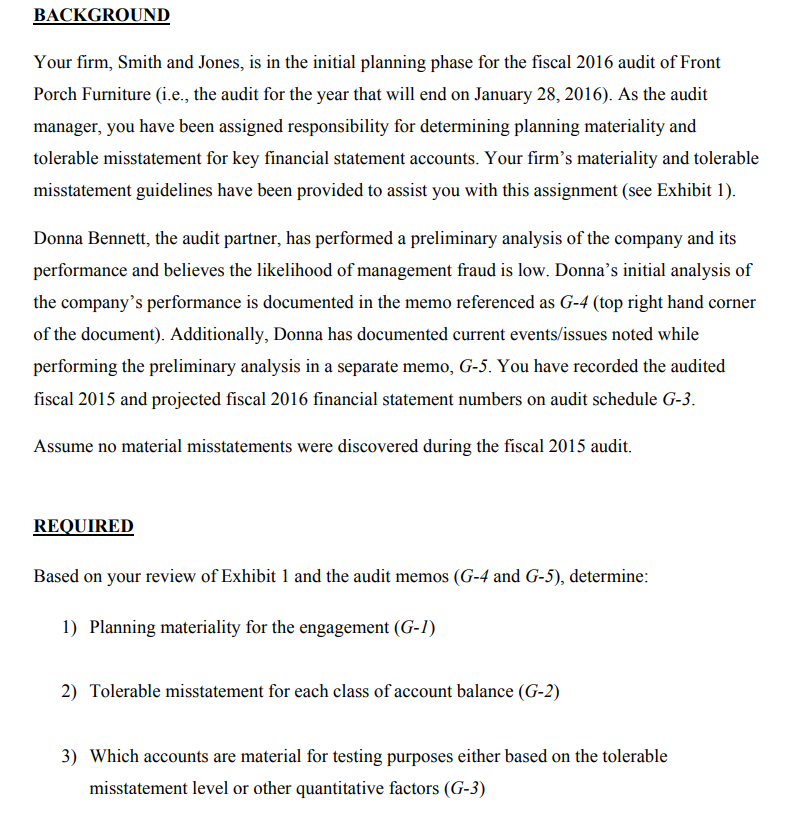

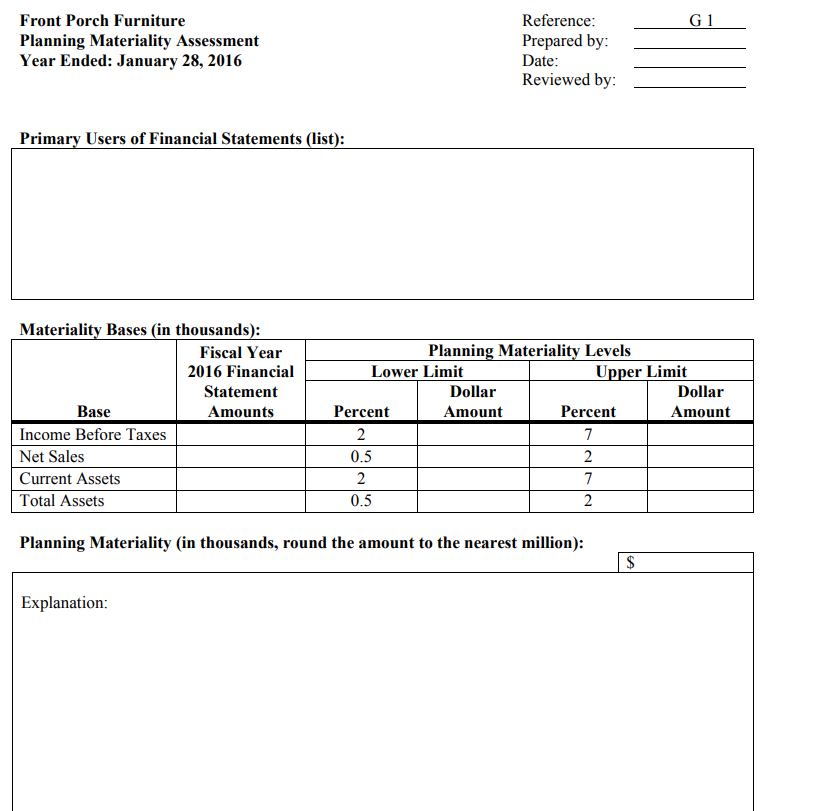

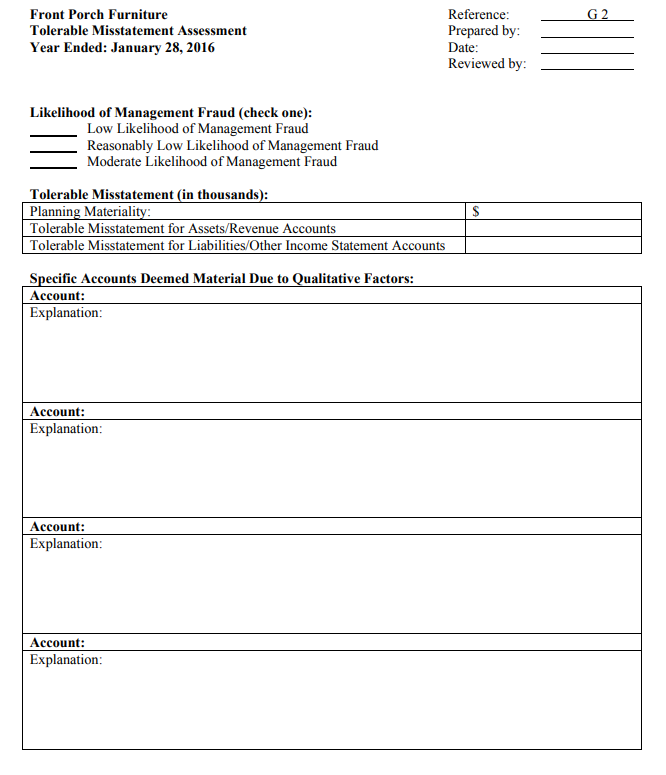

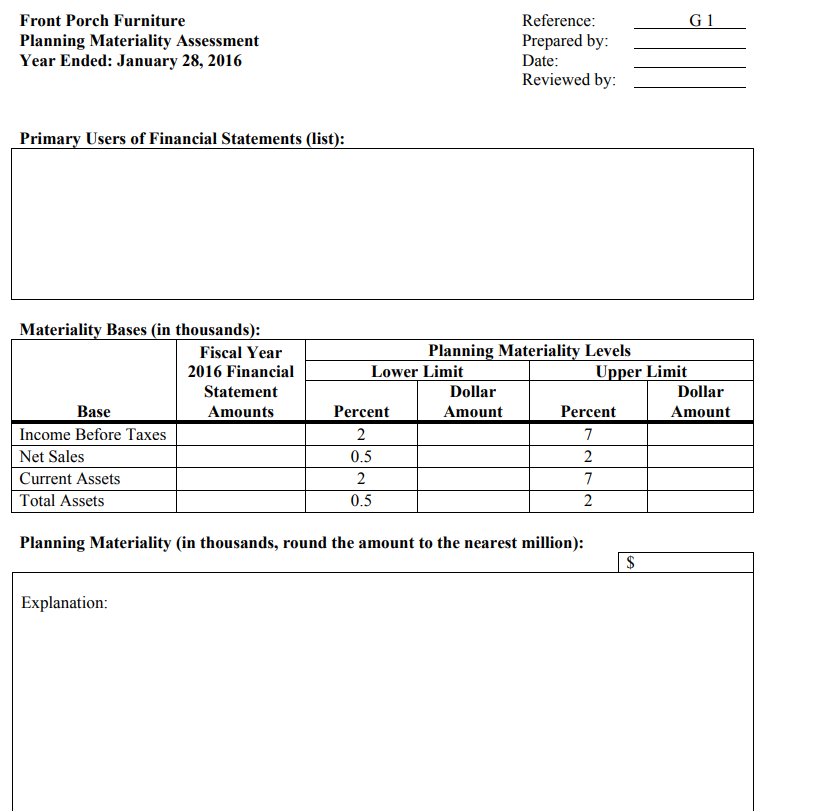

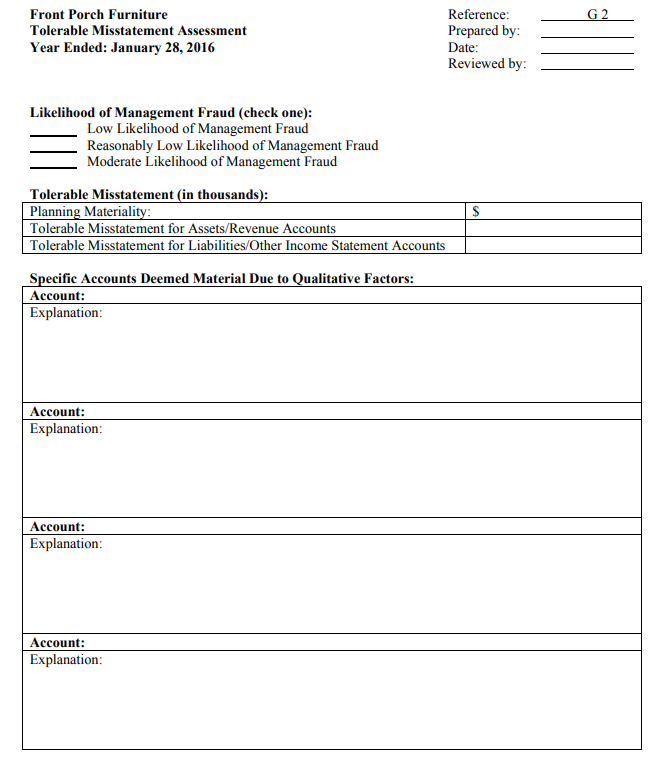

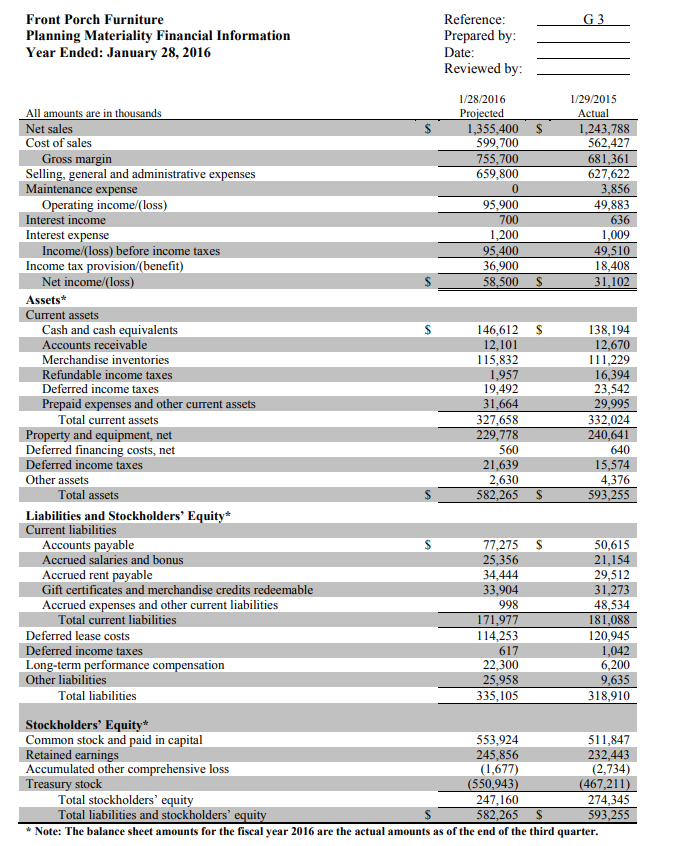

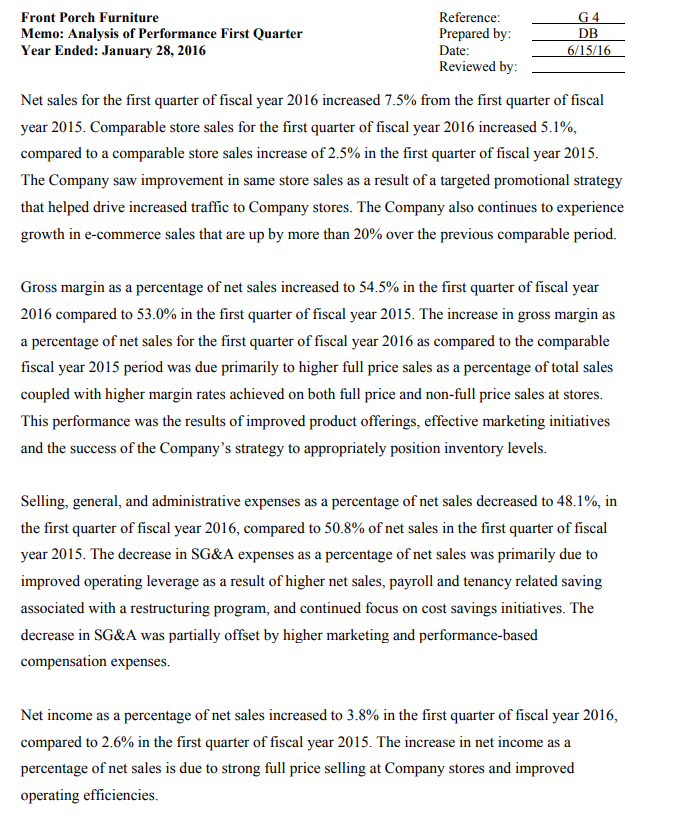

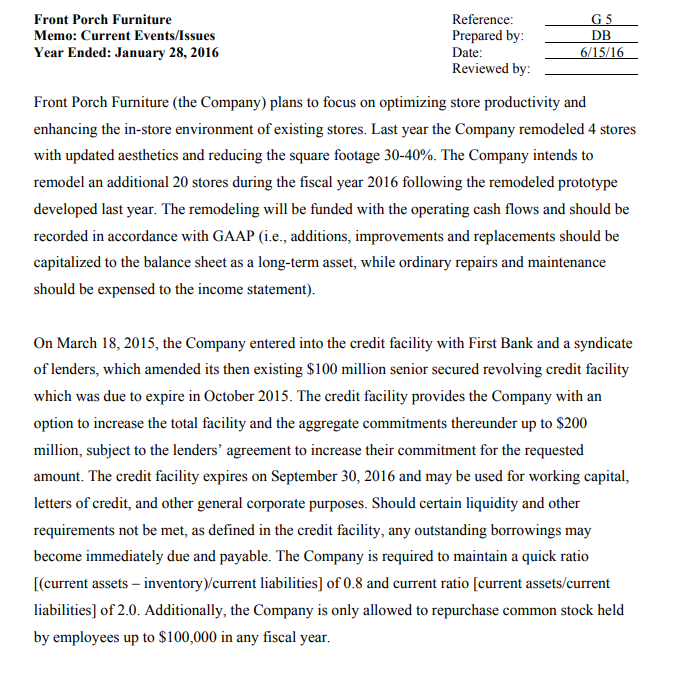

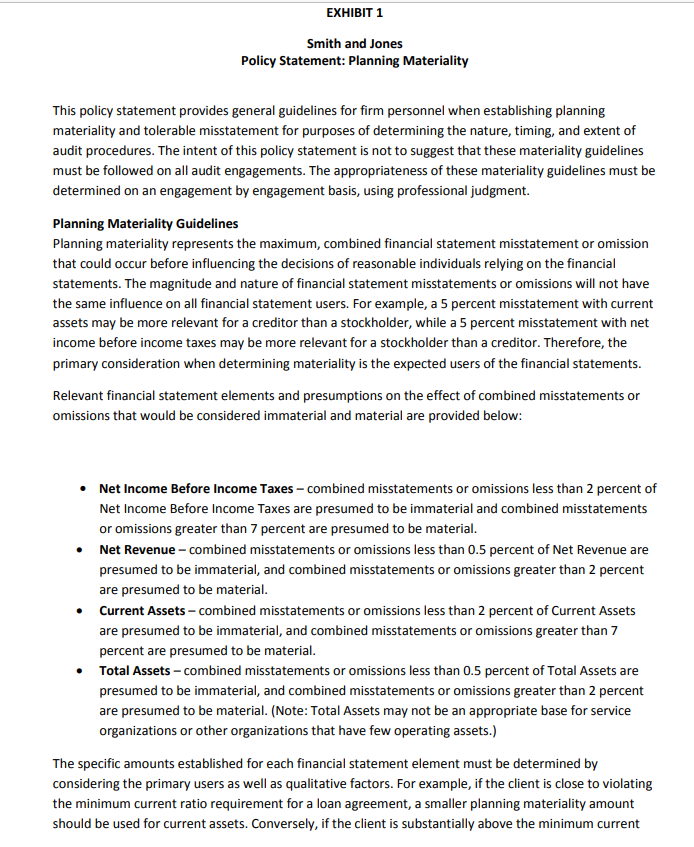

BACKGROUND Your rm, Smith and Jones, is in the initial planning phase for the scal 2016 audit of Front Porch Furniture {i.e., the audit for the year that will end on January 28, 2016}. As the audit manager, you have been assigned responsibility for determining planning materiality and tolerable misstatement for key nancial statement accounts. Your nn's materiality and tolerable misstatement guidelines have been provided to assist you with this assignment (see Exhibit 1). Donna Bennett, the audit partner, has performed a preliminary analysis of the company and its performance and believes the likelihood of management fraud is low. Donna's initial analysis of the company's performance is documented in the memo referenced as 0-4 (top right hand corner of the document). Additionally, Donna has documented current eventsfissues noted while performing the preliminary analysis in a separate memo, G5 . You have recorded the audited scal 2015 and projected scal 2016 nancial statement numbers on audit schedule G3. Assume no material misstatements were discovered during the fiscal 2015 audit. RE UIRED Based on your review of Exhibit 1 and the audit memos {6-4 and G5}, determine: 1) Planning materiality for the engagement (GI ) 2) Tolerable misstatement for each class of account balance (Cf-2) 3) Which accounts are material for testing purposes either based on the tolerable misstatement level or other quantitative factors (6-3} Front Porch Furniture Reference: C 1 Planning Materiality Assessment Prepared by: Year Ended: January 23, 2016 Date: Reviewed by: Primary Users of Financial Statements (list): Materiality Bases (in thousands): Fiscal Year Planning Materiality Levels 2016 Financial Lower Limit