Answered step by step

Verified Expert Solution

Question

1 Approved Answer

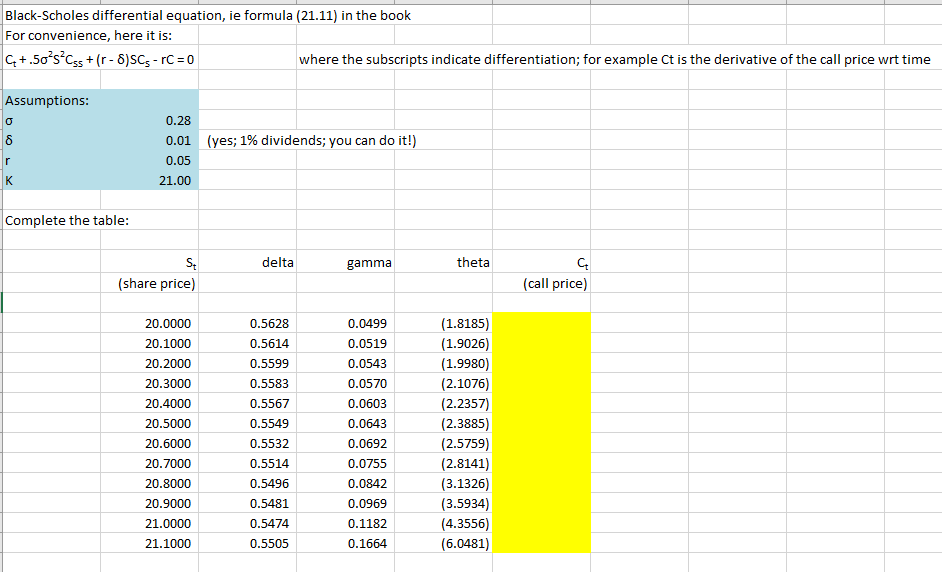

Black-Scholes differential equation, ie formula (21.11) in the book For convenience, here it is: 4+.5osCss + ir - 8)SC - rc = 0 where the

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Econometrics Modeling Market Microstructure Factor Models And Financial Risk Measures

Authors: G. Gregoriou , Razvan Pascalau

1st Edition

0230283624, 0230298109, 9780230283626, 9780230298101