Answered step by step

Verified Expert Solution

Question

1 Approved Answer

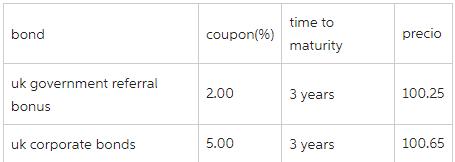

Both bonds pay interest annually. The current benchmark for the 3-year EUR interest rate swap is 2.12%. What is the G-spread in basis points for

Both bonds pay interest annually. The current benchmark for the 3-year EUR interest rate swap is 2.12%.

What is the G-spread in basis points for UK corporate bonds?

bond uk government referral bonus uk corporate bonds coupon(%) 2.00 5.00 time to maturity 3 years 3 years precio 100.25 100.65

Step by Step Solution

★★★★★

3.56 Rating (153 Votes )

There are 3 Steps involved in it

Step: 1

To calculate the Gspread in basis points for UK corporate bonds we need to compare their yield to th...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles of Finance

Authors: Scott Besley, Eugene F. Brigham

5th edition

1111527369, 978-1111527365