Answered step by step

Verified Expert Solution

Question

1 Approved Answer

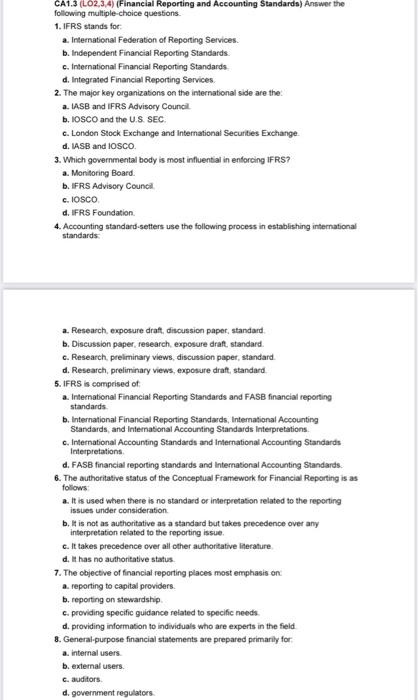

CA1.3 (L02.3.4) (Financial Reporting and Accounting Standards) Answer the following multiple-choice questions 1. IFRS stands for a. International Federation of Reporting Services b. Independent Financial

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Will You Be My Internal Audit Manager

Authors: Benito Gross

1st Edition

B09774C8CK, 979-8521636563