Unper Limit Statement Dollar Dollar Base Amounts Percent Amount Percent Amount Income Before Taxes 2 T Net Sales 0.5 2 Current Assets 2 T Total Assets 0.5 2 Planning Materiality (in thousands, round the amount to the nearest million): Explanation: Front Porch Furniture Reference: G2 Tolerable Misstatement Assessment Prepared by: Year Ended: January 28, 2016 Date: Reviewed by: Likelihood of Management Fraud (check one): Low Likelihood of Management Fraud Reasonably Low Likelihood of Management Fraud Moderate Likelihood of Management Fraud Tolerable Misstatement (in thousands): Planning Materiality: $ Tolerable Misstatement for Assets/Revenue Accounts Tolerable Misstatement for Liabilities/Other Income Statement Accounts Specific Accounts Deemed Material Due to Qualitative Factors: Account: Explanation: Account: Explanation: Account: Explanation: Account: Explanation:Front Porch Furniture Reference: G 3 Planning Materiality Financial Information Prepared by: Year Ended: January 28, 2016 Date: Reviewed by: 1/28/2016 1/29/2015 All amounts are in thousands Projected Actual Net sales S 1,355,400 $ 1,243,788 Cost of sales 599,700 562,427 Gross margin 755,700 681,361 Selling, general and administrative expenses 659,800 627,622 Maintenance expense 3,856 Operating income/(loss) 95.900 19,883 Interest income 700 636 Interest expense 1,200 1,009 Income/(loss) before income taxes 95.400 49,510 Income tax provision (benefit) 36,900 18,408 Net income/(loss) 58,500 $ 31,102 Assets* Current assets Cash and cash equivalents S 146,612 $ 138,194 Accounts receivable 12,101 12,670 Merchandise inventories 115,832 111,229 Refundable income taxes 1.957 16,394 Deferred income taxes 19,492 23,542 Prepaid expenses and other current assets 31,664 29,995 Total current assets 327,658 332,024 Property and equipment, net 229,778 240,641 Deferred financing costs, net 560 640 Deferred income taxes 21,639 15,574 Other assets 2.630 4,376 Total assets S 582,265 $ 593,255 Liabilities and Stockholders' Equity* Current liabilities Accounts payable $ 77,275 5 50,615 Accrued salaries and bonus 