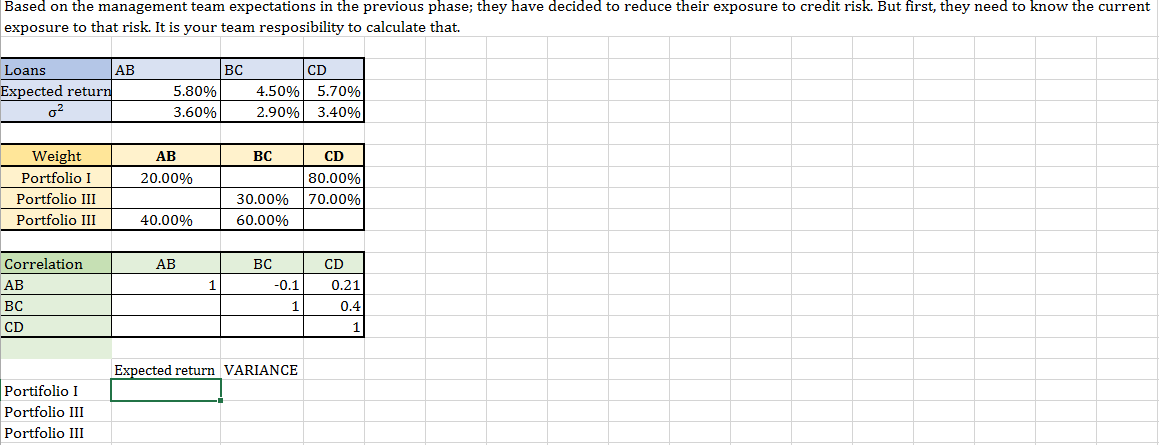

Question

Based on the management team expectations in the previous phase; they have decided to reduce their exposure to credit risk. But first, they need to

Based on the management team expectations in the previous phase; they have decided to reduce their exposure to credit risk. But first, they need to know the current exposure to that risk. It is your team resposibility to calculate that.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Electronic Waste An Actual Gold And Silver Mine

Authors: Antonio Alcivar

1st Edition

979-8367641059