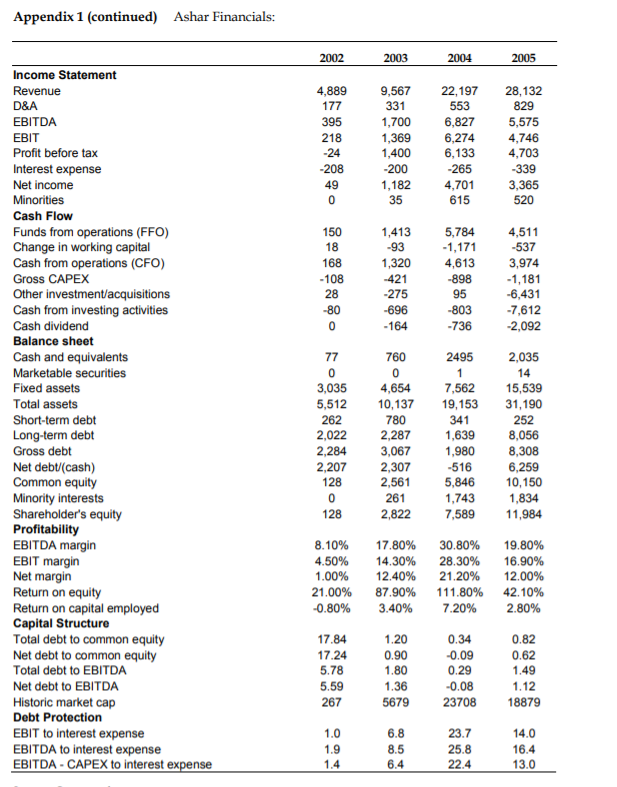

calculate the expected loss, economic revenue and economic profit for both proposals Ashar Industries (Ashar)

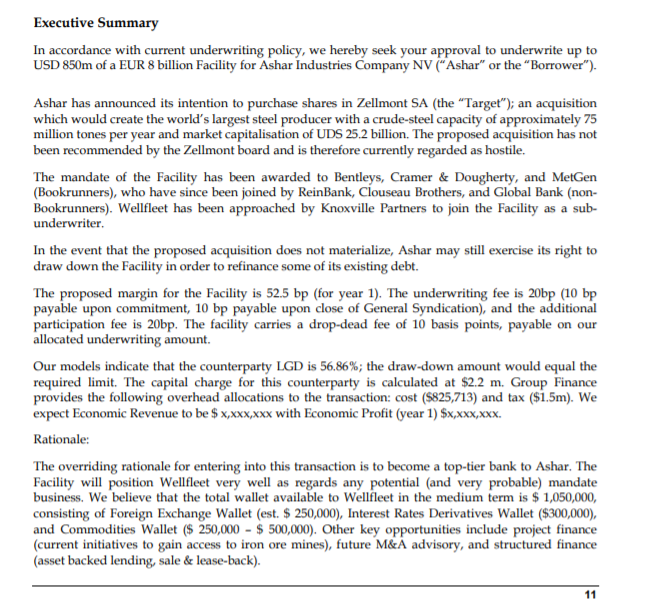

Executive Summary In accordance with current underwriting policy, we hereby seek your approval to underwrite up to USD 850m of a EUR 8 billion Facility for Ashar Industries Company NV ("Ashar" or the "Borrower"). Ashar has announced its intention to purchase shares in Zellmont SA (the Target"); an acquisition which would create the world's largest steel producer with a crude-steel capacity of approximately 75 million tones per year and market capitalisation of UDS 25.2 billion. The proposed acquisition has not been recommended by the Zellmont board and is therefore currently regarded as hostile. The mandate of the Facility has been awarded to Bentleys, Cramer & Dougherty, and MetGen (Bookrunners), who have since been joined by ReinBank, Clouseau Brothers, and Global Bank (non- Bookrunners). Wellfleet has been approached by Knoxville Partners to join the Facility as a sub- underwriter. In the event that the proposed acquisition does not materialize, Ashar may still exercise its right to draw down the Facility in order to refinance some of its existing debt. The proposed margin for the Facility is 52.5 bp (for year 1). The underwriting fee is 20bp (10 bp payable upon commitment, 10 bp payable upon close of General Syndication), and the additional participation fee is 20bp. The facility carries a drop-dead fee of 10 basis points, payable on our allocated underwriting amount. Our models indicate that the counterparty LGD is 56.86%; the draw-down amount would equal the required limit. The capital charge for this counterparty is calculated at $2.2 m. Group Finance provides the following overhead allocations to the transaction: cost (S825,713) and tax ($1.5m). We expect Economic Revenue to be $ x,xxx,xxx with Economic Profit (year 1) $x,XXX,XXX. Rationale: The overriding rationale for entering into this transaction is to become a top-tier bank to Ashar. The Facility will position Wellfleet very well as regards any potential (and very probable) mandate business. We believe that the total wallet available to Wellfleet in the medium term is $ 1,050,000, consisting of Foreign Exchange Wallet (est. $ 250,000), Interest Rates Derivatives Wallet ($300,000), and Commodities Wallet ($ 250,000 - $ 500,000). Other key opportunities include project finance (current initiatives to gain access to iron ore mines), future M&A advisory, and structured finance (asset backed lending, sale & lease-back). 