25,356 21,154 Accrued rent payable 34.444 29,512 Gift certificates and merchandise credits redeemable 33,904 31,273 Accrued expenses and other current liabilities 998 48,534 Total current liabilities 171,977 181,088 Deferred lease costs 1 14,253 120,945 Deferred income taxes 617 1,042 Long-term performance compensation 22,300 6,200 Other liabilities 25,958 9,635 Total liabilities 335,105 318,910 Stockholders Equity* Common stock and paid in capital 553,924 511,847 Retained earnings 245,856 232,443 Accumulated other comprehensive loss (1,677) (2,734) Treasury stock (550,943) (467,211) Total stockholders' equity 247,160 274,345 Total liabilities and stockholders' equity S 582,265 593,255 Note: The balance sheet amounts for the fiscal year 2016 are the actual amounts as of the end of the third quarter.Front Porch Furniture Reference: G 4 Memo: Analysis of Performance First Quarter Prepared by: DB Year Ended: January 28, 2016 Date: 6/15/16 Reviewed by: Net sales for the first quarter of fiscal year 2016 increased 7.5% from the first quarter of fiscal year 2015. Comparable store sales for the first quarter of fiscal year 2016 increased 5.1%, compared to a comparable store sales increase of 2.5% in the first quarter of fiscal year 2015. The Company saw improvement in same store sales as a result of a targeted promotional strategy that helped drive increased traffic to Company stores. The Company also continues to experience growth in e-commerce sales that are up by more than 20% over the previous comparable period. Gross margin as a percentage of net sales increased to 54.5% in the first quarter of fiscal year 2016 compared to 53.0% in the first quarter of fiscal year 2015. The increase in gross margin as a percentage of net sales for the first quarter of fiscal year 2016 as compared to the comparable fiscal year 2015 period was due primarily to higher full price sales as a percentage of total sales coupled with higher margin rates achieved on both full price and non-full price sales at stores. This performance was the results of improved product offerings, effective