Answered step by step

Verified Expert Solution

Question

1 Approved Answer

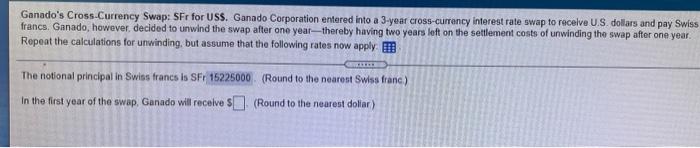

Calculate Years 1-3 Ganado's Cross-Currency Swap: SFr for USS. Ganado Corporation entered into a 3-year cross-currency interest rate swap to receive U.S. dollars and pay

Calculate Years 1-3

Ganado's Cross-Currency Swap: SFr for USS. Ganado Corporation entered into a 3-year cross-currency interest rate swap to receive U.S. dollars and pay Swiss francs. Ganado, however, decided to unwind the swap after one year--thereby having two years left on the settlement costs of unwinding the swap after one year Repeat the calculations for unwinding, but assume that the following rates now apply. The notional principal in Swiss francs is SF 15225000). (Round to the nearest Swiss franc) In the first year of the swap, Ganado will receive 5 (Round to the nearest dollar) Assumptioms Notional principal Original spot rate (SFr/S) New (1-year later) spot (SF/5) New fixed US$ interest New fixed Swiss franc interest Values $10,500,000 1.4500 1.5000 5.20% 2.50% Swap Rates Original US dollar Original Swiss franc 3-Year Bid 5.56% 1.93% 3-Year Ask 5.59% 2.01% Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Real Estate Management Course The Fundamentals Of Real Estate Management

Authors: Maureen Green

1st Edition

979-8395764010