Question

c. Demonstrate how you can use bonds A, B and Cto replace a 3-year zero coupon bond with a face value of $1000. d. IF

c. Demonstrate how you can use bonds A, B and Cto replace a 3-year zero coupon bond with a face value of $1000.

d. IF the 3-year zero coupon bond in c has a market price of $780. Show how you can earn an arbitrage profit. Make sure to provide clesr detail on the arbitrage strategy.

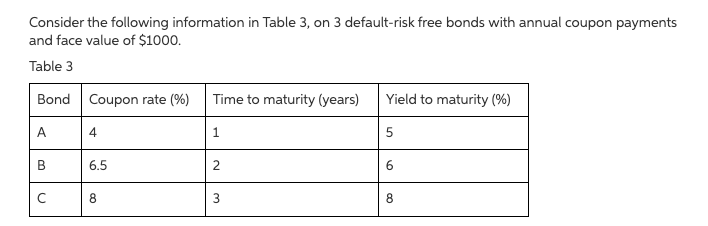

Consider the following information in Table 3, on 3 default-risk free bonds with annual coupon payments and face value of $1000. Table 3 Bond Coupon rate (%) Time to maturity (years) Yield to maturity (%) A A 4 1 5 B 6.5 2 6 8 3 00 Consider the following information in Table 3, on 3 default-risk free bonds with annual coupon payments and face value of $1000. Table 3 Bond Coupon rate (%) Time to maturity (years) Yield to maturity (%) A A 4 1 5 B 6.5 2 6 8 3 00Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Satoshi S Vision The Art Of Bitcoin

Authors: Craig Wright ,Paul Democritou

1st Edition

1688735925, 978-1688735927