Answered step by step

Verified Expert Solution

Question

1 Approved Answer

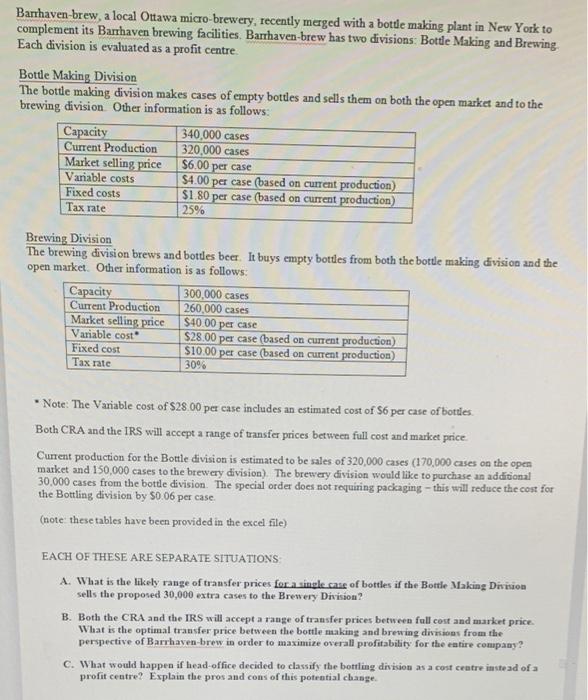

Barthaven-brew, a local Ottawa micro-brewery, recently merged with a botde making plant in New York to complement its Barrhaven brewing facilities. Barrhaven-brew has two divisions

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Traffic Trilogy Access To Millions Of Ultra Targeted Visitors For Pennies On The Dollar

Authors: Fred Lam

1st Edition

1530332788, 978-1530332786