Campbell, Inc. produces and sells outdoor equipment. On July 1, Year 1, Campbell, Inc. issued $73,900,000 of 10-year, 9% bonds at a market (effective) interest rate of 7%, receiving cash of $84,403,259. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year.

Required:

| 1. | Journalize the entry to record the amount of cash proceeds from the issuance of the bonds.* |

| 2. | Journalize the entries to record the following:* | a. | The first semiannual interest payment on December 31, Year 1, and the amortization of the bond premium, using the interest method. (Round to the nearest dollar.) | | b. | The interest payment on June 30, Year 2, and the amortization of the bond premium, using the interest method. (Round to the nearest dollar.) | |

| 3. | Determine the total interest expense for Year 1. | | *Refer to the Chart of Accounts for exact wording of account titles. | |

| CHART OF ACCOUNTS |

| Campbell, Inc. |

| General Ledger |

| | ASSETS | | 110 | Cash | | 111 | Petty Cash | | 121 | Accounts Receivable | | 122 | Allowance for Doubtful Accounts | | 126 | Interest Receivable | | 127 | Notes Receivable | | 131 | Merchandise Inventory | | 141 | Office Supplies | | 142 | Store Supplies | | 151 | Prepaid Insurance | | 191 | Land | | 192 | Store Equipment | | 193 | Accumulated Depreciation-Store Equipment | | 194 | Office Equipment | | 195 | Accumulated Depreciation-Office Equipment | | | LIABILITIES | | 210 | Accounts Payable | | 221 | Salaries Payable | | 231 | Sales Tax Payable | | 232 | Interest Payable | | 241 | Notes Payable | | 251 | Bonds Payable | | 252 | Discount on Bonds Payable | | 253 | Premium on Bonds Payable | | | EQUITY | | 311 | Common Stock | | 312 | Paid-In Capital in Excess of Par-Common Stock | | 315 | Treasury Stock | | 321 | Preferred Stock | | 322 | Paid-In Capital in Excess of Par-Preferred Stock | | 331 | Paid-In Capital from Sale of Treasury Stock | | 340 | Retained Earnings | | 351 | Cash Dividends | | 352 | Stock Dividends | | 390 | Income Summary | | | | REVENUE | | 410 | Sales | | 610 | Interest Revenue | | 611 | Gain on Redemption of Bonds | | | EXPENSES | | 510 | Cost of Merchandise Sold | | 515 | Credit Card Expense | | 516 | Cash Short and Over | | 521 | Sales Salaries Expense | | 522 | Office Salaries Expense | | 531 | Advertising Expense | | 532 | Delivery Expense | | 533 | Repairs Expense | | 534 | Selling Expenses | | 535 | Rent Expense | | 536 | Insurance Expense | | 537 | Office Supplies Expense | | 538 | Store Supplies Expense | | 541 | Bad Debt Expense | | 561 | Depreciation Expense-Store Equipment | | 562 | Depreciation Expense-Office Equipment | | 590 | Miscellaneous Expense | | 710 | Interest Expense | | 711 | Loss on Redemption of Bonds | |

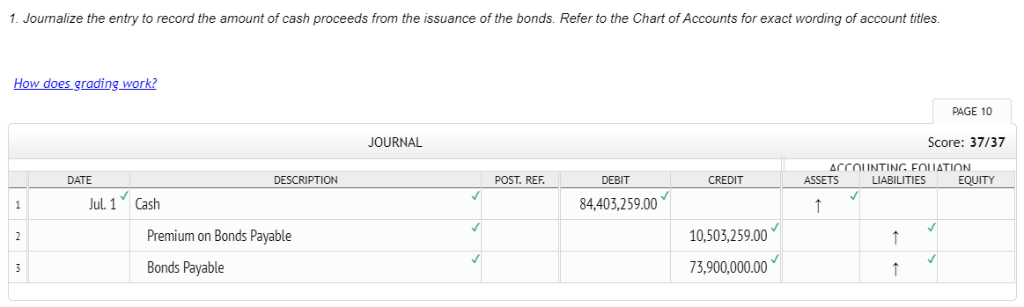

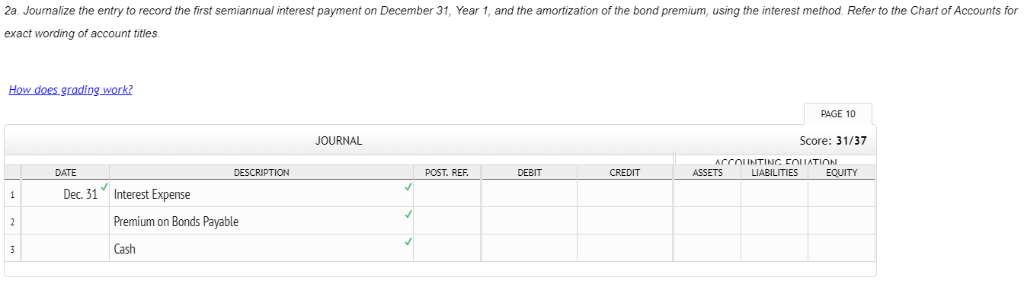

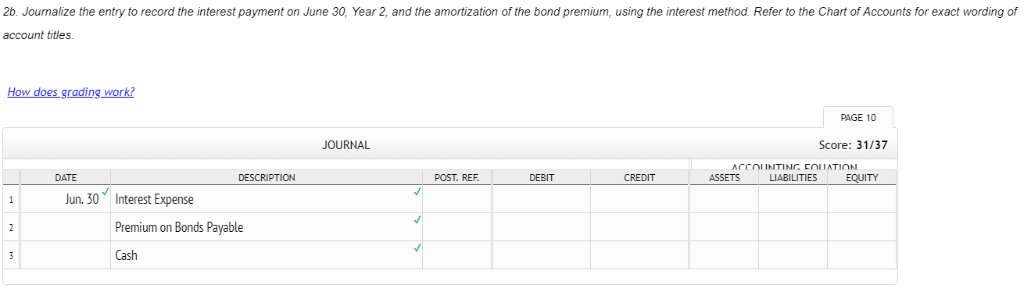

1. Journalize the entry to record the amount of cash proceeds from the issuance of the bonds. Refer to the Chart of Accounts for exact wording of account titles. How does grading work? PAGE 10 JOURNAL Score: 37/37 DATE DESCRIPTION POST. REF DEBIT CREDIT ASSETS LIABILITIES EQUITY Jul. 1Cash 84,403,259.00 Premium on Bonds Payable Bonds Payable 10,503,259.00 73,900,000.00 2a. Jounalize the entry to record the first semiannual interest payment on December 31, Year 1, and the amortization of the bond premium, using the interest method. Refer to the Chart of Accounts for exact wording of account titles How does grading work? PAGE 10 JOURNAL Score: 31/37 DATE POST. REF. DEBIT CREDIT ASSETS LIABILITIES EQUITY Dec.31Intest Expense Premium on Bonds Payable Cash 2b. Jounalize the entry to record the interest payment on June 30, Year 2, and the amortization of the bond premium, using the interest method. Refer to the Chart of Accounts for exact wording of account titles. How does grading work? PAGE 10 JOURNAL Score: 31/37 DATE DESCRIPTION POST. REF DEBIT CREDIT ASSETS LIABILITIES EQUITY Jun. 30 Interest Expense Premium on Bonds Payable Cash 3. Determine the total interest expense for Year 1 . $