Answered step by step

Verified Expert Solution

Question

1 Approved Answer

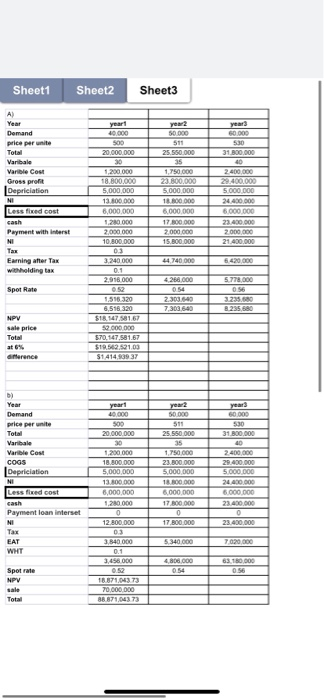

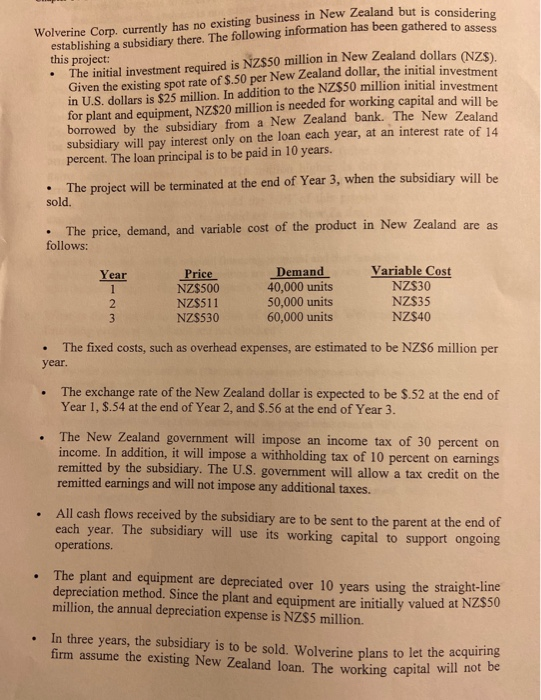

can you check mu answer and Do E ? for me pleasr the fisrt sheet is rhe answe Sheet1 Sheet2 Sheet3 A) year 60.000 Year