marketing initiatives and the success of the Company's strategy to appropriately position inventory levels. Selling, general, and administrative expenses as a percentage of net sales decreased to 48.1%, in the first quarter of fiscal year 2016, compared to 50.8% of net sales in the first quarter of fiscal year 2015. The decrease in SG&A expenses as a percentage of net sales was primarily due to improved operating leverage as a result of higher net sales, payroll and tenancy related saving associated with a restructuring program, and continued focus on cost savings initiatives. The decrease in SG&A was partially offset by higher marketing and performance-based compensation expenses. Net income as a percentage of net sales increased to 3.8% in the first quarter of fiscal year 2016, compared to 2.6% in the first quarter of fiscal year 2015. The increase in net income as a percentage of net sales is due to strong full price selling at Company stores and improved operating efficiencies.Front Porch Furniture Reference: G 5 Memo: Current Events/Issues Prepared by: DB Year Ended: January 28, 2016 Date 6/15/16 Reviewed by: Front Porch Furniture (the Company) plans to focus on optimizing store productivity and enhancing the in-store environment of existing stores. Last year the Company remodeled 4 stores with updated aesthetics and reducing the square footage 30-40%. The Company intends to remodel an additional 20 stores during the fiscal year 2016 following the remodeled prototype developed last year. The remodeling will be funded with the operating cash flows and should be recorded in accordance with GAAP (i.e., additions, improvements and replacements should be capitalized to the balance sheet as a long-term asset, while ordinary repairs and maintenance should be expensed to the income statement). On March 18, 2015, the Company entered into the credit facility with First Bank and a syndicate of lenders, which amended its then existing $100 million senior secured revolving credit facility which was due to expire in October 2015. The credit facility provides