Answered step by step

Verified Expert Solution

Question

1 Approved Answer

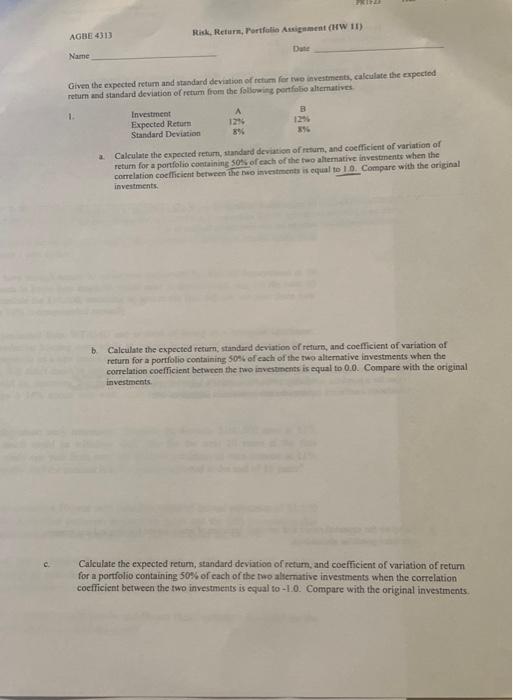

C. AGBE 4313 Name 1. Given the expected return and standard deviation of return for two investments, calculate the expected return and standard deviation of

C. AGBE 4313 Name 1. Given the expected return and standard deviation of return for two investments, calculate the expected return and standard deviation of return from the following portfolio alternatives. b. Risk, Return, Portfolio Assignment (HW 11) a. Investment Expected Return Standard Deviation Date A 12% 8% B 12% 8% Calculate the expected return, standard deviation of return, and coefficient of variation of return for a portfolio containing 50% of each of the two alternative investments when the correlation coefficient between the two investments is equal to 1.0. Compare with the original investments. Calculate the expected return, standard deviation of return, and coefficient of variation of return for a portfolio containing 50% of each of the two alternative investments when the correlation coefficient between the two investments is equal to 0.0. Compare with the original investments. Calculate the expected return, standard deviation of return, and coefficient of variation of return for a portfolio containing 50% of each of the two alternative investments when the correlation coefficient between the two investments is equal to -1.0. Compare with the original investments.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Millionaire By Thirty The Quickest Path To Early Financial Independence

Authors: Douglas R. Andrew, Emron Andrew, Aaron Andrew

1st Edition

0446501840, 978-0446501842