Answered step by step

Verified Expert Solution

Question

1 Approved Answer

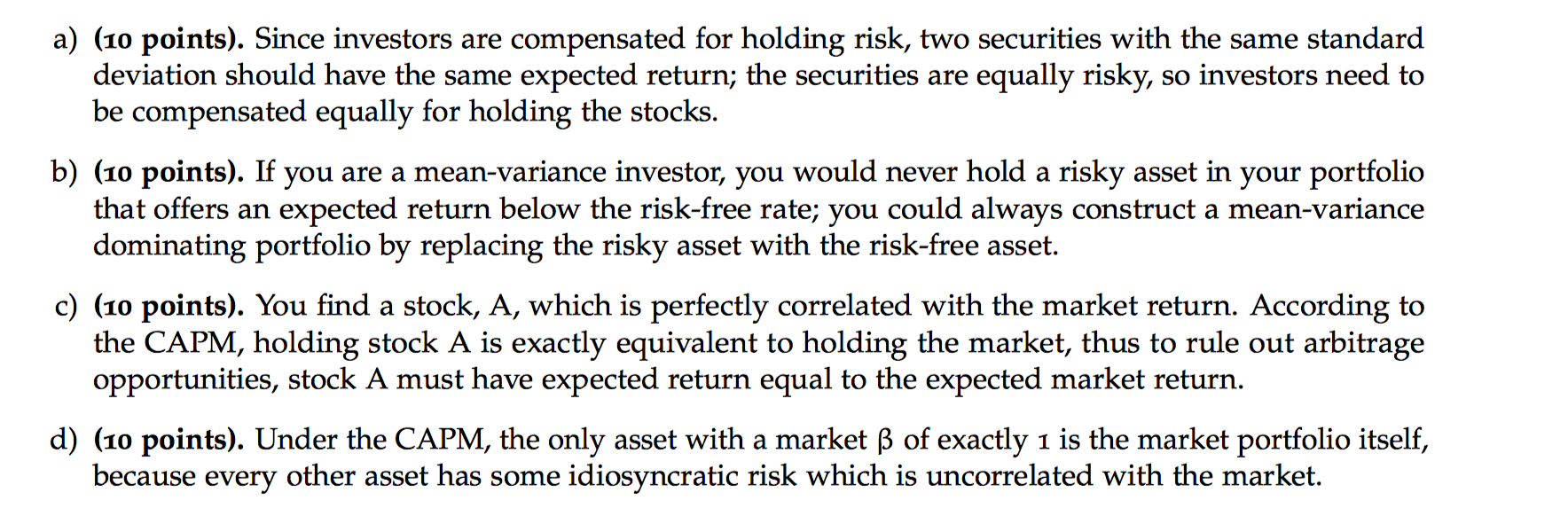

Can someone help me with these True/False questions? Please provide justifications so I can learn. a) (10 points). Since investors are compensated for holding risk,

Can someone help me with these True/False questions? Please provide justifications so I can learn.

Can someone help me with these True/False questions? Please provide justifications so I can learn.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Getting The Schools You Want A Step By Step Guide To Conducting Your Own Curriculum Management Audit

Authors: Kimberly M. Logan

1st Edition

0803965443, 978-0803965447