Answered step by step

Verified Expert Solution

Question

1 Approved Answer

but this is an investment subject (a) As an analyst in Bulls and Bear Investment Company, you have derived the following information about 3 securities

but this is an investment subject

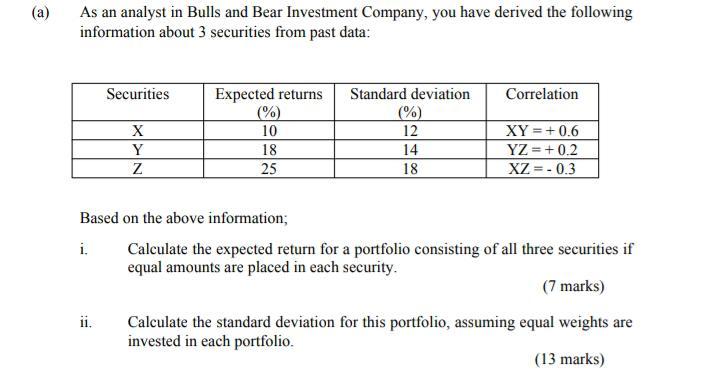

(a) As an analyst in Bulls and Bear Investment Company, you have derived the following information about 3 securities from past data: Securities Correlation Expected returns (% 10 18 X Y Z Standard deviation (%) 12 14 18 XY = + 0.6 YZ = +0.2 XZ=-0.3 25 Based on the above information; i. Calculate the expected return for a portfolio consisting of all three securities if equal amounts are placed in each security. (7 marks) ii. Calculate the standard deviation for this portfolio, assuming equal weights are invested in each portfolio. (13 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Organic Farmers Business Handbook A Complete Guide To Managing Finances Crops And Staff And Making A Profit

Authors: Richard Wiswall

1st Edition

1603581421, 978-1603581424