Answered step by step

Verified Expert Solution

Question

1 Approved Answer

begin{tabular}{|c|c|c|c|c|c|c|c|} hline & L & M & N & 0 & Q & S & T hline 1 & & mean & 0.032063 &

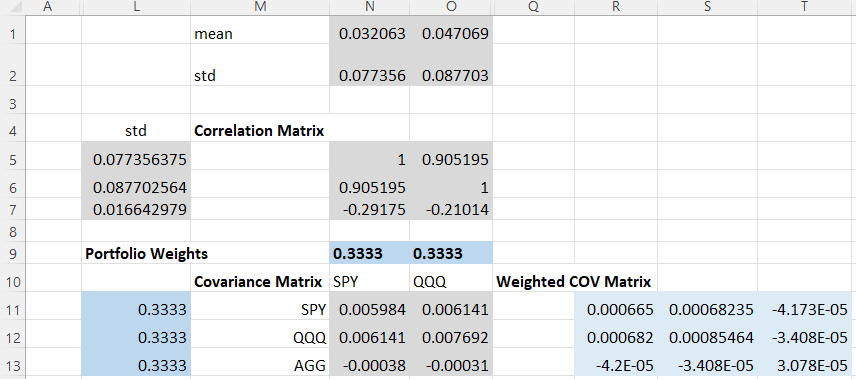

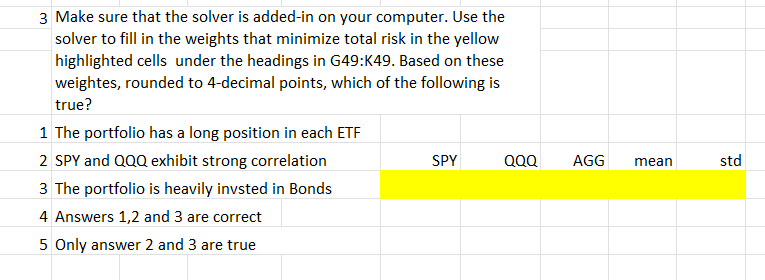

\begin{tabular}{|c|c|c|c|c|c|c|c|} \hline & L & M & N & 0 & Q & S & T \\ \hline 1 & & mean & 0.032063 & 0.047069 & & & \\ \hline 2 & & std & 0.077356 & 0.087703 & & & \\ \hline \multicolumn{8}{|l|}{3} \\ \hline 4 & std & \multicolumn{2}{|l|}{ Correlation Matrix } & & & & \\ \hline 5 & 0.077356375 & & 1 & 0.905195 & & & \\ \hline 6 & 0.087702564 & & 0.905195 & 1 & & & \\ \hline 7 & 0.016642979 & & -0.29175 & -0.21014 & & & \\ \hline 8 & & & & & & & \\ \hline 9 & \multicolumn{2}{|c|}{ Portfolio Weights } & 0.3333 & 0.3333 & & & \\ \hline 10 & & Covariance Matrix & SPY & QQQ & Weighted COV Matrix & & \\ \hline 11 & 0.3333 & SPY & 0.005984 & 0.006141 & 0.000665 & 0.00068235 & 4.173E05 \\ \hline 12 & 0.3333 & QQQ & 0.006141 & 0.007692 & 0.000682 & 0.00085464 & 3.408E05 \\ \hline 13 & 0.3333 & AGG & -0.00038 & -0.00031 & 4.2E05 & 3.408E05 & 3.078E05 \\ \hline \end{tabular} 3 Make sure that the solver is added-in on your computer. Use the solver to fill in the weights that minimize total risk in the yellow highlighted cells under the headings in G49:K49. Based on these weightes, rounded to 4-decimal points, which of the following is true? 1 The portfolio has a long position in each ETF 2 SPY and QQQ exhibit strong correlation SPY QQQ AGG mean std 3 The portfolio is heavily invsted in Bonds 4 Answers 1,2 and 3 are correct 5 Only answer 2 and 3 are true

\begin{tabular}{|c|c|c|c|c|c|c|c|} \hline & L & M & N & 0 & Q & S & T \\ \hline 1 & & mean & 0.032063 & 0.047069 & & & \\ \hline 2 & & std & 0.077356 & 0.087703 & & & \\ \hline \multicolumn{8}{|l|}{3} \\ \hline 4 & std & \multicolumn{2}{|l|}{ Correlation Matrix } & & & & \\ \hline 5 & 0.077356375 & & 1 & 0.905195 & & & \\ \hline 6 & 0.087702564 & & 0.905195 & 1 & & & \\ \hline 7 & 0.016642979 & & -0.29175 & -0.21014 & & & \\ \hline 8 & & & & & & & \\ \hline 9 & \multicolumn{2}{|c|}{ Portfolio Weights } & 0.3333 & 0.3333 & & & \\ \hline 10 & & Covariance Matrix & SPY & QQQ & Weighted COV Matrix & & \\ \hline 11 & 0.3333 & SPY & 0.005984 & 0.006141 & 0.000665 & 0.00068235 & 4.173E05 \\ \hline 12 & 0.3333 & QQQ & 0.006141 & 0.007692 & 0.000682 & 0.00085464 & 3.408E05 \\ \hline 13 & 0.3333 & AGG & -0.00038 & -0.00031 & 4.2E05 & 3.408E05 & 3.078E05 \\ \hline \end{tabular} 3 Make sure that the solver is added-in on your computer. Use the solver to fill in the weights that minimize total risk in the yellow highlighted cells under the headings in G49:K49. Based on these weightes, rounded to 4-decimal points, which of the following is true? 1 The portfolio has a long position in each ETF 2 SPY and QQQ exhibit strong correlation SPY QQQ AGG mean std 3 The portfolio is heavily invsted in Bonds 4 Answers 1,2 and 3 are correct 5 Only answer 2 and 3 are true Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Probability For Risk Management

Authors: Matthew J. Hassett, Donald G. Stewart

2nd Edition

156698548X, 978-1566985482