Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Bette is enrolled in a employer-sponsored retirement plan. The estimated social security benefit is listed under other income. It is $1,300 per month.. Her employer

Bette is enrolled in a employer-sponsored retirement plan. The estimated social security benefit is listed under other income. It is $1,300 per month.. Her employer does not offer a pension plan .

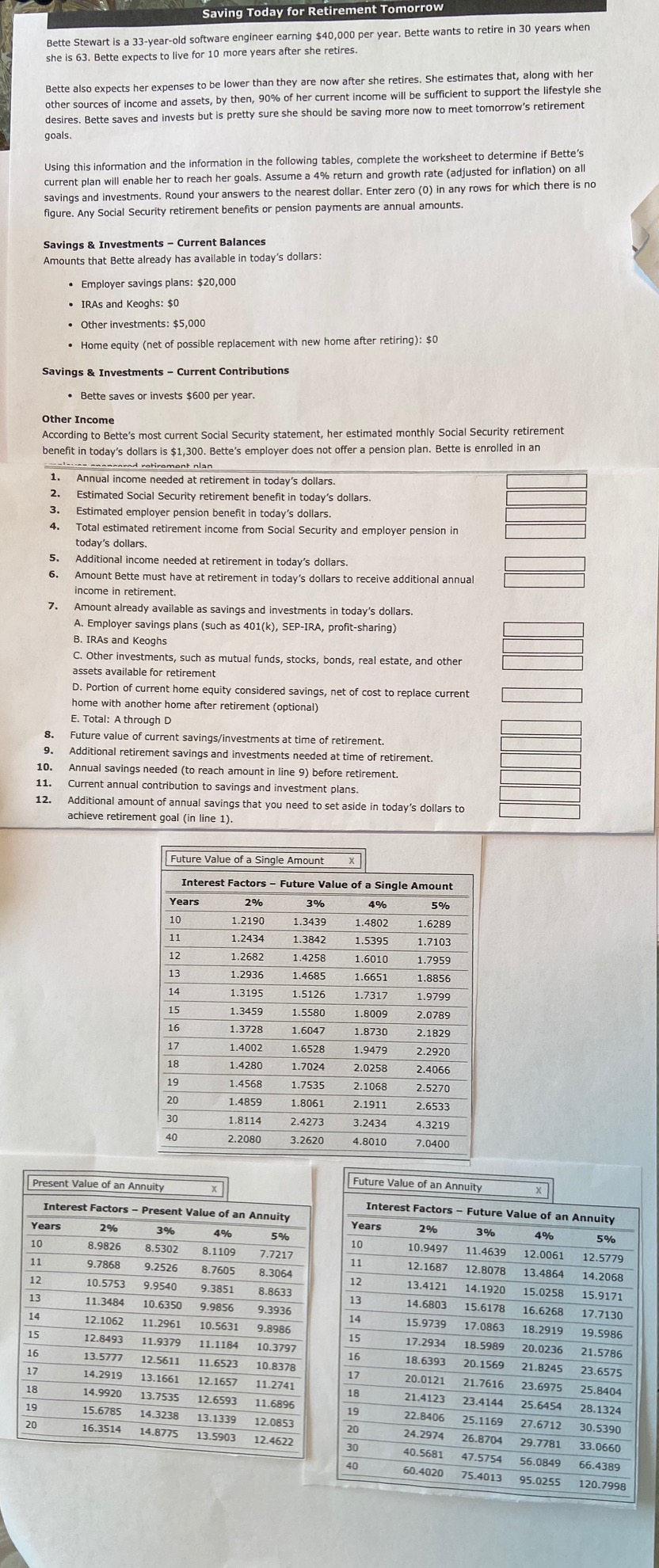

Saving Today for Retirement Tomorrow Bette Stewart is a 33-year-old software engineer earning $40,000 per year. Bette wants to retire in 30 years when she is 63. Bette expects to live for 10 more years after she retires. Bette also expects her expenses to be lower than they are now after she retires. She estimates that, along with her other sources of income and assets, by then, 90% of her current income will be sufficient to support the lifestyle she desires. Bette saves and invests but is pretty sure she should be saving more now to meet tomorrow's retirement goals. Using this information and the information in the following tables, complete the worksheet to determine if Bette's current plan will enable her to reach her goals. Assume a 4% return and growth rate (adjusted for inflation, on all savings and investments. Round your answers to the nearest dollar. Enter zero (0) in any rows for which there is no figure. Any Social Security retirement benefits or pension payments are annual amounts. Savings & Investments - Current Balances Amounts that Bette already has available in today's dollars: Employer savings plans: $20,000 IRAs and Keoghs: $0 Other investments: $5,000 Home equity (net of possible replacement with new home after retiring): $0 Savings & Investments - Current Contributions Bette saves or invests $600 per year. 2. Other Income According to Bette's most current Social Security statement, her estimated monthly Social Security retirement benefit in today's dollars is $1,300. Bette's employer does not offer a pension plan. Bette is enrolled in an A rotirement nlan 1. Annual income needed at retirement in today's dollars. Estimated Social Security retirement benefit in today's dollars. 3. Estimated employer pension benefit in today's dollars. 4. Total estimated retirement income from Social Security and employer pension in today's dollars. Additional income needed at retirement in today's dollars. Amount Bette must have at retirement in today's dollars to receive additional annual income in retirement. Amount already available as savings and investments in today's dollars. A. Employer savings plans (such as 401(k), SEP-IRA, profit-sharing) B. IRAs and Keoghs C. Other investments, such as mutual funds, stocks, bonds, real estate, and other assets available for retirement D. Portion of current home equity considered savings, net of cost to replace current home with another home after retirement (optional) E. Total: A through D Future value of current savings/investments at time of retirement. Additional retirement savings and investments needed at time of retirement. 