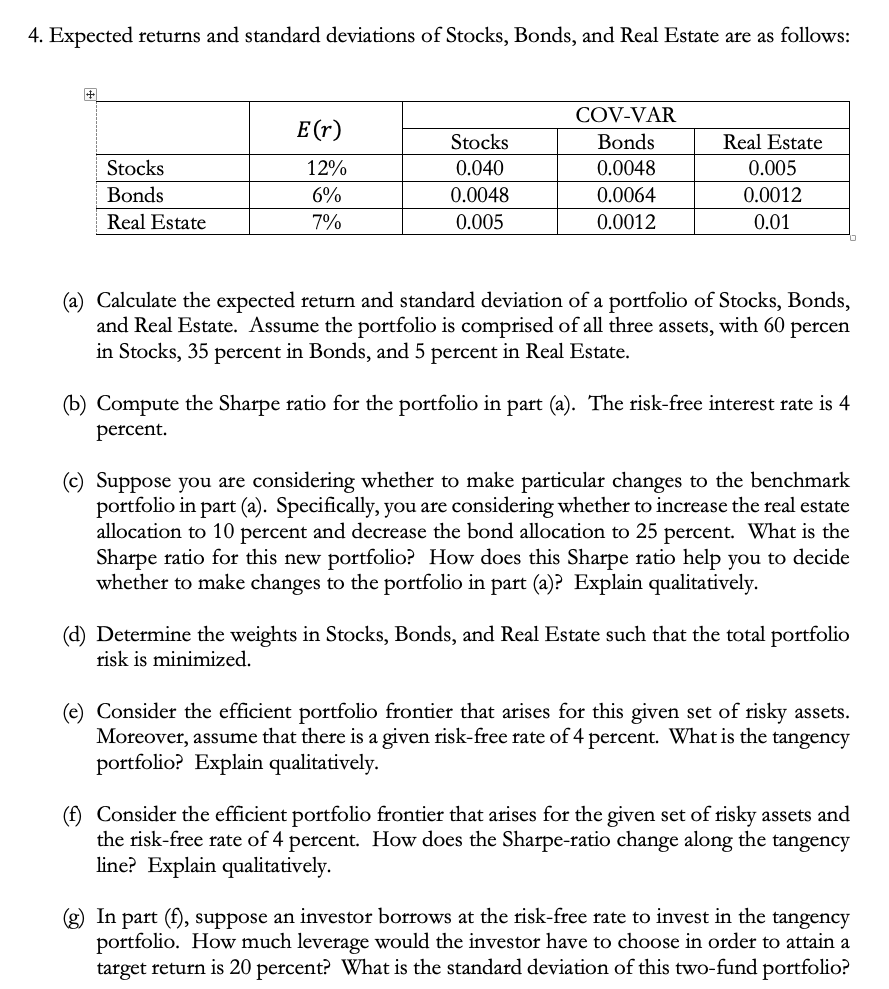

Question

(c) Suppose you are considering whether to make particular changes to the benchmark portfolio in part (a). Specifically, you are considering whether to increase the

(c) Suppose you are considering whether to make particular changes to the benchmark portfolio in part (a). Specifically, you are considering whether to increase the real estate allocation to 10 percent and decrease the bond allocation to 25 percent. What is the Sharpe ratio for this new portfolio? How does this Sharpe ratio help you to decide whether to make changes to the portfolio in part (a)? Explain qualitatively.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Behavioral Finance And Investor Types

Authors: Michael M. Pompian

1st Edition

1118011503, 978-1118011508