can you check mu answer and Do E ? for me pleasr

the fisrt sheet is rhe answe

Sheet1 Sheet2 Sheet3 A) year 60.000 Year year year2 50000 Demand 40000 price per unite 500 20.000.000 511 530 25.550.000 31800,000 Total 30 1200.000 18.800,000 35 40 Varibale 2400,000 29.400.000 Varible Cost Gross profit Depriciation 1,750,000 23.800,000 5.000.000 5,000,000 18800000 6,000.000 5,000,000 24.400 000 13.800000 NI Less fixed cost 6,000,000 6000,000 cash 1280 000 17.800.000 23400000 2.000,000 2000.000 Payment with interst 2,000,00 15.800.000 10.800.000 21.400.000 NI 03 Earning after Tax 3,240.000 44 740000 6420,000 wiholding tax 0.1 4266.000 2916.000 5778,000 Spot Rate 052 054 056 3.235.680 1516 320 2.303.640 7,303.640 8235.680 6,516 320 $18,147 581.67 52.000.000 NPV sale price $70.147.581.67 $19.562 521.03 Total at 6% $1414.839 37 anerence b) Year year2 year 60,000 yeart Demand 40,000 50.000 price per unite 500 20.000.000 511 530 25.550.000 31.800.000 Total Varbale 30 1200 000 35 1.750 000 40 2400,000 29.400.000 Varible Cost 23.800 000 COGS 18.800.000 Depriciation 5,000,000 5,000,000 18800,000 6,000.000 5.000,000 24400 000 NI 13.800 000 Less fixed cost 6,000,000 6,000,000 17.800 000 cash ,280.000 23400.000 Payment loan interset 0 12.800.000 0 17.800.000 0 23,400,000 NI 03 7.020,000 EAT 3840.000 5,340,000 WHT 0.1 4.806.000 63.180 000 3456 000 056 Spot rate 0.52 054 NPV 18871,043 73 sale 70,000,000- 88.871,043 73 Total Wolverine Corp. currently has no existing business in New Zealand but is considering establishing a subsidiary there. The following information has been gathered to assess this project: The initial investment required is NZ$50 million in New Zealand dollars (NZS). Given the existing spot rate of $.50 per New Zealand dollar, the initial investment in U.S. dollars is $25 million. In addition to the NZS50 million initial investment for plant and equipment, NZ$20 million is needed for working capital and will he borrowed by the subsidiary from a New Zealand bank. The New Zealand subsidiary will pay interest only on the loan each year, at an interest rate of 14 percent. The loan principal is to be paid in 10 years. The project will be terminated at the end of Year 3, when the subsidiary will be sold. The price, demand, and variable cost of the product in New Zealand are as follows: Demand 40,000 units 50,000 units 60,000 units Variable Cost Price NZ$500 NZ$511 NZ$530 Year NZ$30 NZ$35 2 NZ$40 3 The fixed costs, such as overhead expenses, are estimated to be NZ$6 million per year. The exchange rate of the New Zealand dollar is expected to be $.52 at the end of Year 1, $.54 at the end of Year 2, and $.56 at the end of Year 3. The New Zealand government will impose an income tax of 30 percent on income. In addition, it will impose a withholding tax of 10 percent on earnings remitted by the subsidiary. The U.S. government will allow a tax credit on the remitted earnings and will not impose any additional taxes. All cash flows received by the subsidiary are to be sent to the parent at the end of each year. The subsidiary will use its working capital to support ongoing operations. The plant and equipment are depreciated over 10 years using the straight-line depreciation method. Since the plant and equipment are initially valued at NZS50 million, the annual depreciation expense is NZ$5 million. In three years, the subsidiary is to be sold. Wolverine plans to let the acquiring firm assume the existing New Zealand loan. The working capital will not be liquidated but will be used by the acquiring firm when it sells the subsidiary. Wolverine expects to receive NZ$52 million after subtracting capital gains taxes. Assume that this amount is not subject to a withholding tax. Wolverine requires a of return 20 percent rate this project. on a. Determine the net present value of this project. Should Wolverine accept this project? b. Assume that Wolverine is also considering an alternative financing arrangement in which the parent would invest an additional USS10 million (20 million NZD) to cover the working capital requirements so that the subsidiary would avoid the New Zealand loan (the upfront investment is now 50 million NZD plus 20 million NZD for the Net Working Capital resulting in a total investment of 70 million NZD)., If this arrangement is used, the selling price of the subsidiary (after subtracting any capital gains taxes) is expected to be NZ$18 million higher. Is this alternative financing arrangement more feasible for the parent than the original proposal? Explain. c. From the parent's perspective, would the NPV of this project be more sensitive to exchange rate movements if the subsidiary uses New Zealand financing to cover the working capital or if the parent invests more of its own funds to cover the working capital? Explain. d. Assume Wolverine used the original financing proposal and that funds are blocked until the subsidiary is sold. The funds to be remitted are reinvested at a rate of 6 percent (after taxes) until the end of Year 3. How is the project's NPV affected? What is the break-even salvage value of this project if Wolverine uses the original financing proposal and funds are not blocked? e. 2) By what percent can Unit Sales (Demand) decrease and the project breakeven on NPV (use the original proposal)? 3) By what percent can Fixed Costs increase and the project breakeven on NPV (use the original proposal)? 