Answered step by step

Verified Expert Solution

Question

1 Approved Answer

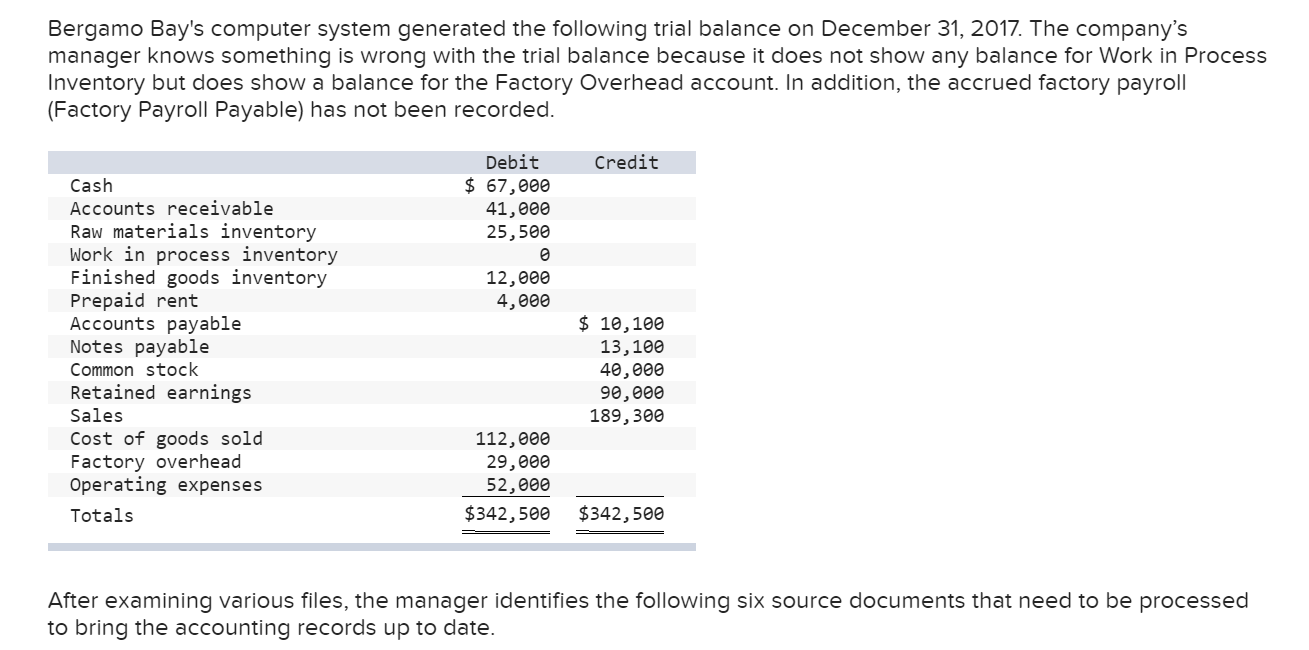

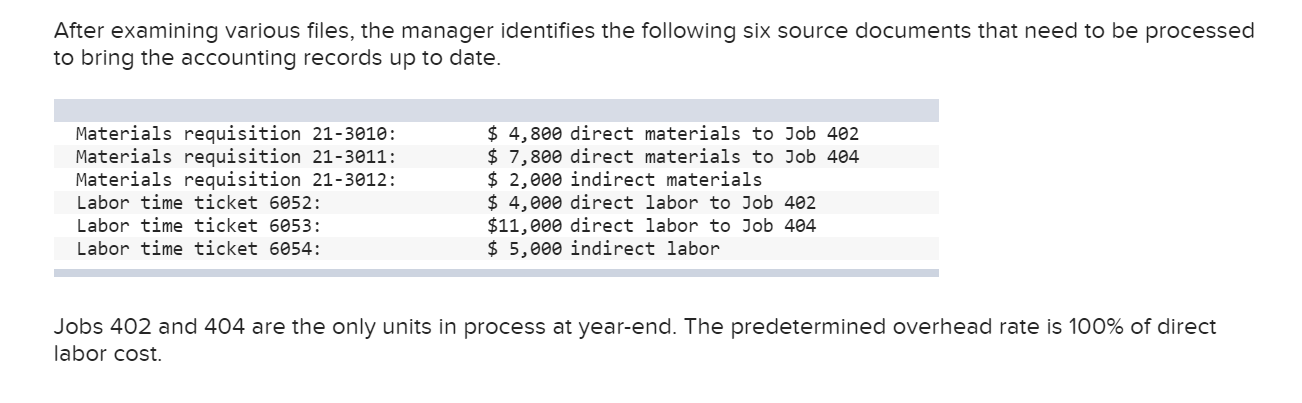

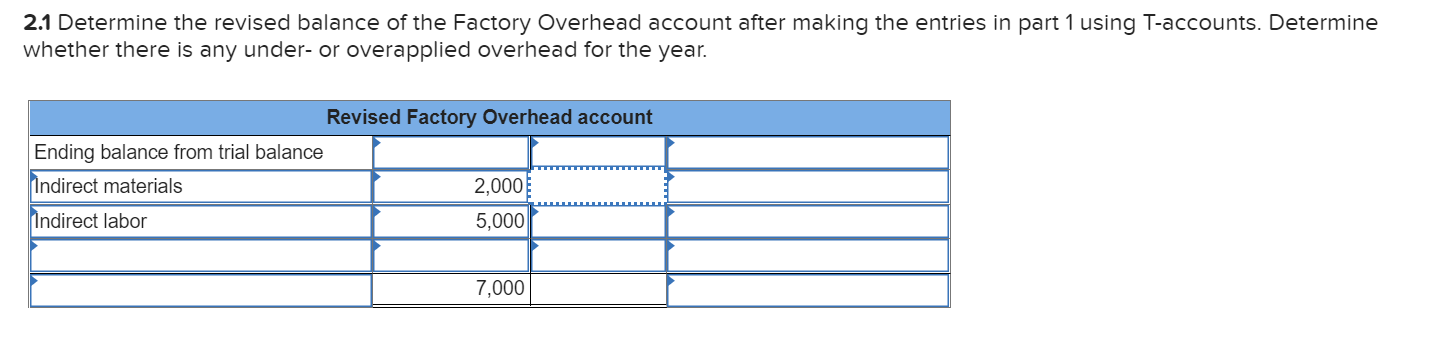

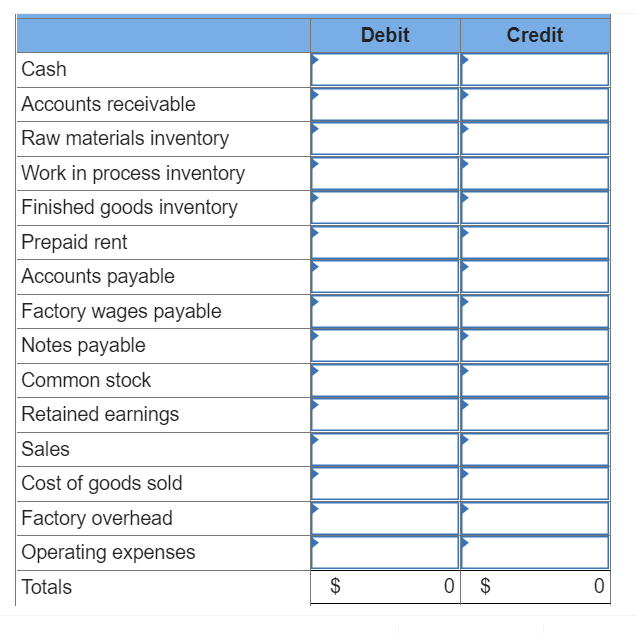

Bergamo Bay's computer system generated the following trial balance on December 31, 2017. The company's manager knows something is wrong with the trial balance because

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Core Concepts Of Accounting Information Systems

Authors: Nancy A. Bagranoff, Mark G. Simkin, Carolyn Strand Norman

11th Edition

9780470507025, 0470507020