), hand ( 12" x 20") and m id-range ( 15"x 24"). The normal production cycle for an order of white towels is three days. If a customer wants a colored towel, the basic white towel made by Blue Ridge is sent to a dyeing firm, which extends the production cycle of an order by three days. Also, occasionally , customers order towels i n sizes other than the three standard sizes. These towels are called "special".The firm now produces a "medium" quality towel. They have had some difficulty with the "staying power" of the material pri nted on these towels, whi ch i s attri buted to the towel qual ity, the ink and the pri nti ng process. Customers have complai ned that the ink "lays on the surface" and it cracks and peels off. Blue Ridge recently made a break-through i n developi ng an ink that soaks i nto the towel , won't wash out and is non-tox ic. A big advantage of this i n k is that it avoids EPA disposal requi rements because is can be "washed down the drain". Due to these characteristics of its new i n k, Bl ue Ridge i s considering upgradi ng the quality of the basic towel it produces because it wi ll "take" the ink better , both the towel and the i n k wi ll last longer and the product wi ll sell at a higher price. If it takes this step, the company wi l l evaluate expanding its marketi ng and sales area with the objective of "going national". CUSTOMERS: Except for a few non-regional chains, Blue Ridge's sales are predominantly in the southeastern states. The company sells its products to 986 different customers. These customers differ primari ly i n the volume of their purchases, so management classifies each customer i n one of three groups: large (8 customers), medi um ( 154 customers) and smal l (824 customers). Large customers are primari ly national chains, small customers are single store operations (i nclud i ng pro shops at golf courses) and mediu m-sized customers are smal l chains, large single stores or l icensing agents for professional sports teams and manufacturers of consumer products . Table I gives the product and customer size statistics for 200 I . Blue Ridge has a differen t approach to customers i n each of its three categories. A small group of in-house sales people sell directly to buyers i n the large customer category. Independent manufacturer representatives , on com m ission, call on the l icense holder or the manager of a store i n the medi um customer category. Ads placed i n regional and national magazines and newspapers target customers pri mari ly i n the small-customer segment, who cal l or mail i n thei r orders. Blue Ridge does not give discounts and it ships all order free on board (FOB) poi nt of origin, i.e., customers pay thei r freight costs. MANUFACTURING: Bl ue Ri dge has a modern knitti ng and pri nti ng plant i n the foothi lls of North Caroli na's Blue Ridge Mountai ns. Upgrading the faci l ities over recent years was accompanied by the introducti on of an activity-based costing (ABC) system to determi ne product costs. The cost accounti ng system is fairly sophisticated and management has confidence in the accuracy of the manufacturi ng cost figures for each product l i ne. Table 2 shows the firm's unit costs for various items. Company management is comm itted to adoptin g advanced manu facturing techniques such as benchm arki ng and j ust-i n-time (JIT). The corporate culture necessary for the success of such techniques is evolv ing and worker empowerment is already a maj or program . J n addition, workers are allowed several hours away from regular work assignments each week for trai ni ng programs conferring on budgets and work im provements and applying the ABC system. PERFORMANCE: The company i s profitabl e. However, management has become concerned about the profitabi l ity of the customers i n its three customer-size categories-l arge, medium and small. Different customers demand different levels of support. Management has no basis for identifying customers that generate high profits or to drop those that do not" generate enough revenues to cover the expenses to support them . Under the prev ious accounti ng system, it wasn't possibl e to determi ne the costs of supporting i ndividual customers. With the i ntroduction of ABC, it now may be possible to determi ne customer profitabi l i ty. Tabl e 3 shows how the admi nistrative and selling costs are assigned and re-assigned between vari ous functions within the selling and m arketing areas and to sub-activities i n the selling and marketing areas. Tabl e 4 provides a l ist of selling and marketing activ iti es and the activity base to use i n assigning costs to each .

REQUIRED:

The managers of Blue Ridge Man ufacturi ng have hi red your consulti ng firm to advise them on the potential of using strategic cost analysis i n assessing the profitabi l ity of their custom er accounts.

Your analysis should i nclude:

l. What is Blue Ridge's com petitive strategy?

- Wh at type of cost system does Blue Ridge use, and i s it consistent with their strategy?

- Develop a spreadsheet analysis which can be used to assess the profitability of the three customer groups of Blue Ridge--large, m edium and small customer account sizes. Use the i nformation in Tabl es 1-4 to trace and allocate the costs necessary for the analysis.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investments Analysis and Management

Authors: Charles P. Jones

12th edition

978-1118475904, 1118475909, 1118363299, 978-1118363294