4) Assume a bad case scenario has happened (prices will be 5% less than forecasted, demand will be 10% less than forecasted, and fixed costs will be 10 % more than forecasted). What is the NPV under this scenario? Sheet1 Sheet2 Sheet3 A) year 60.000 Year year year2 50000 Demand 40000 price per unite 500 20.000.000 511 530 25.550.000 31800,000 Total 30 1200.000 18.800,000 35 40 Varibale 2400,000 29.400.000 Varible Cost Gross profit Depriciation 1,750,000 23.800,000 5.000.000 5,000,000 18800000 6,000.000 5,000,000 24.400 000 13.800000 NI Less fixed cost 6,000,000 6000,000 cash 1280 000 17.800.000 23400000 2.000,000 2000.000 Payment with interst 2,000,00 15.800.000 10.800.000 21.400.000 NI 03 Earning after Tax 3,240.000 44 740000 6420,000 wiholding tax 0.1 4266.000 2916.000 5778,000 Spot Rate 052 054 056 3.235.680 1516 320 2.303.640 7,303.640 8235.680 6,516 320 $18,147 581.67 52.000.000 NPV sale price $70.147.581.67 $19.562 521.03 Total at 6% $1414.839 37 anerence b) Year year2 year 60,000 yeart Demand 40,000 50.000 price per unite 500 20.000.000 511 530 25.550.000 31.800.000 Total Varbale 30 1200 000 35 1.750 000 40 2400,000 29.400.000 Varible Cost 23.800 000 COGS 18.800.000 Depriciation 5,000,000 5,000,000 18800,000 6,000.000 5.000,000 24400 000 NI 13.800 000 Less fixed cost 6,000,000 6,000,000 17.800 000 cash ,280.000 23400.000 Payment loan interset 0 12.800.000 0 17.800.000 0 23,400,000 NI 03 7.020,000 EAT 3840.000 5,340,000 WHT 0.1 4.806.000 63.180 000 3456 000 056 Spot rate 0.52 054 NPV 18871,043 73 sale 70,000,000- 88.871,043 73 Total Wolverine Corp. currently has no existing business in New Zealand but is considering establishing a subsidiary there. The following information has been gathered to assess this project: The initial investment required is NZ$50 million in New Zealand dollars (NZS). Given the existing spot rate of $.50 per New Zealand dollar, the initial investment in U.S. dollars is $25 million. In addition to the NZS50 million initial investment for plant and equipment, NZ$20 million is needed for working capital and will he borrowed by the subsidiary from a New Zealand bank. The New Zealand subsidiary will pay interest only on the loan each year, at an interest rate of 14 percent. The loan principal is to be paid in 10 years. The project will be terminated at the end of Year 3, when the subsidiary will be sold. The price, demand, and variable cost of the product in New Zealand are as follows: Demand 40,000 units 50,000 units 60,000 units Variable Cost Price NZ$500 NZ$511 NZ$530 Year NZ$30 NZ$35 2 NZ$40 3 The fixed costs, such as overhead expenses, are estimated to be NZ$6 million per year. The exchange rate of the New Zealand dollar is expected to be $.52 at the end of Year 1, $.54 at the end of Year 2, and $.56 at the end of Year 3. The New Zealand government will impose an income tax of 30 percent on income. In addition, it will impose a withholding tax of 10 percent on earnings remitted by the subsidiary. The U.S. government will allow a tax credit on the remitted earnings and will not impose any additional taxes. All cash flows received by the subsidiary are to be sent to the parent at the end of each year. The subsidiary will use its working capital to support ongoing operations. The plant and equipment are depreciated over 10 years using the straight-line depreciation method. Since the plant and equipment are initially valued at NZS50 million, the annual depreciation expense is NZ$5 million. In three years, the subsidiary is to be sold. Wolverine plans to let the acquiring firm assume the existing New Zealand loan. The working capital will not be liquidated but will be used by the acquiring firm when it sells the subsidiary. Wolverine expects to receive NZ$52 million after subtracting capital gains taxes. Assume that this amount is not subject to a withholding tax. Wolverine requires a of return 20 percent rate this project. on a. Determine the net present value of this project. Should Wolverine accept this project? b. Assume that Wolverine is also considering an alternative financing arrangement in which the parent would invest an additional USS10 million (20 million NZD) to cover the working capital requirements so that the subsidiary would avoid the New Zealand loan (the upfront investment is now 50 million NZD plus 20 million NZD for the Net Working Capital resulting in a total investment of 70 million NZD)., If this arrangement is used, the selling price of the subsidiary (after subtracting any capital gains taxes) is expected to be NZ$18 million higher. Is this alternative financing arrangement more feasible for the parent than the original proposal? Explain. c. From the parent's perspective, would the NPV of this project be more sensitive to exchange rate movements if the subsidiary uses New Zealand financing to cover the working capital or if the parent invests more of its own funds to cover the working capital? Explain. d. Assume Wolverine used the original financing proposal and that funds are blocked until the subsidiary is sold. The funds to be remitted are reinvested at a rate of 6 percent (after taxes) until the end of Year 3. How is the project's NPV affected? What is the break-even salvage value of this project if Wolverine uses the original financing proposal and funds are not blocked? e. 2) By what percent can Unit Sales (Demand) decrease and the project breakeven on NPV (use the original proposal)? 3) By what percent can Fixed Costs increase and the project breakeven on NPV (use the original proposal)? 4) Assume a bad case scenario has happened (prices will be 5% less than forecasted, demand will be 10% less than forecasted, and fixed costs will be 10 % more than forecasted). What is the NPV under this scenario Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Gapenskis Understanding Healthcare Financial Management

Authors: George H. Pink, Paula H. Song

8th Edition

1640551093, 978-1640551091