10. Annual savings needed to reach amount in line 9) before retirement. 11. Current annual contribution to savings and investment plans. 12. Additional amount of annual savings that you need to set aside in today's dollars to achieve retirement goal (in line 1). 9. Future Value of a Single Amount x 11 Interest Factors - Future Value of a Single Amount Years 2% 3% 4% 5% 10 1.21901 .3439 1.4802 1.6289 1.2434 1.3842 1.5395 1.7103 1.2682 1.4258 1.6010 1.7959 1.2936 1.4685 1.6651 1.8856 1.3195 1.5126 1.7317 1.9799 1.3459 1 .5580 1.8009 2.0789 1.3728 1.6047 1.8730 2.1829 1.4002 1.6528 1.9479 2.2920 1.4280 1.7024 2.0258 2.4066 1.4568 1.7535 2.1068 2.5270 1.4859 1.8061 2.1911 2.6533 1.8114 2.4273 3.2434 4.3219 2.2080 3.2620 4.8010 7.0400 Present Value of an Annuity Future Value of an Annuity 14 Interest Factors - Present Value of an Annuity Years 2% 3% 4% 5% 10 8.9826 8.5302 8.11097.7217 9.7868 9.2526 8.7605 8.3064 10.5753 9.9540 9.3851 8.8633 11.3484 10.6350 9.9856 9.3936 12.1062 11.2961 10.5631 9.8986 15 12.8493 11.9379 11.1184 10.3797 13.5777 12.5611 11.6523 10.8378 17 14.291913.1661 12.1657 11.2741 18 14.9920 13.7535 12.6593 11.6896 19 15.6785 14.3238 13.1339 12.0853 20 16.3514 14.8775 13.5903 12.4622 Interest Factors - Future Value of an Annuity Years 2% 3% 4% 5% 10 10.9497 11.4639 12.0061 12.5779 11 12.1687 12.8078 13.4864 14.2068 12 13.4121 14.1920 15.0258 15.9171 14.6803 15.6178 16.6268 17.7130 14 15.9739 17.0863 18.2919 19.5986 15 17.2934 18.5989 20.0236 21.5786 18.6393 20.1569 21.8245 23.6575 20.0121 21.7616 23.6975 25.8404 21.4123 23.4144 25.6454 28.1324 22.8406 25.1169 27.6712 30.5390 24.2974 26.8704 29.7781 33.0660 40.5681 47.5754 56.084966.4389 60.4020 75.4013 95.0255 120.7998 16 16 40 Saving Today for Retirement Tomorrow Bette Stewart is a 33-year-old software engineer earning $40,000 per year. Bette wants to retire in 30 years when she is 63. Bette expects to live for 10 more years after she retires. Bette also expects her expenses to be lower than they are now after she retires. She estimates that, along with her other sources of income and assets, by then, 90% of her current income will be sufficient to support the lifestyle she desires. Bette saves and invests but is pretty sure she should be saving more now to meet tomorrow's retirement goals. Using this information and the information in the following tables, complete the worksheet to determine if Bette's current plan will enable her to reach her goals. Assume a 4% return and growth rate (adjusted for inflation, on all savings and investments. Round your answers to the nearest dollar. Enter zero (0) in any rows for which there is no figure. Any Social Security retirement benefits or pension payments are annual amounts. Savings & Investments - Current Balances Amounts that Bette already has available in today's dollars: Employer savings plans: $20,000 IRAs and Keoghs: $0 Other investments: $5,000 Home equity (net of possible replacement with new home after retiring): $0 Savings & Investments - Current Contributions Bette saves or invests $600 per year. 2. Other Income According to Bette's most current Social Security statement, her estimated monthly Social Security retirement benefit in today's dollars is $1,300. Bette's employer does not offer a pension plan. Bette is enrolled in an A rotirement nlan 1. Annual income needed at retirement in today's dollars. Estimated Social Security retirement benefit in today's dollars. 