Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Can someone do these questions with a Creative Director in California as the career and the retiring age of 65. Assignment: Personal Financial Planning for

Can someone do these questions with a Creative Director in California as the career and the retiring age of 65.

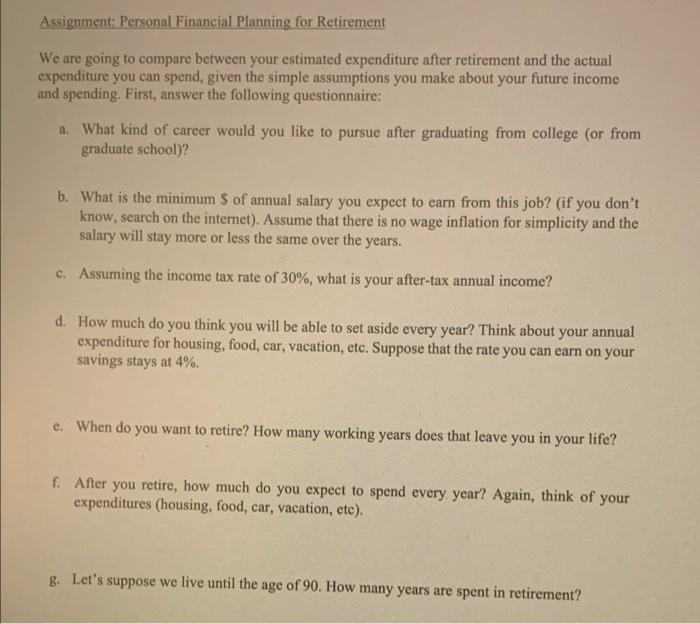

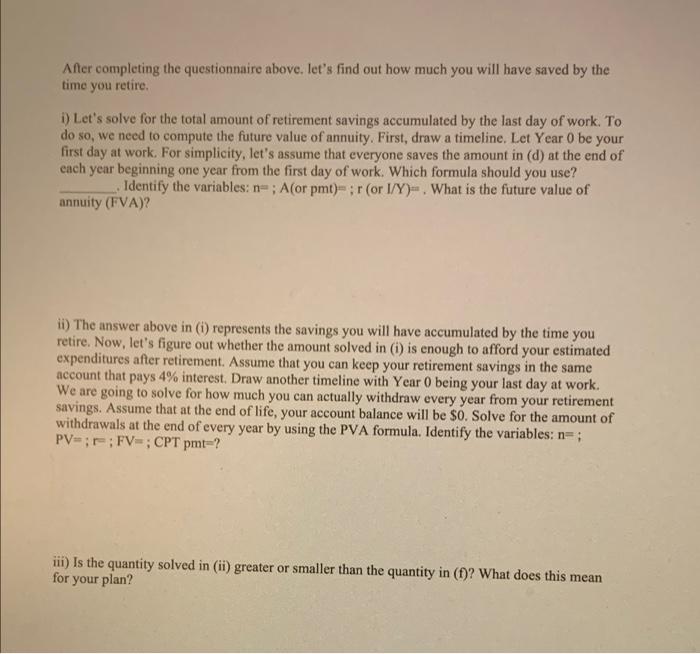

Assignment: Personal Financial Planning for Retirement We are going to compare between your estimated expenditure after retirement and the actual expenditure you can spend, given the simple assumptions you make about your future income and spending. First, answer the following questionnaire: a. What kind of career would you like to pursue after graduating from college (or from graduate school)? b. What is the minimum $ of annual salary you expect to earn from this job? (if you don't know, search on the internet). Assume that there is no wage inflation for simplicity and the salary will stay more or less the same over the years. c. Assuming the income tax rate of 30%, what is your after-tax annual income? d. How much do you think you will be able to set aside every year? Think about your annual expenditure for housing, food, car, vacation, etc. Suppose that the rate you can earn on your savings stays at 4%. e. When do you want to retire? How many working years does that leave you in your life? f. After you retire, how much do you expect to spend every year? Again, think of your expenditures (housing, food, car, vacation, etc). g. Let's suppose we live until the age of 90. How many years are spent in retirement? After completing the questionnaire above. let's find out how much you will have saved by the time you retire. i) Let's solve for the total amount of retirement savings accumulated by the last day of work. To do so, we need to compute the future value of annuity. First, draw a timeline. Let Year 0 be your first day at work. For simplicity, let's assume that everyone saves the amount in (d) at the end of each year beginning one year from the first day of work. Which formula should you use? . Identify the variables: n=; A(or pmt); r (or I/Y). What is the future value of annuity (FVA)? ii) The answer above in (i) represents the savings you will have accumulated by the time you retire. Now, let's figure out whether the amount solved in (i) is enough to afford your estimated expenditures after retirement. Assume that you can keep your retirement savings in the same account that pays 4% interest. Draw another timeline with Year 0 being your last day at work. We are going to solve for how much you can actually withdraw every year from your retirement savings. Assume that at the end of life, your account balance will be $0. Solve for the amount of withdrawals at the end of every year by using the PVA formula. Identify the variables: n=; PV=;; FV; CPT pmt=? iii) Is the quantity solved in (ii) greater or smaller than the quantity in (f)? What does this mean for your plan? Assignment: Personal Financial Planning for Retirement We are going to compare between your estimated expenditure after retirement and the actual expenditure you can spend, given the simple assumptions you make about your future income and spending. First, answer the following questionnaire: a. What kind of career would you like to pursue after graduating from college (or from graduate school)? b. What is the minimum $ of annual salary you expect to earn from this job? (if you don't know, search on the internet). Assume that there is no wage inflation for simplicity and the salary will stay more or less the same over the years. c. Assuming the income tax rate of 30%, what is your after-tax annual income? d. How much do you think you will be able to set aside every year? Think about your annual expenditure for housing, food, car, vacation, etc. Suppose that the rate you can earn on your savings stays at 4%. e. When do you want to retire? How many working years does that leave you in your life? f. After you retire, how much do you expect to spend every year? Again, think of your expenditures (housing, food, car, vacation, etc). g. Let's suppose we live until the age of 90. How many years are spent in retirement? After completing the questionnaire above. let's find out how much you will have saved by the time you retire. i) Let's solve for the total amount of retirement savings accumulated by the last day of work. To do so, we need to compute the future value of annuity. First, draw a timeline. Let Year 0 be your first day at work. For simplicity, let's assume that everyone saves the amount in (d) at the end of each year beginning one year from the first day of work. Which formula should you use? . Identify the variables: n=; A(or pmt); r (or I/Y). What is the future value of annuity (FVA)? ii) The answer above in (i) represents the savings you will have accumulated by the time you retire. Now, let's figure out whether the amount solved in (i) is enough to afford your estimated expenditures after retirement. Assume that you can keep your retirement savings in the same account that pays 4% interest. Draw another timeline with Year 0 being your last day at work. We are going to solve for how much you can actually withdraw every year from your retirement savings. Assume that at the end of life, your account balance will be $0. Solve for the amount of withdrawals at the end of every year by using the PVA formula. Identify the variables: n=; PV=;; FV; CPT pmt=? iii) Is the quantity solved in (ii) greater or smaller than the quantity in (f)? What does this mean for your plan Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Governance Of Financial Management

Authors: John Carver, Miriam Carver

1st Edition

0470392541, 9780470392546