11 Appendix 1 (continued) Ashar Financials: 2002 2003 2004 2005 4,889 177 395 218 -24 -208 49 0 9,567 331 1,700 1,369 1,400 -200 1,182 35 22,197 553 6,827 6,274 6,133 -265 4,701 615 28,132 829 5,575 4,746 4,703 -339 3,365 520 150 18 168 - 108 28 -80 0 1,413 -93 1,320 -421 -275 -696 -164 5,784 -1,171 4,613 -898 95 -803 -736 4,511 -537 3,974 -1,181 -6,431 -7,612 -2,092 Income Statement Revenue D&A EBITDA EBIT Profit before tax Interest expense Net income Minorities Cash Flow Funds from operations (FFO) Change in working capital Cash from operations (CFO) Gross CAPEX Other investment/acquisitions Cash from investing activities Cash dividend Balance sheet Cash and equivalents Marketable securities Fixed assets Total assets Short-term debt Long-term debt Gross debt Net debt(cash) Common equity Minority interests Shareholder's equity Profitability EBITDA margin EBIT margin Net margin Return on equity Return on capital employed Capital Structure Total debt to common equity Net debt to common equity Total debt to EBITDA Net debt to EBITDA Historic market cap Debt Protection EBIT to interest expense EBITDA to interest expense EBITDA-CAPEX to interest expense 77 0 3,035 5,512 262 2,022 2,284 2,207 128 0 128 760 0 4,654 10,137 780 2,287 3,067 2,307 2,561 261 2,822 2495 1 7,562 19,153 341 1,639 1,980 -516 5,846 1,743 7,589 2,035 14 15,539 31,190 252 8,056 8,308 6,259 10,150 1,834 11,984 8.10% 4.50% 1.00% 21.00% -0.80% 17.80% 14.30% 12.40% 87.90% 3.40% 30.80% 19.80% 28.30% 16.90% 21.20% 12.00% 111.80% 42.10% 7.20% 2.80% 17.84 17.24 5.78 5.59 267 1.20 0.90 1.80 1.36 5679 0.34 -0.09 0.29 -0.08 23708 0.82 0.62 1.49 1.12 18879 1.0 1.9 1.4 6.8 8.5 6.4 23.7 25.8 22.4 14.0 16.4 13.0 Executive Summary In accordance with current underwriting policy, we hereby seek your approval to underwrite up to USD 850m of a EUR 8 billion Facility for Ashar Industries Company NV ("Ashar" or the "Borrower"). Ashar has announced its intention to purchase shares in Zellmont SA (the Target"); an acquisition which would create the world's largest steel producer with a crude-steel capacity of approximately 75 million tones per year and market capitalisation of UDS 25.2 billion. The proposed acquisition has not been recommended by the Zellmont board and is therefore currently regarded as hostile. The mandate of the Facility has been awarded to Bentleys, Cramer & Dougherty, and MetGen (Bookrunners), who have since been joined by ReinBank, Clouseau Brothers, and Global Bank (non- Bookrunners). Wellfleet has been approached by Knoxville Partners to join the Facility as a sub- underwriter. In the event that the proposed acquisition does not materialize, Ashar may still exercise its right to draw down the Facility in order to refinance some of its existing debt. The proposed margin for the Facility is 52.5 bp (for year 1). The underwriting fee is 20bp (10 bp payable upon commitment, 10 bp payable upon close of General Syndication), and the additional participation fee is 20bp. The facility