Answered step by step

Verified Expert Solution

Question

1 Approved Answer

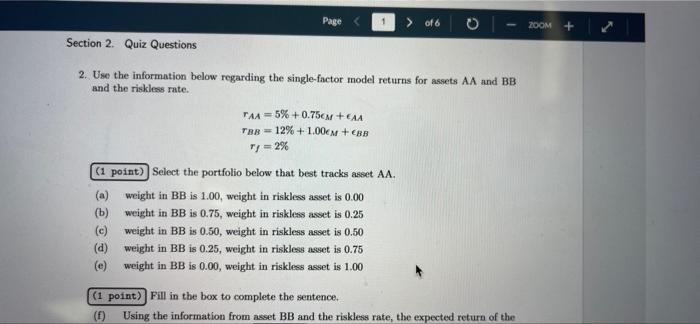

Can someone explain why selection (b.) best tracks assett AA? Page > of 6 Section 2. Quiz Questions 2. Use the information below regarding the

Can someone explain why selection (b.) best tracks assett AA?

Page > of 6 Section 2. Quiz Questions 2. Use the information below regarding the single-factor model returns for assets AA and BB and the riskless rate. TAA5%+0.75CM +EAA TBB 12% +1.00CM + EBB 71=2% (1 point)] Select the portfolio below that best tracks asset AA. (a) weight in BB is 1.00, weight in riskless asset is 0.00 weight in BB is 0.75, weight in riskless asset is 0.25 (b) (c) weight in BB is 0.50, weight in riskless asset is 0.50 (d) weight in BB is 0.25, weight in riskless asset is 0.75 (e) weight in BB is 0.00, weight in riskless asset is 1.00 (1 point) Fill in the box to complete the sentence. (f) Using the information from asset BB and the riskless rate, the expected return of the ZOOM + Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Social Profit Handbook

Authors: David Grant

1st Edition

1603586040, 978-1603586047