the Company with an option to increase the total facility and the aggregate commitments thereunder up to $200 million, subject to the lenders' agreement to increase their commitment for the requested amount. The credit facility expires on September 30, 2016 and may be used for working capital, letters of credit, and other general corporate purposes. Should certain liquidity and other requirements not be met, as defined in the credit facility, any outstanding borrowings may become immediately due and payable. The Company is required to maintain a quick ratio [(current assets - inventory )/current liabilities] of 0.8 and current ratio [current assets/current liabilities] of 2.0. Additionally, the Company is only allowed to repurchase common stock held by employees up to $100,000 in any fiscal year.EXHIBIT 1 Smith and Jones Policy Statement: Planning Materiality This policy statement provides general guidelines for firm personnel when establishing planning materiality and tolerable misstatement for purposes of determining the nature, timing, and extent of audit procedures. The intent of this policy statement is not to suggest that these materiality guidelines must be followed on all audit engagements. The appropriateness of these materiality guidelines must be determined on an engagement by engagement basis, using professional judgment. Planning Materiality Guidelines Planning materiality represents the maximum, combined financial statement misstatement or omission that could occur before influencing the decisions of reasonable individuals relying on the financial statements. The magnitude and nature of financial statement misstatements or omissions will not have the same influence on all financial statement users. For example, a 5 percent misstatement with current assets may be more relevant for a creditor than a stockholder, while a 5 percent misstatement with net income before income taxes may be more relevant for a stockholder than a creditor. Therefore, the primary consideration when determining materiality is the expected users of the financial