Based on the case answer the all questions

Questions:

1. Brief Overview (Describe the Company and issues discussed)

2. Situation Analysis (SWOT)

3. Key Issues (Symptoms/Problems)

4. Alternatives (A set of strategic alternatives that have a potential to solve the problem)

5. Evaluation of Alternatives (How well does the alternative address the issue stated? / List the pros and cons of each alternative)

6. Recommendation

7. Implementation Plan (Steps to follow constrained by budget and timeline/Short term and long term plan/Always look for appendices)

8. Risk and Mitigation (List all the challenges that would prevent the company from successfully implementing the proposed solution/List risk mitigation strategies for every challenge)

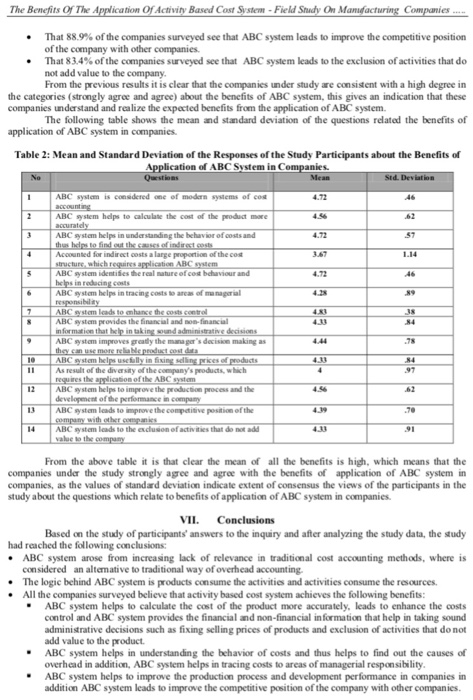

OSR Journal of Business and Management dOSR-JBM e-ISSN: 2278-487X. p-ISSN: 2319-7668 Volume 16, Issue 1.Ver. I (Nov. 2014), PP 39-45 The Benefits of the Application of Activity Based Cost System- Field Study on Manufacturing Companies Operating In Allahabad City India Mr. Shaban E. A. Salem, Dr. Shabana Mazhar? Ph.D.Research Scholar, Business Administration Department Joseph School of Business Studies, SHIATS India) (Associate Professor, Business Administration Deparment, Joseph School of Business Snudies, SHIATS, India Abstract: This study aims to identifying the benefits of the application of ABC system throuth fidd study on companies operating in allahabad-india- In order to achieve such aims, questionnaire was developed and distributed to the population of studly. Spss program was ased in the analysis The study concluded with some resuts The most apparent is that the expected benefits of behind the application of ABC system from the standpoint of these companies are ABC system helps to calculate the cost of the product more accuratey, leads to enhance the costs control and ABC system provides the financial and non-financial information that help in taking sound administrative decisions such as fixing selling prices of products and ystem from lh s arcunteds, le exclusion of activities that do not add value to the product The sranly recommends he companies should start gradazIly in plying ABC stem by persuading the management of these companies on the inmportance of application the system because of its advantages and henefits Key BC System, Traditional Cost System, Overkead I Introduction In the present era, companies produce wide range of products and direct labour represent only a small percentage of total costs, the intense global competition has made decision errors due to poor cost information more problem and more costly, also in this computer age of advancing technologies and aormation, de proportion and importance of overhead in the manufacturing operations is increasing and direct costs are being relegated to the background. Overhead is the aggregate of indirect materials, indirect wages and indirect expenses (M. N. Arora,2013) it is a well-known fact the traditional cost systems utilize a single volume-based cost driver, this is the reason why the traditional cost systam distorts the cost of products (V. K. Saxena, et al, 2011). In most cases this type of costing system assigns the overhead costs to products on the basis of their relative usage of direct labour. For this reason traditional cost systems often report inaccurate product costs. Therefore, there is a need for a more sophisticated system of accounting for overhead so that more accurate costs of products and services may be ascertained. activity based cost system which known as (ABC system) is an altemative to traditional way of overhead accounting, it is an upcoming and more refined approach of charging overhead to ascertain more accurate product costs (V. Rajasekaran, et al, 201) ABC system arose in the 1980s from the increasing lack of relevance of traditional cost accounting methods, it is developed by cooper and kalpan for assigning overhead to end products, jobs and processes, it aims to rectify the problem of inaccurate cost in formation due to selection of wrong bases of overhead apportionment (Charles t. Horngren,et al, 2013) this study comes as an attempt to explain the concept of ABC system, in addition to determine the expected benefits of application of ABC system in companies under study I The Study Problem manufacturing companies this study problem attempts to answer the following question: are there any benefits III. The Study