Answered step by step

Verified Expert Solution

Question

1 Approved Answer

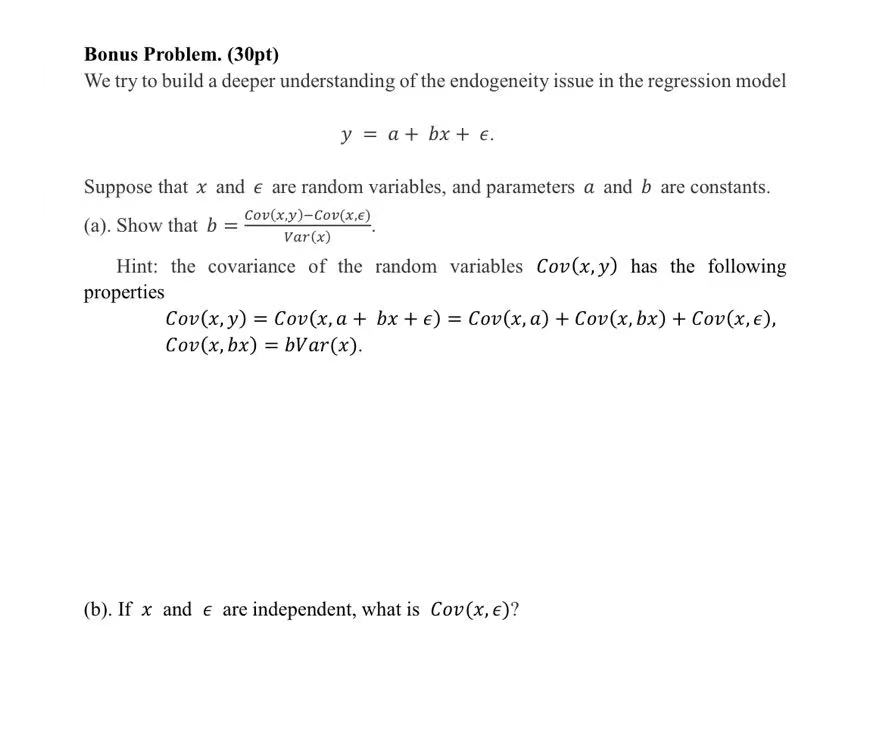

Bonus Problem. ( 3 0 pt ) We try to build a deeper understanding of the endogeneity issue in the regression model y = a

Bonus Problem. pt

We try to build a deeper understanding of the endogeneity issue in the regression model

Suppose that and are random variables, and parameters a and are constants.

a Show that

Hint: the covariance of the random variables Cov has the following

properties

CovCovCovCovCov

CovbVar

b If and are independent, what is Cov

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Management

Authors: Robert Kreitner, Charlene Cassidy

12th edition

1111221367, 978-1285225289, 1285225287, 978-1111221362