Answered step by step

Verified Expert Solution

Question

1 Approved Answer

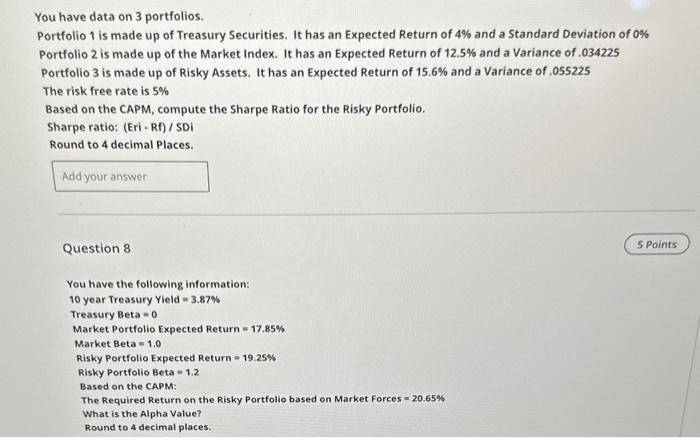

both ?s please You have data on 3 portfolios. Portfolio 1 is made up of Treasury Securities. It has an Expected Return of 4% and

both ?s please

You have data on 3 portfolios. Portfolio 1 is made up of Treasury Securities. It has an Expected Return of 4% and a Standard Deviation of 0\% Portfolio 2 is made up of the Market Index. It has an Expected Return of 12.5% and a Variance of.034225 Portfolio 3 is made up of Risky Assets. It has an Expected Return of 15.6% and a Variance of .055225 The risk free rate is 5% Based on the CAPM, compute the Sharpe Ratio for the Risky Portfolio. Sharpe ratio: (Eri-Rf) / SDi Round to 4 decimal Places. Question 8 You have the following information: 10 year Treasury Yield =3.87% Treasury Beta =0 Market Portfolio Expected Return =17.85% Market Beta =1.0 Risky Portfolio Expected Return =19.25% Risky Portfolio Beta =1.2 Based on the CAPM: The Required Return on the Risky Portfolio based on Market Forces =20.65% What is the Alpha Value? Round to 4 decimal places. You have data on 3 portfolios. Portfolio 1 is made up of Treasury Securities. It has an Expected Return of 4% and a Standard Deviation of 0\% Portfolio 2 is made up of the Market Index. It has an Expected Return of 12.5% and a Variance of.034225 Portfolio 3 is made up of Risky Assets. It has an Expected Return of 15.6% and a Variance of .055225 The risk free rate is 5% Based on the CAPM, compute the Sharpe Ratio for the Risky Portfolio. Sharpe ratio: (Eri-Rf) / SDi Round to 4 decimal Places. Question 8 You have the following information: 10 year Treasury Yield =3.87% Treasury Beta =0 Market Portfolio Expected Return =17.85% Market Beta =1.0 Risky Portfolio Expected Return =19.25% Risky Portfolio Beta =1.2 Based on the CAPM: The Required Return on the Risky Portfolio based on Market Forces =20.65% What is the Alpha Value? Round to 4 decimal places Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Ichimoku Charting And Technical Analysis

Authors: Charles G Koonitz

1st Edition

1989118739, 978-1989118733