Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Barbara Reynolds suggest that if cash is needed for capital budget a stock dividend could be substituted for cash dividend .Do you agree? How do

Barbara Reynolds suggest that if cash is needed for capital budget a stock dividend could be substituted for cash dividend .Do you agree? How do you think stockholders would react ?Regardless of their reaction is the stock dividend an equivalent substitute for the cash dividend.

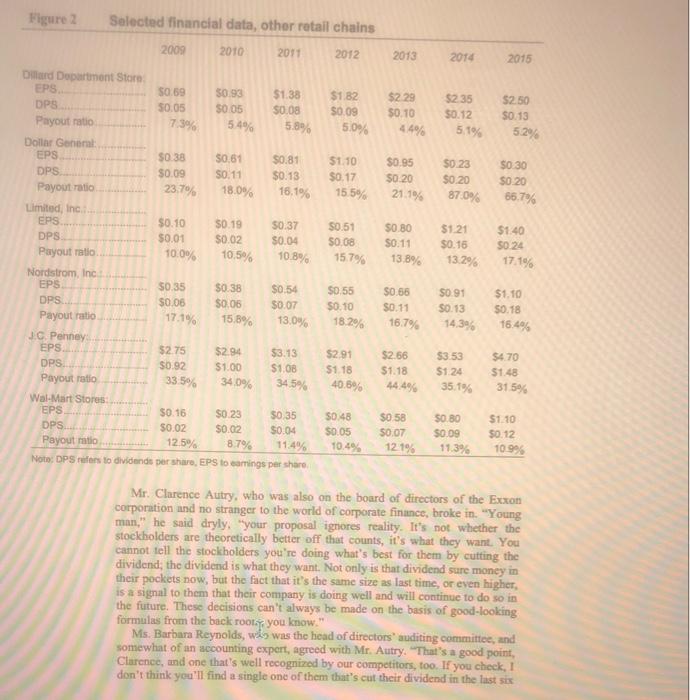

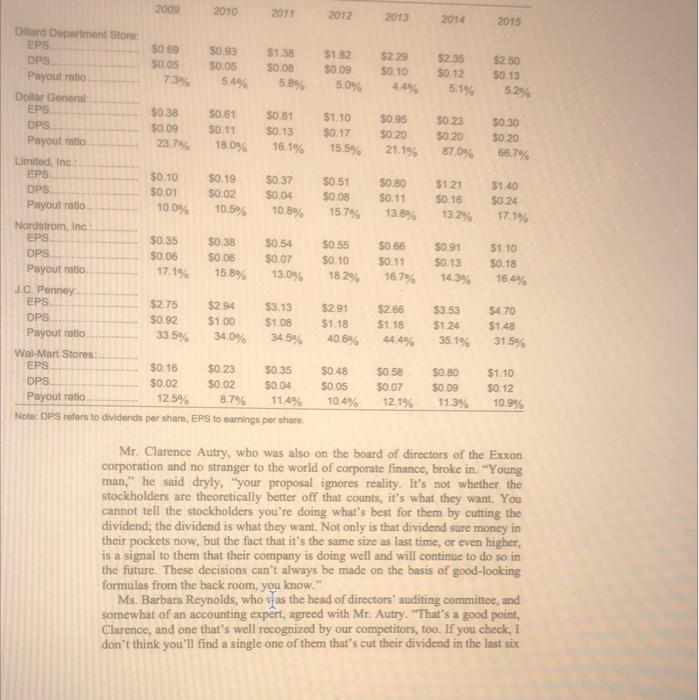

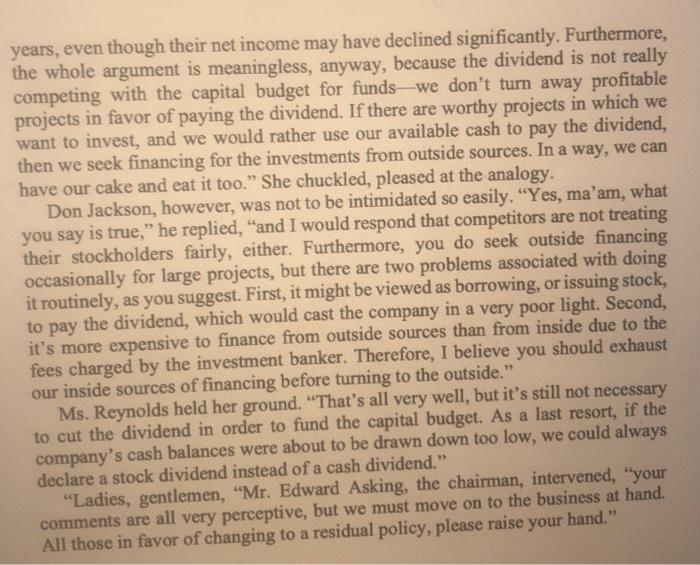

Figure 2 Selected financial data, other retail chains 2009 2010 2011 2012 2013 2014 2015 $1.82 $0.09 5.0% $2 29 $0.10 $2.35 $0.12 7.3% $2.50 50.13 52% 44% 5.1% $1.10 $0.17 15.5% $0.95 $0.20 21.1% $0 23 $0.20 87.0% SO 30 $0.20 66.7% 50.51 50.08 $0.80 S0.11 13.8% Dard Department Store EPS 50:59 $0.93 $1.38 DPS 50.05 50.05 50.08 Payout ratio 5.4% 5.8% Dollar General EPS $0.38 $0.61 $0.81 DPS $0.09 50.11 $0.13 Payout ratio 23.7% 18.0% 16.1% Limited, Inc EPS $0.10 S0.19 50.37 DPS $0.01 S0.02 30.04 Payout ratio 100% 10.5% 10.8% Nordstrom, Inc EPS 50.35 $0.38 $0.54 DPS S0.06 $0.06 $0.07 Payout ratio 17.1% 15.8% 13.0% JC Penney EPS $275 $2.94 $3.13 DPS. $0.92 $1.00 $1.08 Payout ratio 33.5% 34,5% Wal-Mart Stores EPS $0.16 SO 23 $0 35 DPS. $0.02 $0.02 $0.04 Payout ratio 12.5% 8.7% 11.4% Note: DPS refers to dividends per shar, EPS to samnings per share $1.21 $0.16 13.2% $1.40 50.24 17.1% 15.79% $0.55 $0.10 SO 56 S0.11 16.7% $0.91 50.13 14.39 $1.10 $0.18 18.2% 16.4% $2.91 $1.18 $2.66 $1.18 $3.53 $124 $4.70 $1.48 340% 40.6% 35.1% 31 5% $0.48 50.05 10.4% SO 58 50.07 12.1% $0.80 50.09 11.3% $1.10 $0.12 10.99 Mr. Clarence Autry, who was also on the board of directors of the Exxon corporation and no stranger to the world of corporate finance, broke in. "Young man," he said dryly, "your proposal ignores reality. It's not whether the stockholders are theoretically better off that counts, it's what they want. You cannot tell the stockholders you're doing what's best for them by cutting the dividend, the dividend is what they want. Not only is that dividend sure money in their pockets now, but the fact that it's the same size as last time, or even higher, is a signal