carries a drop-dead fee of 10 basis points, payable on our allocated underwriting amount. Our models indicate that the counterparty LGD is 56.86%; the draw-down amount would equal the required limit. The capital charge for this counterparty is calculated at $2.2 m. Group Finance provides the following overhead allocations to the transaction: cost (S825,713) and tax ($1.5m). We expect Economic Revenue to be $ x,xxx,xxx with Economic Profit (year 1) $x,XXX,XXX. Rationale: The overriding rationale for entering into this transaction is to become a top-tier bank to Ashar. The Facility will position Wellfleet very well as regards any potential (and very probable) mandate business. We believe that the total wallet available to Wellfleet in the medium term is $ 1,050,000, consisting of Foreign Exchange Wallet (est. $ 250,000), Interest Rates Derivatives Wallet ($300,000), and Commodities Wallet ($ 250,000 - $ 500,000). Other key opportunities include project finance (current initiatives to gain access to iron ore mines), future M&A advisory, and structured finance (asset backed lending, sale & lease-back). 11 Appendix 1 (continued) Ashar Financials: 2002 2003 2004 2005 4,889 177 395 218 -24 -208 49 0 9,567 331 1,700 1,369 1,400 -200 1,182 35 22,197 553 6,827 6,274 6,133 -265 4,701 615 28,132 829 5,575 4,746 4,703 -339 3,365 520 150 18 168 - 108 28 -80 0 1,413 -93 1,320 -421 -275 -696 -164 5,784 -1,171 4,613 -898 95 -803 -736 4,511 -537 3,974 -1,181 -6,431 -7,612 -2,092 Income Statement Revenue D&A EBITDA EBIT Profit before tax Interest expense Net income Minorities Cash Flow Funds from operations (FFO) Change in working capital Cash from operations (CFO) Gross CAPEX Other investment/acquisitions Cash from investing activities Cash dividend Balance sheet Cash and equivalents Marketable securities Fixed assets Total assets Short-term debt Long-term debt Gross debt Net debt(cash) Common equity Minority interests Shareholder's equity Profitability EBITDA margin EBIT margin Net margin Return on equity Return on capital employed Capital Structure Total debt to common equity Net debt to common equity Total debt to EBITDA Net debt to EBITDA Historic market cap Debt Protection EBIT to interest expense EBITDA to interest expense EBITDA-CAPEX to interest expense 77 0 3,035 5,512 262 2,022 2,284 2,207 128 0 128 760 0 4,654 10,137 780 2,287 3,067 2,307 2,561 261 2,822 2495 1 7,562 19,153 341 1,639 1,980 -516 5,846 1,743 7,589 2,035 14 15,539 31,190 252 8,056 8,308 6,259 10,150 1,834 11,984 8.10% 4.50% 1.00% 21.00% -0.80% 17.80% 14.30% 12.40% 87.90% 3.40% 30.80% 19.80% 28.30% 16.90% 21.20% 12.00% 111.80% 42.10% 7.20% 2.80% 17.84 17.24 5.78 5.59 267 1.20 0.90 1.80 1.36 5679 0.34 -0.09 0.29 -0.08 23708 0.82 0.62 1.49 1.12 18879 1.0 1.9 1.4 6.8 8.5 6.4 23.7 25.8 22.4 14.0 16.4 13.0