Answered step by step

Verified Expert Solution

Question

1 Approved Answer

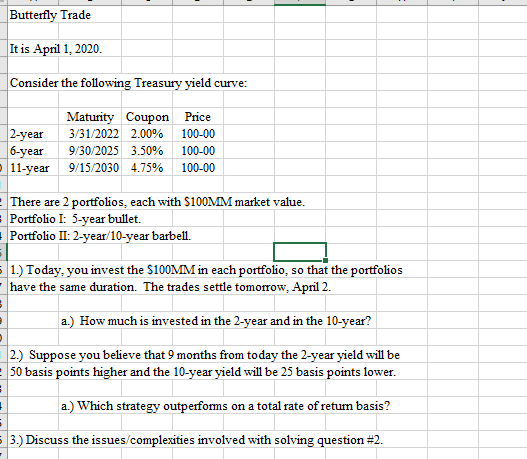

Butterfly Trade It is April 1, 2020. Consider the following Treasury yield curve: 2-year 6-year 11-year Maturity Coupon 3/31/2022 2.00% 9/30/2025 3.50% 9/15/2030 4.75% Price

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Institutions Management A Risk Management Approach

Authors: Marcia Cornett, Patricia McGraw, Anthony Saunders

8th edition

978-0078034800, 78034809, 978-0071051590