Answered step by step

Verified Expert Solution

Question

1 Approved Answer

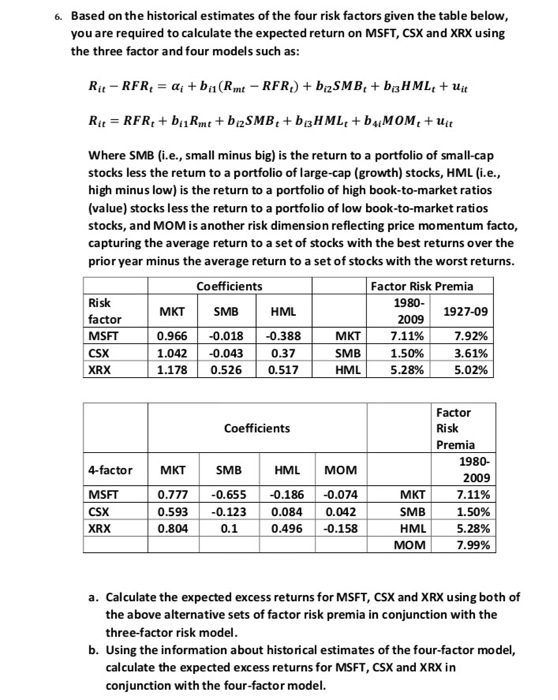

Based on the historical estimates of the four risk factors given the table below you are required to calculate the expected return on MSFT, CSX

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Passive Income Stacking Handbook How To Reach Financial Freedom Faster Regardless Of Your Age Or Situation

Authors: Mark Walters

1st Edition

0578530171, 978-0578530178