statements. Relevant financial statement elements and presumptions on the effect of combined misstatements or omissions that would be considered immaterial and material are provided below: Net Income Before Income Taxes - combined misstatements or omissions less than 2 percent of Net Income Before Income Taxes are presumed to be immaterial and combined misstatements or omissions greater than 7 percent are presumed to be material. Net Revenue - combined misstatements or omissions less than 0.5 percent of Net Revenue are presumed to be immaterial, and combined misstatements or omissions greater than 2 percent are presumed to be material. Current Assets - combined misstatements or omissions less than 2 percent of Current Assets are presumed to be immaterial, and combined misstatements or omissions greater than 7 percent are presumed to be material. Total Assets - combined misstatements or omissions less than 0.5 percent of Total Assets are presumed to be immaterial, and combined misstatements or omissions greater than 2 percent are presumed to be material. (Note: Total Assets may not be an appropriate base for service organizations or other organizations that have few operating assets.) The specific amounts established for each financial statement element must be determined by considering the primary users as well as qualitative factors. For example, if the client is close to violating the minimum current ratio requirement for a loan agreement, a smaller planning materiality amount should be used for current assets. Conversely, if the client is substantially above the minimum currentratio requirement for a loan agreement, it would be reasonable to use a higher planning materiality amount for current assets. Planning materiality should be based on the smallest amount established from relevant materiality bases to provide reasonable assurance that the financial statements, taken as a whole, are not materially misstated for any user. Tolerable Misstatement Guidelines In addition to establishing materiality for overall financial statements, materiality for individual