Answered step by step

Verified Expert Solution

Question

1 Approved Answer

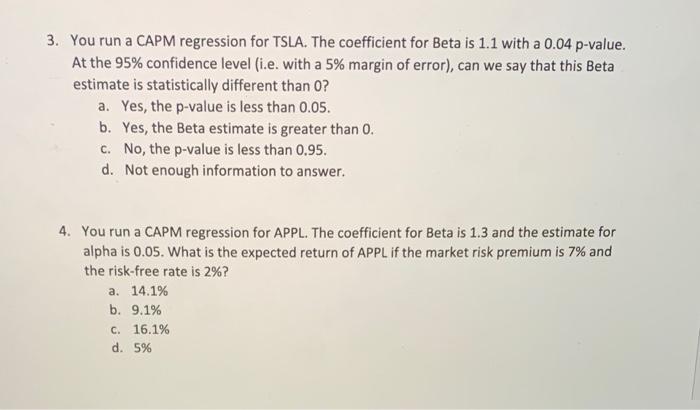

both questions please 3. You run a CAPM regression for TSLA. The coefficient for Beta is 1.1 with a 0.04-value. At the 95% confidence level

both questions please  3. You run a CAPM regression for TSLA. The coefficient for Beta is 1.1 with a 0.04-value. At the 95% confidence level (i.e. with a 5% margin of error), can we say that this Beta estimate is statistically different than 0 ? a. Yes, the p-value is less than 0.05. b. Yes, the Beta estimate is greater than 0 . c. No, the p-value is less than 0.95. d. Not enough information to answer. 4. You run a CAPM regression for APPL. The coefficient for Beta is 1.3 and the estimate for alpha is 0.05. What is the expected return of APPL if the market risk premium is 7% and the risk-free rate is 2% ? a. 14.1% b. 9.1% c. 16.1% d. 5%

3. You run a CAPM regression for TSLA. The coefficient for Beta is 1.1 with a 0.04-value. At the 95% confidence level (i.e. with a 5% margin of error), can we say that this Beta estimate is statistically different than 0 ? a. Yes, the p-value is less than 0.05. b. Yes, the Beta estimate is greater than 0 . c. No, the p-value is less than 0.95. d. Not enough information to answer. 4. You run a CAPM regression for APPL. The coefficient for Beta is 1.3 and the estimate for alpha is 0.05. What is the expected return of APPL if the market risk premium is 7% and the risk-free rate is 2% ? a. 14.1% b. 9.1% c. 16.1% d. 5%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of Recent Advances In Commodity And Financial Modeling

Authors: Giorgio Consigli, Silvana Stefani, Giovanni Zambruno

1st Edition

3319613189, 978-3319613185