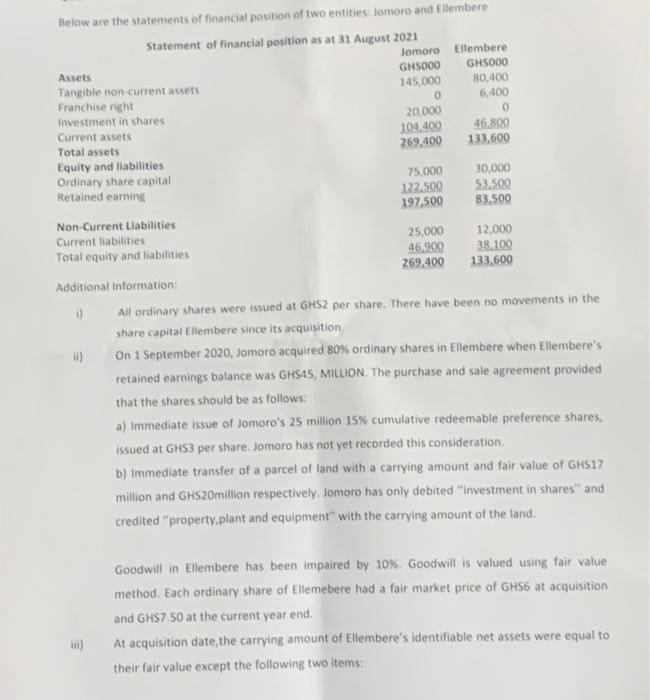

Below are the statements of financial position of two entities: Jomoro and fllembere Additional information: i) All ordinary shares were issued at GHS2 per share. There have been no movements in the share capital Ellembere since its acquisition. ii) On 1 September 2020 , Jomoro acquired 80% ordinary shares in Ellembere when Ellembere's retained earnings balance was GHS45, MILLON. The purchase and sale agreement provided that the shares should be as follows: a) Immediate issue of Jomoro's 25 million 15% cumulative redeemable preference shares, issued at GHS3 per share. Jomoro has not yet recorded this consideration. b) Immediate transfer of a parcel of land with a carrying amount and fair value of GHS17 million and GHS20million respectively. Jomoro has only debited "investment in shares" and credited "property.plant and equipment" with the carrying amount of the land. Goodwill in Ellembere has been impaired by 10%. Goodwill is valued using fair value method. Each ordinary share of Ellemebere had a fair market price of GHS6 at acquisition and GHS7 50 at the current year end. iii) At acquisition date, the carrying amount of Ellembere's identifiable net assets were equal to their fair value except the following two items: a) Intangible asset(purchase franchise right)has a fair value of Gtis12 million and carrying amount of the right at 31 August 2021 was estimated at GHs9million. Ellembere has hot incorporated the fair values in its separate financial stateinents. (Ignore deferred tax for this adjustment). b) An iten of equipment has its fair value of GHS5 million in excess of its camying amount. It had a remaining useful life of 5 years. The faif value adjustment should be deemed as temporary difference which suffers tax of 20%. (v) Jomoro accounts for Il passive equity investment at fair value through other comprehension income. The fair value of Jomora's investment in Ellembere was GHS110million as at 11 August 2021. v) Ellembere sold goods to Jomoro for ghs 3.2 million in July 2021 . Jomoro held a half of these items in its yeat end inventory. Ellembere bought the goods sold to lonoro for GHs5million from an outside supplier. At year end, Ellembere still owed the supplier aow of the purchase cost. At yearend, Jomoro did not owe Ellembere in respect of the above transactions. All Items were in good condition at the date of transfer. Ignore any deferred tax implications. Required: Prepare a consolidated statement of financial position as at 31 August 2021 Below are the statements of financial position of two entities: Jomoro and fllembere Additional information: i) All ordinary shares were issued at GHS2 per share. There have been no movements in the share capital Ellembere since its acquisition. ii) On 1 September 2020 , Jomoro acquired 80% ordinary shares in Ellembere when Ellembere's retained earnings balance was GHS45, MILLON. The purchase and sale agreement provided that the shares should be as follows: a) Immediate issue of Jomoro's 25 million 15% cumulative redeemable preference shares, issued at GHS3 per share. Jomoro has not yet recorded this consideration. b) Immediate transfer of a parcel of land with a carrying amount and fair value of GHS17 million and GHS20million respectively. Jomoro has only debited "investment in shares" and credited "property.plant and equipment" with the carrying amount of the land. Goodwill in Ellembere has been impaired by 10%. Goodwill is valued using fair value method. Each ordinary share of Ellemebere had a fair market price of GHS6 at acquisition and GHS7 50 at the current year end. iii) At acquisition date, the carrying amount of Ellembere's identifiable net assets were equal to their fair value except the following two items: a) Intangible asset(purchase franchise right)has a fair value of Gtis12 million and carrying amount of the right at 31 August 2021 was estimated at GHs9million. Ellembere has hot incorporated the fair values in its separate financial stateinents. (Ignore deferred tax for this adjustment). b) An iten of equipment has its fair value of GHS5 million in excess of its camying amount. It had a remaining useful life of 5 years. The faif value adjustment should be deemed as temporary difference which suffers tax of 20%. (v) Jomoro accounts for Il passive equity investment at fair value through other comprehension income. The fair value of Jomora's investment in Ellembere was GHS110million as at 11 August 2021. v) Ellembere sold goods to Jomoro for ghs 3.2 million in July 2021 . Jomoro held a half of these items in its yeat end inventory. Ellembere bought the goods sold to lonoro for GHs5million from an outside supplier. At year end, Ellembere still owed the supplier aow of the purchase cost. At yearend, Jomoro did not owe Ellembere in respect of the above transactions. All Items were in good condition at the date of transfer. Ignore any deferred tax implications. Required: Prepare a consolidated statement of financial position as at 31 August 2021