financial statements accounts should be established. The amount established for individual accounts is referred to as "tolerable misstatement." Tolerable misstatement represents the amount individual financial statements accounts can differ from their true amount without affecting the fair presentation of the financial statements taken as a whole. Establishment of tolerable misstatement for individual accounts enables the auditor to design and execute an audit strategy for each audit cycle. The objective in setting tolerable misstatement for individual financial statement accounts is to provide reasonable assurance that the financial statements taken as a whole are fairly presented in all material respects at the lowest cost. To provide reasonable assurance that the financial statements taken as a whole do not contain material misstatements, the tolerable misstatement established for individual financial statement accounts should not exceed 75 percent of planning materiality for asset and revenue accounts and 50 percent of planning materiality for liability, stockholder's equity, and all other income statement accounts. The percentage threshold should be lower as the expectation for management fraud increase. In many audits it is reasonable to expect that individual financial accounts misstatements identified will be less than tolerable misstatement and that misstatements across accounts will offset each other (some identified misstatements will overstate net income and some identified misstatements will understate net income). This expectation is not reasonable when the likelihood of management fraud is high. If management is intentionally trying to misstate the financial statements, it is likely that misstatements will be systematically biased in one direction across accounts. Finally a lower tolerable misstatement may be required for specific accounts because of the relevance of the account to users. Tolerable misstatement for a specific account should not exceed that amount that would influence the decision of reasonable users. Approved: October 23, 2014