Answered step by step

Verified Expert Solution

Question

1 Approved Answer

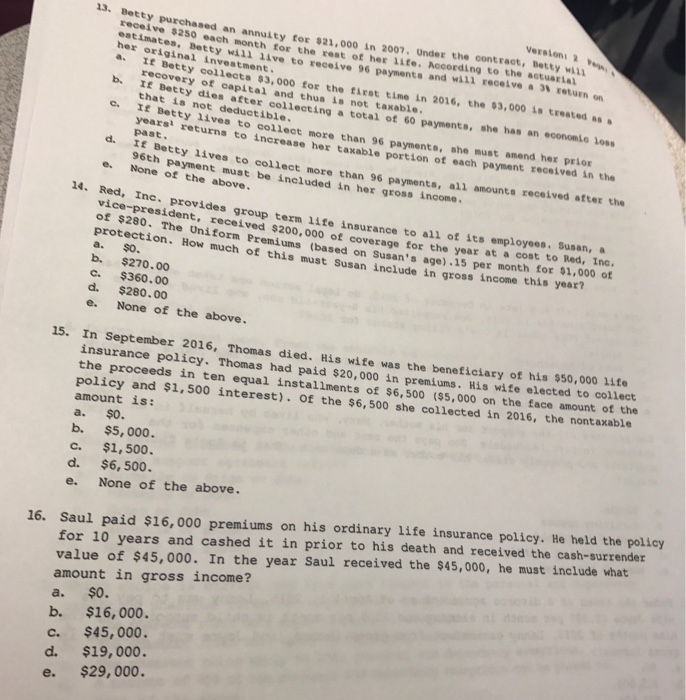

Betty purchased an annuity for $21,000 in 2007. Under the contract, Betty will receive $250 each month for the rest of her life. According to

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting A Key To Your Success In The Exam

Authors: Victoria Dobrynskaya

2nd Edition

3843389713, 978-3843389716