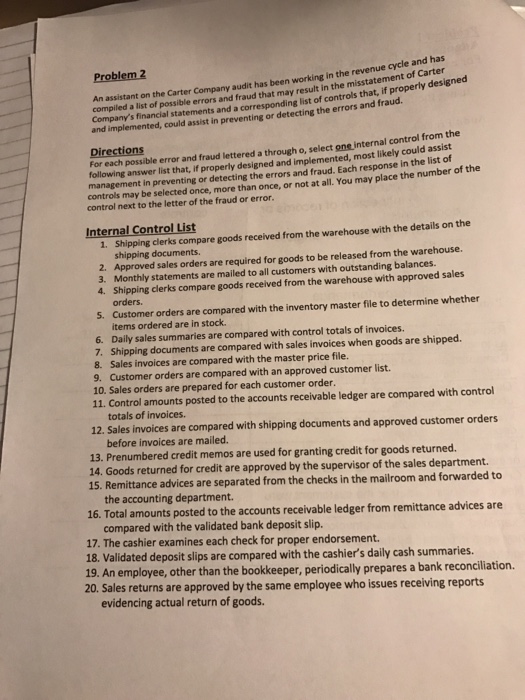

been working in the revenue cycle and has tement of Carter Problem 2 An assistant on the Carter Company audit has igned Company's financial statements and a corresponding list of controls that, if properly des and implemented, could assist in preventing or detecting the errors and fraud. compiled a list of possible errors and fraud that may result in the missta For each possible error and fraud lettered a through o, select one internal control from the management in controls may be selected once, more than once, or not at all. You may place the number of the answer list that, if properly designed and implemented, most likely could assist preventing or detecting the errors and fraud. Each response in the list of control next to the letter of the fraud or error. Internal Control List Shipping clerks compare goods received from the warehouse with the details on the shipping documents 1. 2. Approved sales orders are required for goods to be released from the warehouse. 3. Monthly statements are mailed to all customers with outstanding balances. 4. Shipping clerks compare goods received from the warehouse with approved sales orders. 5. Customer orders are compared with the inventory master file to determine whether items ordered are in stock. 6. Daily sales summaries are compared with control totals of invoices. 7. Shipping documents are compared with sales invoices when goods are shipped. 8. Sales invoices are compared with the master price file. 9. Customer orders are compared with an approved customer list 10. Sales orders are prepared for each customer order. 11. Control amounts posted to the accounts receivable ledger are compared with control totals of invoices. 12. Sales invoices are compared with shipping documents and approved customer orders before invoices are mailed. 13. Prenumbered credit memos are used for granting credit for goods returned. 14. Goods returned for credit are approved by the supervisor of the sales department. 15. Remittance advices are separated from the checks in the mailroom and forwarded to the accounting department. 16. Total amounts posted to the accounts receivable ledger from remittance advices are compared with the validated bank deposit slip. 17. The cashier examines each check for proper endorsement. 18. Validated deposit slips are compared with the cashier's daily cash summaries. 19. An 20. Sales returns are approved by the same employee who issues receiving reports employee, other than the bookkeeper, periodically prepares a bank reconciliation. evidencing actual return of goods been working in the revenue cycle and has tement of Carter Problem 2 An assistant on the Carter Company audit has igned Company's financial statements and a corresponding list of controls that, if properly des and implemented, could assist in preventing or detecting the errors and fraud. compiled a list of possible errors and fraud that may result in the missta For each possible error and fraud lettered a through o, select one internal control from the management in controls may be selected once, more than once, or not at all. You may place the number of the answer list that, if properly designed and implemented, most likely could assist preventing or detecting the errors and fraud. Each response in the list of control next to the letter of the fraud or error. Internal Control List Shipping clerks compare goods received from the warehouse with the details on the shipping documents 1. 2. Approved sales orders are required for goods to be released from the warehouse. 3. Monthly statements are mailed to all customers with outstanding balances. 4. Shipping clerks compare goods received from the warehouse with approved sales orders. 5. Customer orders are compared with the inventory master file to determine whether items ordered are in stock. 6. Daily sales summaries are compared with control totals of invoices. 7. Shipping documents are compared with sales invoices when goods are shipped. 8. Sales invoices are compared with the master price file. 9. Customer orders are compared with an approved customer list 10. Sales orders are prepared for each customer order. 11. Control amounts posted to the accounts receivable ledger are compared with control totals of invoices. 12. Sales invoices are compared with shipping documents and approved customer orders before invoices are mailed. 13. Prenumbered credit memos are used for granting credit for goods returned. 14. Goods returned for credit are approved by the supervisor of the sales department. 15. Remittance advices are separated from the checks in the mailroom and forwarded to the accounting department. 16. Total amounts posted to the accounts receivable ledger from remittance advices are compared with the validated bank deposit slip. 17. The cashier examines each check for proper endorsement. 18. Validated deposit slips are compared with the cashier's daily cash summaries. 19. An 20. Sales returns are approved by the same employee who issues receiving reports employee, other than the bookkeeper, periodically prepares a bank reconciliation. evidencing actual return of goods