3. Estimated employer pension benefit in today's dollars. 4. Total estimated retirement income from Social Security and employer pension in today's dollars. Additional income needed at retirement in today's dollars. Amount Bette must have at retirement in today's dollars to receive additional annual income in retirement. Amount already available as savings and investments in today's dollars. A. Employer savings plans (such as 401(k), SEP-IRA, profit-sharing) B. IRAs and Keoghs C. Other investments, such as mutual funds, stocks, bonds, real estate, and other assets available for retirement D. Portion of current home equity considered savings, net of cost to replace current home with another home after retirement (optional) E. Total: A through D Future value of current savings/investments at time of retirement. Additional retirement savings and investments needed at time of retirement. 10. Annual savings needed to reach amount in line 9) before retirement. 11. Current annual contribution to savings and investment plans. 12. Additional amount of annual savings that you need to set aside in today's dollars to achieve retirement goal (in line 1). 9. Future Value of a Single Amount x 11 Interest Factors - Future Value of a Single Amount Years 2% 3% 4% 5% 10 1.21901 .3439 1.4802 1.6289 1.2434 1.3842 1.5395 1.7103 1.2682 1.4258 1.6010 1.7959 1.2936 1.4685 1.6651 1.8856 1.3195 1.5126 1.7317 1.9799 1.3459 1 .5580 1.8009 2.0789 1.3728 1.6047 1.8730 2.1829 1.4002 1.6528 1.9479 2.2920 1.4280 1.7024 2.0258 2.4066 1.4568 1.7535 2.1068 2.5270 1.4859 1.8061 2.1911 2.6533 1.8114 2.4273 3.2434 4.3219 2.2080 3.2620 4.8010 7.0400 Present Value of an Annuity Future Value of an Annuity 14 Interest Factors - Present Value of an Annuity Years 2% 3% 4% 5% 10 8.9826 8.5302 8.11097.7217 9.7868 9.2526 8.7605 8.3064 10.5753 9.9540 9.3851 8.8633 11.3484 10.6350 9.9856 9.3936 12.1062 11.2961 10.5631 9.8986 15 12.8493 11.9379 11.1184 10.3797 13.5777 12.5611 11.6523 10.8378 17 14.291913.1661 12.1657 11.2741 18 14.9920 13.7535 12.6593 11.6896 19 15.6785 14.3238 13.1339 12.0853 20 16.3514 14.8775 13.5903 12.4622 Interest Factors - Future Value of an Annuity Years 2% 3% 4% 5% 10 10.9497 11.4639 12.0061 12.5779 11 12.1687 12.8078 13.4864 14.2068 12 13.4121 14.1920 15.0258 15.9171 14.6803 15.6178 16.6268 17.7130 14 15.9739 17.0863 18.2919 19.5986 15 17.2934 18.5989 20.0236 21.5786 18.6393 20.1569 21.8245 23.6575 20.0121 21.7616 23.6975 25.8404 21.4123 23.4144 25.6454 28.1324 22.8406 25.1169 27.6712 30.5390 24.2974 26.8704 29.7781 33.0660 40.5681 47.5754 56.084966.4389 60.4020 75.4013 95.0255 120.7998 16 16 40Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Business Forecasting

Authors: John E. Hanke, Dean Wichern

9th edition

132301202, 978-0132301206