to them that their company is doing well and will continue to do so in the future. These decisions can't always be made on the basis of good-looking formulas from the back rooty, you know." Ms. Barbara Reynolds, wis was the head of directors' auditing committee, and somewhat of an accounting expert, agreed with Mr. Autry. "That's a good point, Clarence, and one that's well recognized by our competitors, too. If you check, 1 don't think you'll find a single one of them that's cut their dividend in the last six 2009 2010 2011 2012 2013 2014 2015 $1.82 SO 09 5.0% 52.29 $0.10 $2.35 SO 12 5.1% $250 0.13 5.2% $1.10 50.17 $0.95 $0.20 21.1% 50 23 $0.20 87.0% $0.30 SO 20 16.1% 15,5% 56.7% $0.51 S0.08 15.7% SO:80 $0.11 13.8% $1.21 S0.15 13.2% Dard Department Store EPS $0.69 50.83 5138 DPS S0.05 S0.05 50.08 Payout ratio 73% 5.4% 5.8% Dollar General EPS $0.38 $0.61 $0.81 DPS $0.09 50.11 $0.13 Payout ratio 23.7% 18.0% Limited, Ino EPS 30.10 $0.19 $0.37 DPS 30.01 50.02 $0.04 Payout ratio 10.0% 10.5% 10.8% Nordstrom, Inc EPS $0.35 $0.38 $0.54 DPS $0.06 S0.06 $0.07 Payout ratio 17.1% 15.8% 13.0% JC Penney EPS 52.75 $2.94 $3.13 DPS $0.92 $100 $1.08 Payout ratio 33.5% 34.0% 34 5% Wal-Mart Stores EPS $0.16 $0,23 $0 35 DPS $0.02 $0.02 30.04 Payout ratio 12.5% 8.7% 11.4% Note: DPS refers to dividends per shar, EPS to carings per share. $1.40 50 24 17.1% SO 55 $0.10 18.2% $0 66 $0.51 $0.91 $0.13 14.3% $1.10 $0.18 16.4% 16.7% S291 $1.18 40.6% $2.56 $1.18 44.4% $3.53 $1.24 $4.70 $148 35.1% 315% $0.48 $0.05 10.4% $0.58 $0.07 $0.80 $0.09 11.3% $1.10 $0.12 10.9% 12.1% Mr. Clarence Autry, who was also on the board of directors of the Exxon corporation and no stranger to the world of corporate finance, broke in. "Young man," he said dryly, "your proposal ignores reality. It's not whether the stockholders are theoretically better off that counts, it's what they want. You cannot tell the stockholders you're doing what's best for them by cutting the dividend; the dividend is what they want. Not only is that dividend sure money in their pockets now, but the fact that it's the same size as last time, or even higher, is a signal to them that their company is doing well and will continue to do so in the future. These decisions can't always be made on the basis of good-looking