Objectives In light of the growing interest in topic of importance and benefits of the application of ABC system in from the application of ABC in companies? This study aims to attain the following objectives: To highlight the concept of ABC system in addition to know the advantages and disadvantages of ABC system. .Being acquainted with the benefits of application of ABC system in companies OSR Journal of Business and Management dOSR-JBM e-ISSN: 2278-487X. p-ISSN: 2319-7668 Volume 16, Issue 1.Ver. I (Nov. 2014), PP 39-45 The Benefits of the Application of Activity Based Cost System- Field Study on Manufacturing Companies Operating In Allahabad City India Mr. Shaban E. A. Salem, Dr. Shabana Mazhar? Ph.D.Research Scholar, Business Administration Department Joseph School of Business Studies, SHIATS India) (Associate Professor, Business Administration Deparment, Joseph School of Business Snudies, SHIATS, India Abstract: This study aims to identifying the benefits of the application of ABC system throuth fidd study on companies operating in allahabad-india- In order to achieve such aims, questionnaire was developed and distributed to the population of studly. Spss program was ased in the analysis The study concluded with some resuts The most apparent is that the expected benefits of behind the application of ABC system from the standpoint of these companies are ABC system helps to calculate the cost of the product more accuratey, leads to enhance the costs control and ABC system provides the financial and non-financial information that help in taking sound administrative decisions such as fixing selling prices of products and ystem from lh s arcunteds, le exclusion of activities that do not add value to the product The sranly recommends he companies should start gradazIly in plying ABC stem by persuading the management of these companies on the inmportance of application the system because of its advantages and henefits Key BC System, Traditional Cost System, Overkead I Introduction In the present era, companies produce wide range of products and direct labour represent only a small percentage of total costs, the intense global competition has made decision errors due to poor cost information more problem and more costly, also in this computer age of advancing technologies and aormation, de proportion and importance of overhead in the manufacturing operations is increasing and direct costs are being relegated to the background. Overhead is the aggregate of indirect materials, indirect wages and indirect expenses (M. N. Arora,2013) it is a well-known fact the traditional cost systems utilize a single volume-based cost driver, this is the reason why the traditional cost systam distorts the cost of products (V. K. Saxena, et al, 2011). In most cases this type of costing system assigns the overhead costs to products on the basis of their relative usage of direct labour. For this reason traditional cost systems often report inaccurate product costs. Therefore, there is a need for a more sophisticated system of accounting for overhead so that more accurate costs of products and services may be ascertained. activity based cost system which known as (ABC system) is an altemative to traditional way of overhead accounting, it is an upcoming and more refined approach of charging overhead to ascertain more accurate product costs (V. Rajasekaran, et al, 201) ABC system arose in the 1980s from the increasing lack of relevance of traditional cost accounting methods, it is developed by cooper and kalpan for assigning overhead to end products, jobs and processes, it aims to rectify the problem of inaccurate cost in formation due to selection of wrong bases of overhead apportionment (Charles t. Horngren,et al, 2013) this study comes as an attempt to explain the concept of ABC system, in addition to determine the expected benefits of application of ABC system in companies under study I The Study Problem manufacturing companies this study problem attempts to answer the following question: are there any benefits III. The Study Objectives In light of the growing interest in topic of importance and benefits of the application of ABC system in from the application of ABC in companies? This study aims to attain the following objectives: To highlight the concept of ABC system in addition to know the advantages and disadvantages of ABC system. .Being acquainted with the benefits of application of ABC system in companies