Answered step by step

Verified Expert Solution

Question

1 Approved Answer

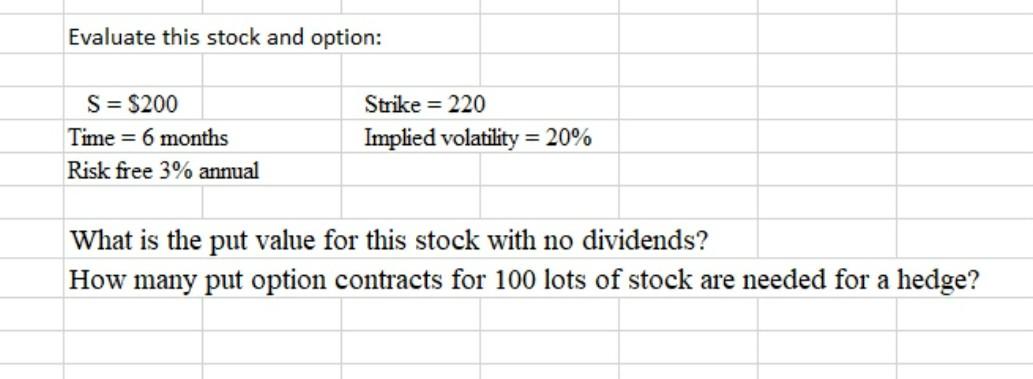

be fast plzz Evaluate this stock and option: S = $200 Time = 6 months Risk free 3% annual Strike = 220 Implied volatility =

be fast plzz

Evaluate this stock and option: S = $200 Time = 6 months Risk free 3% annual Strike = 220 Implied volatility = 20% What is the put value for this stock with no dividends? How many put option contracts for 100 lots of stock are needed for a hedge

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Literacy For Young Adults Simplified Discover How To Manage Save And Invest Money To Build A Secure And Independent Future

Authors: Raman Keane

1st Edition

8399806501, 979-8399806501