BAT4M

Unit 1 Activity 6

Practice Exercise - Adjusting Entries

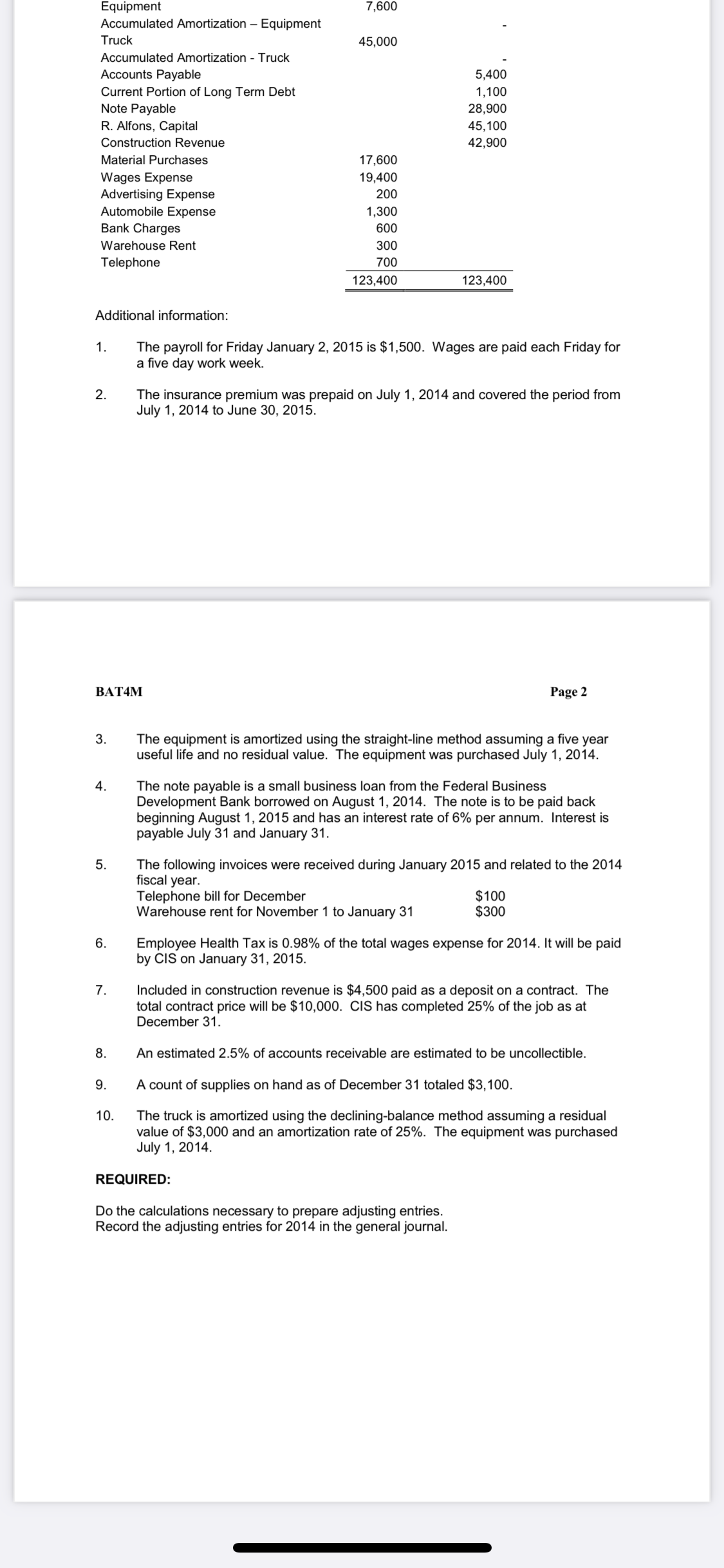

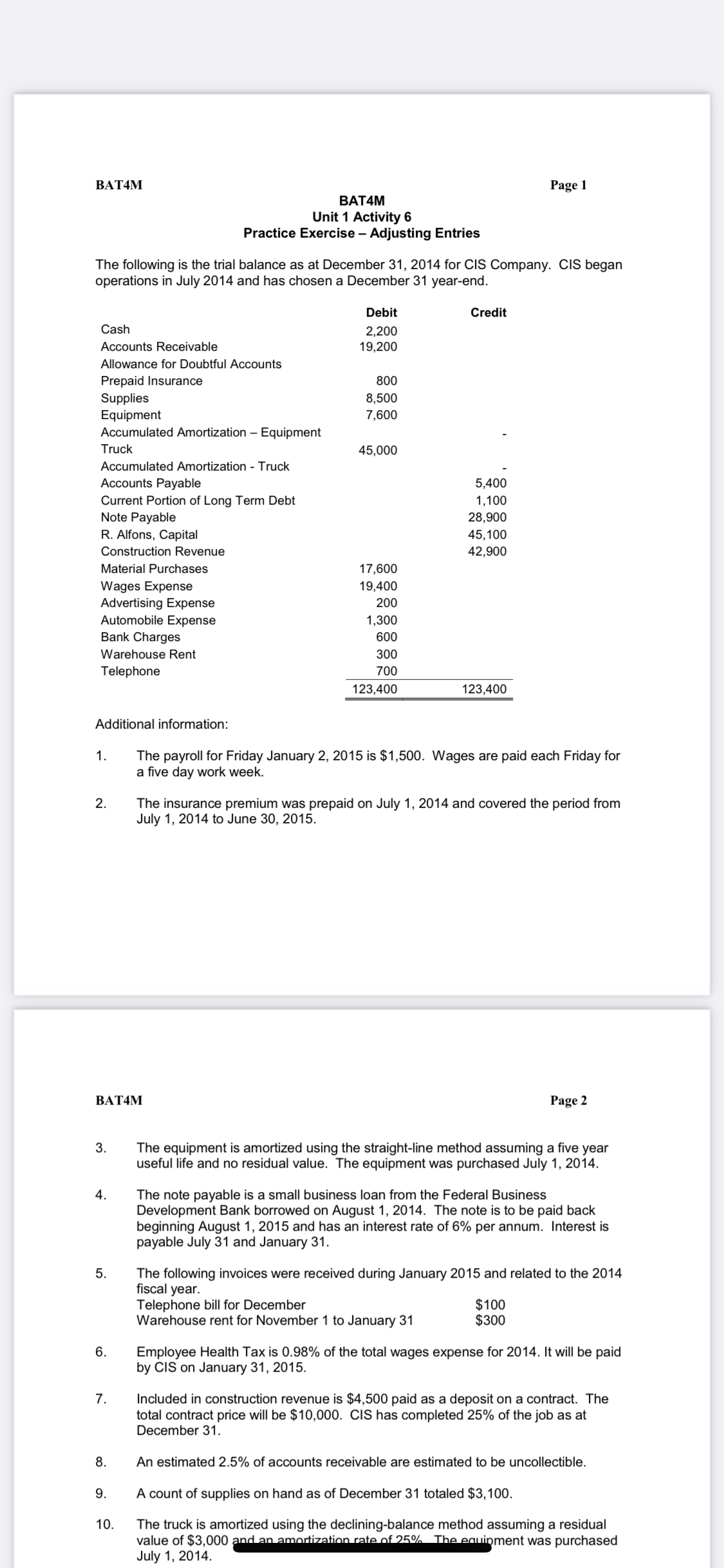

Equipment 7.600 Accumulated Amortization Equipment - Truck 45.000 Accumulated Amortization - Truck _ Accounts Payable 5,400 Current Portion of Long Term Debt 1,100 Note Payable 28,900 R. Alfons, Capital 45,100 Construction Revenue 42,900 Material Purchases 17.600 Wages Expense 19.400 Advertising Expense 200 Automobile Expense 1.300 Bank Charges 600 Warehouse Rent 300 Telephone 700 123.400 123,400 Additional information: 1. The payroll for Friday January 2, 2015 is $1,500. Wages are paid each Friday for a ve day work week. 2. The insurance premium was prepaid on July 1, 2014 and covered the period from July 1, 2014 to June 30, 2015. BAT4M Page 2 3. The equipment is amortized using the straight-line method assuming a ve year useful life and no residual value. The equipment was purchased July 1, 2014. 4. The note payable is a small business loan from the Federal Business Development Bank borrowed on August 1, 2014. The note is to be paid back beginning August 1, 2015 and has an interest rate of 6% per annum. Interest is payable July 31 and January 31. 5. The following invoices were received during January 2015 and related to the 2014 scal year. Telephone bill for December $100 Warehouse rent for November 1 to January 31 $300 6. Employee Health Tax is 0.98% of the total wages expense for 2014. It will be paid by CIS on January 31, 2015. 7. Included in construction revenue is $4,500 paid as a depositon a contract. The total contract price will be $10,000. CIS has completed 25% of the job as at December 31. 8. An estimated 2.5% of accounts receivable are estimated to be uncollectible. 9. A count of supplies on hand as of December 31 totaled $3,100. 10. The truck is amortized using the declining-balance method assuming a residual value of $3,000 and an amortization rate of 25%. The equipment was purchased July 1. 