Answered step by step

Verified Expert Solution

Question

1 Approved Answer

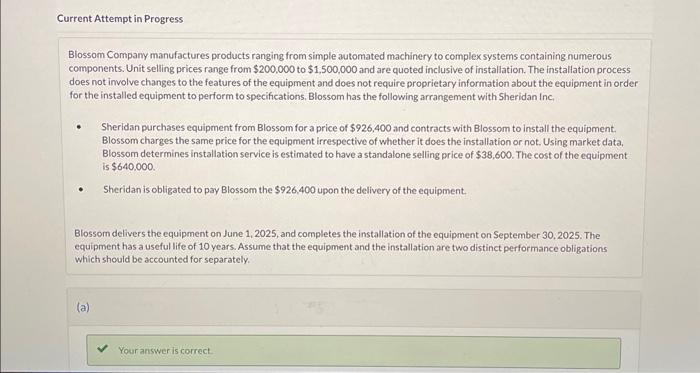

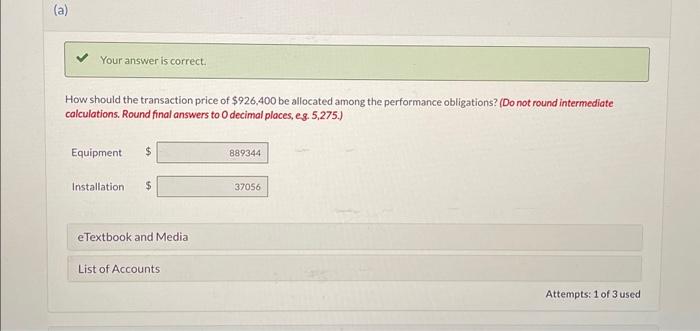

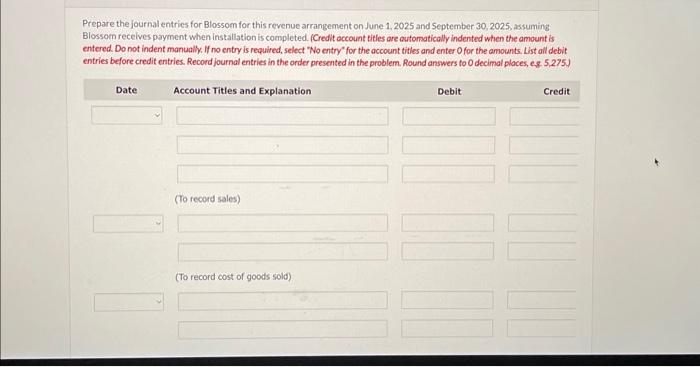

Blossom Company manufactures products ranging from simple automated machinery to complex systems containing numerous components. Unit selling prices range from $200,000 to $1,500,000 and are

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Transfer Pricing Audits In China

Authors: J. Li, A. Paisey

2007th Edition

0230001963, 978-0230001961