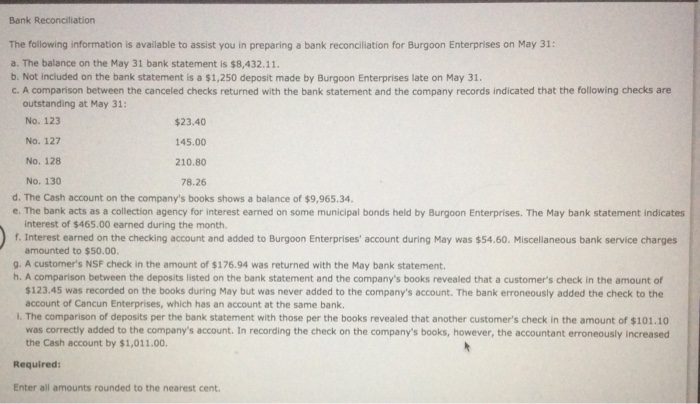

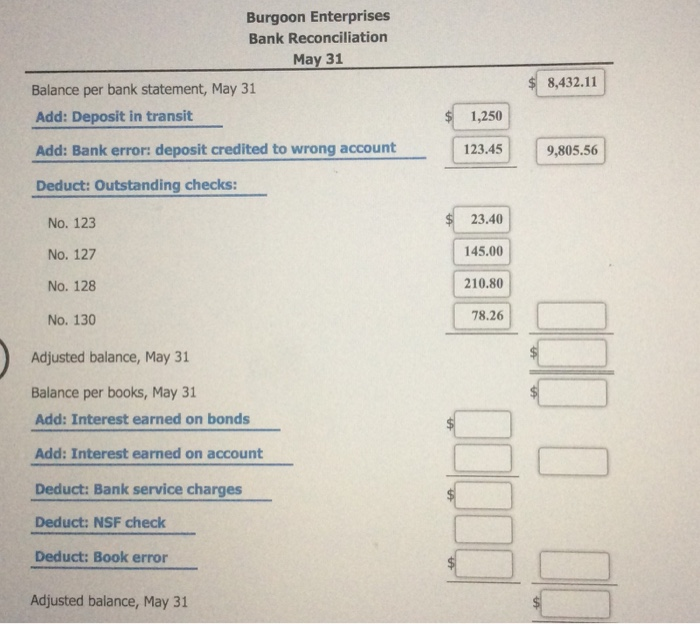

Bank Reconciliation The following information is available to assist you in preparing a bank reconciliation for Burgoon Enterprises on May 31: a. The balance on the May 31 bank statement is $8,432.11. b. Not included on the bank statement is a $1,250 deposit made by Burgoon Enterprises late on May 31. c. A comparison between the canceled checks returned with the bank statement and the company records indicated that the following checks are outstanding at May 31: No. 123 $23.40 No. 127 145.00 No. 128 210.80 No. 130 78.26 d. The Cash account on the company's books shows a balance of $9,965.34. e. The bank acts as a collection agency for interest earned on some municipal bonds held by Burgoon Enterprises. The May bank statement indicates interest of $465.00 earned during the month f. Interest earned on the checking account and added to Burgoon Enterprises' account during May was $54.60. Miscellaneous bank service charges amounted to $50.00 9. A customer's NSF check in the amount of $176.94 was returned with the May bank statement. h. A comparison between the deposits listed on the bank statement and the company's books revealed that a customer's check in the amount of $123.45 was recorded on the books during May but was never added to the company's account. The bank erroneously added the check to the account of Cancun Enterprises, which has an account at the same bank. The comparison of deposits per the bank statement with those per the books revealed that another customer's check in the amount of $101.10 was correctly added to the company's account. In recording the check on the company's books, however, the accountant erroneously increased the Cash account by $1,011.00 Required: Enter all amounts rounded to the nearest cent. Burgoon Enterprises Bank Reconciliation May 31 Balance per bank statement, May 31 Add: Deposit in transit $ 8,432.11 1,250 Add: Bank error: deposit credited to wrong account 123.45 9,805.56 Deduct: Outstanding checks: No. 123 23.40 No. 127 145.00 No. 128 210.80 No. 130 78.26 Adjusted balance, May 31 Balance per books, May 31 Add: Interest earned on bonds Add: Interest earned on account Deduct: Bank service charges Deduct: NSF check Deduct: Book error Adjusted balance, May 31 2. A friend says to you: "I don't know why companies bother to prepare bank reconciliations-it seems a waste of time. Why don't they just do like I do and adjust the Cash account for any difference between what the bank shows as a balance and what shows up in the books?" Why does a bank reconciliation should be prepared as soon as a bank statement is received. A bank reconciliation is needed to detect errors and omissions in records