BRAP Accounting Cycle (Step 8 & 9)

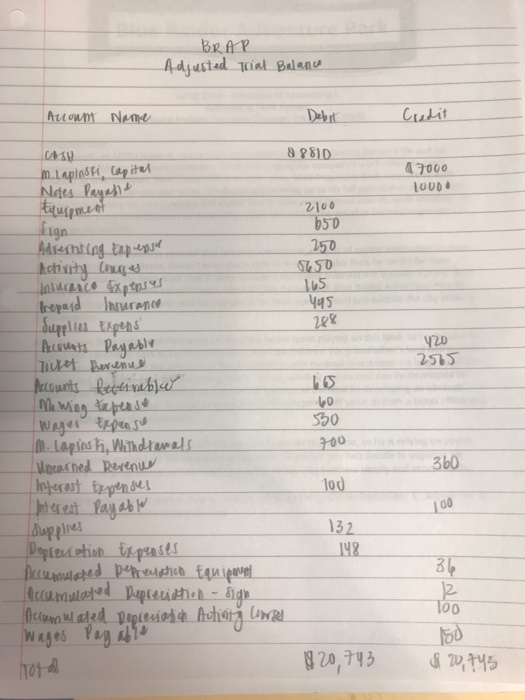

Chapter 4 (Accounting Cycle Steps 8 & 9) ACCOUNTING CYCLE STEP 8: Prepare journal entries to includes journalizing the closing entries in the general ledger accounts, using the cross-referen general journal and general ledger that you used in the previous steps al entries to close all the temporary accounts. This step sing entries in the general journal and posting them to the appropriate * using the cross-reference procedure described in Step 3. Use the same Helpful Hints The temporary accounts to be closed are the revenue accounts, expense accounts, and the owner's withdrawal (a.k.a. drawing) account. Note that the owner's capital account before the closing process does not equal the ending owner's capital we reported on the statement of owner's equity and on the balance sheet. The closing process, when properly completed, will update the owner's capital account balance in the general ledger so that it reconciles with the ending owner's equity balance we reported on the Tinancial statements. The closing process will also reduce all temporary accounts to a zero balance clearing the way for the accumulation of revenues, expenses, and withdrawals for the next accounting period. Revenue accounts must be DEBITED to remove their credit balances and expense accounts and the owner's withdrawal account must be CREDITED to remove their debit balances. ACCOUNTING CYCLE STEP 9: Prepare a post-closing trial balance. Just like the unadjusted trial balance and the adjusted trial balance, this trial balance is simply a listing of the general ledger accounts and their balances in financial statement order with the debit and credit columns summed. See Exhibit 4.6 in your textbook for an example of a post-closing trial balance. No working papers been provided for this step, so you may either handwrite your solution or prepare it electronically. If you prepare your solution electronically, be sure to bring a hardcopy to class Helpful Hints This trial balance confirms that general ledger debits and credits are equal before beginning a new accounting cycle. Given that all the temporary account balances were reduced to zero during the closing process, the temporary accounts may be omitted from this trial balance. Check Figure: Debits and Credits must each equal $18,502. ACCOUNTING CYCLE STEP 10: Preparing reversing entries is an optional step in the accounting cycle that will not be covered in this course. BRAP Adjusted Trial Balance Aunt Name Credit 47000 LOUD 288 20 255 AH 8 8810 m. Lapinski, capital Notes Payable tquipment 2100 Sign 650 Hechting tapeysur 250 Activ Cours 750 Inbuc Sxpenses 165 krepad Thawana 495 dupplies Expens' Accounts Payably Ticket Revenue Accounts Receivable Mi Wing tubes 60 Wager Expenso Lapin h Withdrawals Unearned Revenue Interest txpenses 100 Interest Payable Supplies 132 Depreciation Expenses Decumuloped Depression Equipment famuloped Depreidhol - Side fuumwated Vepievielio Autiera cunees Wages Payable 820,743 530 700 360 00 148 27 150 Total $20,743