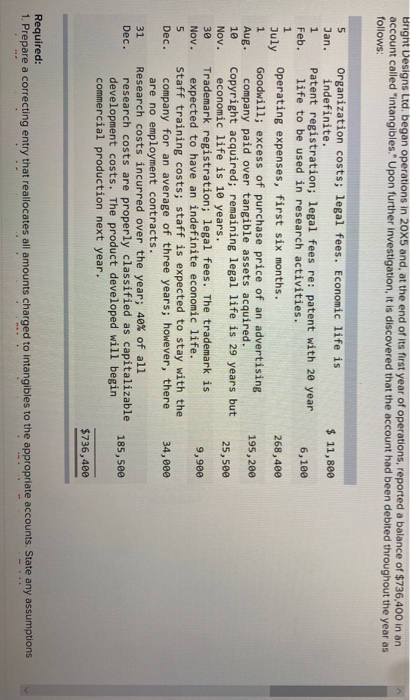

Bright Designs Ltd, began operations in 2005 and, at the end of its first year of operations, reported a balance of $736,400 in an account called "intangibles." Upon further investigation, it is discovered that the account had been debited throughout the year as follows: 5 Jan. 1 Feb. 1 July 1 Aug. 10 Nov. 30 Nov. 5 Dec. Organization costs; legal fees. Economic life is indefinite. $ 11,800 Patent registration; legal fees re: patent with 20 year life to be used in research activities. 6,100 Operating expenses, first six months. 268,400 Goodwill; excess of purchase price of an advertising company paid over tangible assets acquired. 195, 200 Copyright acquired; remaining legal life is 29 years but economic life is 10 years. 25,500 Trademark registration; legal fees. The trademark is expected to have an indefinite economic life. 9,980 Staff training costs; staff is expected to stay with the company for an average of three years; however, there 34,000 are no employment contracts. Research costs incurred over the year; 40% of all research costs are properly classified as capitalizable 185,500 development costs. The product developed will begin commercial production next year. $736,400 31 Dec. Required: 1. Prepare a correcting entry that reallocates all amounts charged to intangibles to the appropriate accounts. State any assumptions 2. Calculate amortization expense on intangible assets for 20X5. Straight-line amortization, to the exact month of purchase, is used. All residual values are expected to be zero. (Round your answers to the nearest whole dollars.) 20x5 Amortization expense: Bright Designs Ltd, began operations in 2005 and, at the end of its first year of operations, reported a balance of $736,400 in an account called "intangibles." Upon further investigation, it is discovered that the account had been debited throughout the year as follows: 5 Jan. 1 Feb. 1 July 1 Aug. 10 Nov. 30 Nov. 5 Dec. Organization costs; legal fees. Economic life is indefinite. $ 11,800 Patent registration; legal fees re: patent with 20 year life to be used in research activities. 6,100 Operating expenses, first six months. 268,400 Goodwill; excess of purchase price of an advertising company paid over tangible assets acquired. 195, 200 Copyright acquired; remaining legal life is 29 years but economic life is 10 years. 25,500 Trademark registration; legal fees. The trademark is expected to have an indefinite economic life. 9,980 Staff training costs; staff is expected to stay with the company for an average of three years; however, there 34,000 are no employment contracts. Research costs incurred over the year; 40% of all research costs are properly classified as capitalizable 185,500 development costs. The product developed will begin commercial production next year. $736,400 31 Dec. Required: 1. Prepare a correcting entry that reallocates all amounts charged to intangibles to the appropriate accounts. State any assumptions 2. Calculate amortization expense on intangible assets for 20X5. Straight-line amortization, to the exact month of purchase, is used. All residual values are expected to be zero. (Round your answers to the nearest whole dollars.) 20x5 Amortization expense