2014. REQUIRED: Do the calculations necessary to prepare adjusting entries. Record the adjusting entries for 2014 in the general journal. BAT4M Page 1 BAT4M Unit 1 Activity 6 Practice Exercise - Adjusting Entries The following is the trial balance as at December 31, 2014 for CIS Company. CIS began operations in July 2014 and has chosen a December 31 year-end. Debit Credit Cash 2,200 Accounts Receivable 19,200 Allowance for Doubtful Accounts Prepaid Insurance 800 Supplies 8,500 Equipment 7,600 Accumulated Amortization - Equipment Truck 45,000 Accumulated Amortization - Truck Accounts Payable 5,400 Current Portion of Long Term Debt 1,100 Note Payable 28,900 R. Alfons, Capital 45,100 Construction Revenue 42,900 Material Purchases 17,600 Wages Expense 19,400 Advertising Expense 200 Automobile Expense 1,300 Bank Charges 600 Warehouse Rent 300 Telephone 700 123,400 123,400 Additional information: 1 . The payroll for Friday January 2, 2015 is $1,500. Wages are paid each Friday for a five day work week. 2. The insurance premium was prepaid on July 1, 2014 and covered the period from July 1, 2014 to June 30, 2015. BAT4M Page 2 3. The equipment is amortized using the straight-line method assuming a five year useful life and no residual value. The equipment was purchased July 1, 2014. 4 The note payable is a small business loan from the Federal Business Development Bank borrowed on August 1, 2014. The note is to be paid back beginning August 1, 2015 and has an interest rate of 6% per annum. Interest is payable July 31 and January 31. 5 The following invoices were received during January 2015 and related to the 2014 fiscal year. Telephone bill for December $100 Warehouse rent for November 1 to January 31 $300 6. Employee Health Tax is 0.98% of the total wages expense for 2014. It will be paid by CIS on January 31, 2015. 7 Included in construction revenue is $4,500 paid as a deposit on a contract. The total contract price will be $10,000. CIS has completed 25% of the job as at December 31. 8. An estimated 2.5% of accounts receivable are estimated to be uncollectible. 9. A count of supplies on hand as of December 31 totaled $3, 100. 10. The truck is amortized using the declining-balance method assuming a residual value of $3,000 and an amortization rate of 25% The equipment was purchased July 1, 2014