Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Calculate and complete the tables for the following 3 holding period scenarios ( 5 , 1 1 . 5 , and 2 7 years )

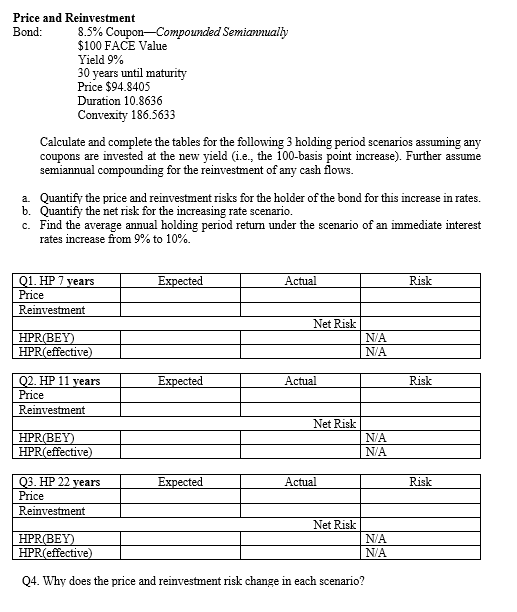

Calculate and complete the tables for the following holding period scenarios and years assuming any coupons are invested at the new yield ie the basis point increase and the bond is sold at this new yield. Further assume semiannual compounding for the reinvestment of any cash flows.

a Quantify the price and reinvestment risks for the holder of the bond for this increase in rates.

b Quantify the net risk for the increasing rate scenario.

c Find the holding period returns under the scenario of an immediate interest rates increase from to

Price and Reinvestment

Bond: CouponCompounded Semiannually

$ FACE Value

Yield

years until maturity

Price $

Duration

Convexity

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial management theory and practice

Authors: Eugene F. Brigham and Michael C. Ehrhardt

12th Edition

978-0030243998, 30243998, 324422695, 978-0324422696