Answered step by step

Verified Expert Solution

Question

1 Approved Answer

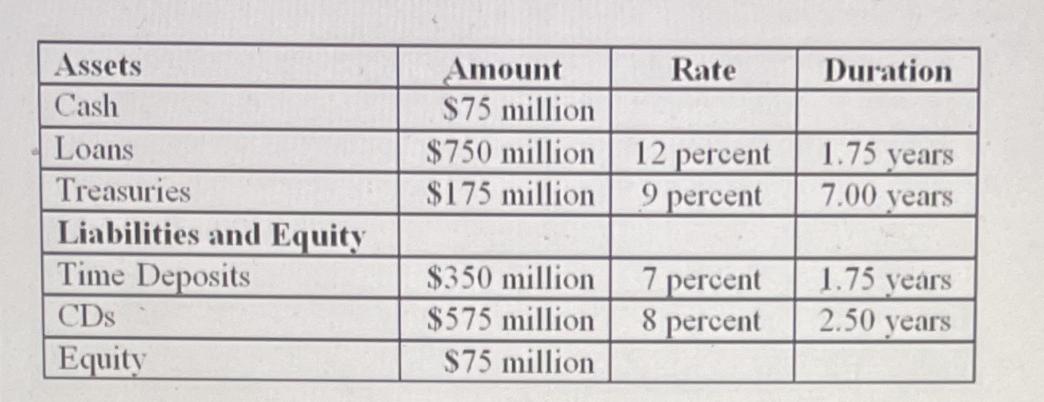

Calculate the leverage-adjusted duration gap to four decimal places and state the FI's interest rate risk exposure of this institution. Assets Cash Loans Treasuries

Calculate the leverage-adjusted duration gap to four decimal places and state the FI's interest rate risk exposure of this institution. Assets Cash Loans Treasuries Liabilities and Equity Time Deposits CDs Equity Amount $75 million $750 million $175 million $350 million $575 million $75 million Rate 12 percent 9 percent 7 percent 8 percent Duration 1.75 years 7.00 years 1.75 years 2.50 years

Step by Step Solution

★★★★★

3.42 Rating (155 Votes )

There are 3 Steps involved in it

Step: 1

To calculate the leverageadjusted duration gap we need to first calculate the duration gap and the e...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Institutions Management A Risk Management Approach

Authors: Marcia Cornett, Patricia McGraw, Anthony Saunders

8th edition

978-0078034800, 78034809, 978-0071051590