Answered step by step

Verified Expert Solution

Question

1 Approved Answer

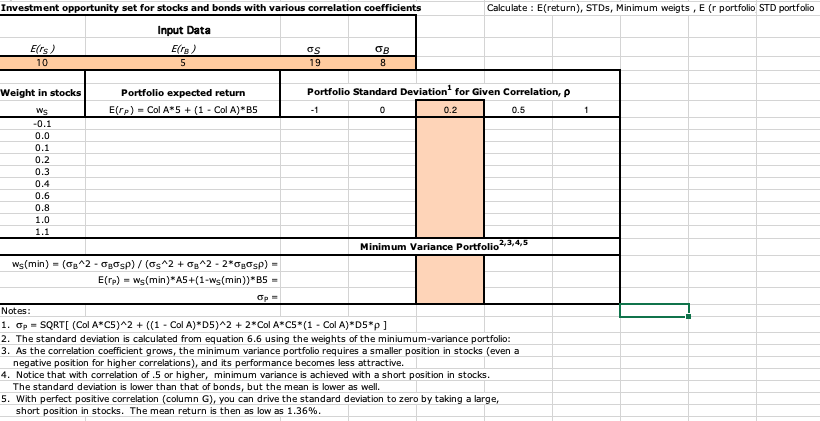

Calculate : E(return), STDs, Minimum weigts, E (r portfolio STD portfolio Investment opportunity set for stocks and bonds with various correlation coefficients Input Data Elts)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Bitcoins Investment

Authors: Paulita Kingrey

1st Edition

979-8353894094