formulas from the back room, you know." Ms. Barbara Reynolds, who fas the head of directors' auditing committee, and somewhat of an accounting expert, agreed with Mr. Autry. "That's a good point, Clarence, and one that's well recognized by our competitors, too. If you check, I don't think you'll find a single one of them that's cut their dend in the years, even though their net income may have declined significantly. Furthermore, the whole argument is meaningless, anyway, because the dividend is not really competing with the capital budget for funds-we don't turn away profitable projects in favor of paying the dividend. If there are worthy projects in which we want to invest, and we would rather use our available cash to pay the dividend, then we seek financing for the investments from outside sources. In a way, we can have our cake and eat it too." She chuckled, pleased at the analogy. Don Jackson, however, was not to be intimidated so easily. "Yes, ma'am, what you say is true," he replied, "and I would respond that competitors are not treating their stockholders fairly, either. Furthermore, you do seek outside financing occasionally for large projects, but there are two problems associated with doing it routinely, as you suggest. First, it might be viewed as borrowing, or issuing stock, to pay the dividend, which would cast the company in a very poor light. Second, it's more expensive to finance from outside sources than from inside due to the fees charged by the investment banker. Therefore, I believe you should exhaust our inside sources of financing before turning to the outside." Ms. Reynolds held her ground. That's all very well, but it's still not necessary to cut the dividend in order to fund the capital budget. As a last resort, if the company's cash balances were about to be drawn down too low, we could always declare a stock dividend instead of a cash dividend." "Ladies, gentlemen, "Mr. Edward Asking, the chairman, intervened, "your comments are all very perceptive, but we must move on to the business at hand. All those in favor of changing to a residual policy, please raise your hand Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advanced Finance Theories

Authors: Ser-Huang Poon

1st Edition

9814460370, 978-9814460378