Answered step by step

Verified Expert Solution

Question

1 Approved Answer

can you help ? be specific so I can learn when doing similar problems. Calculate 98% and 99% VaR at the 1 and 10 day

can you help ? be specific so I can learn when doing similar problems.

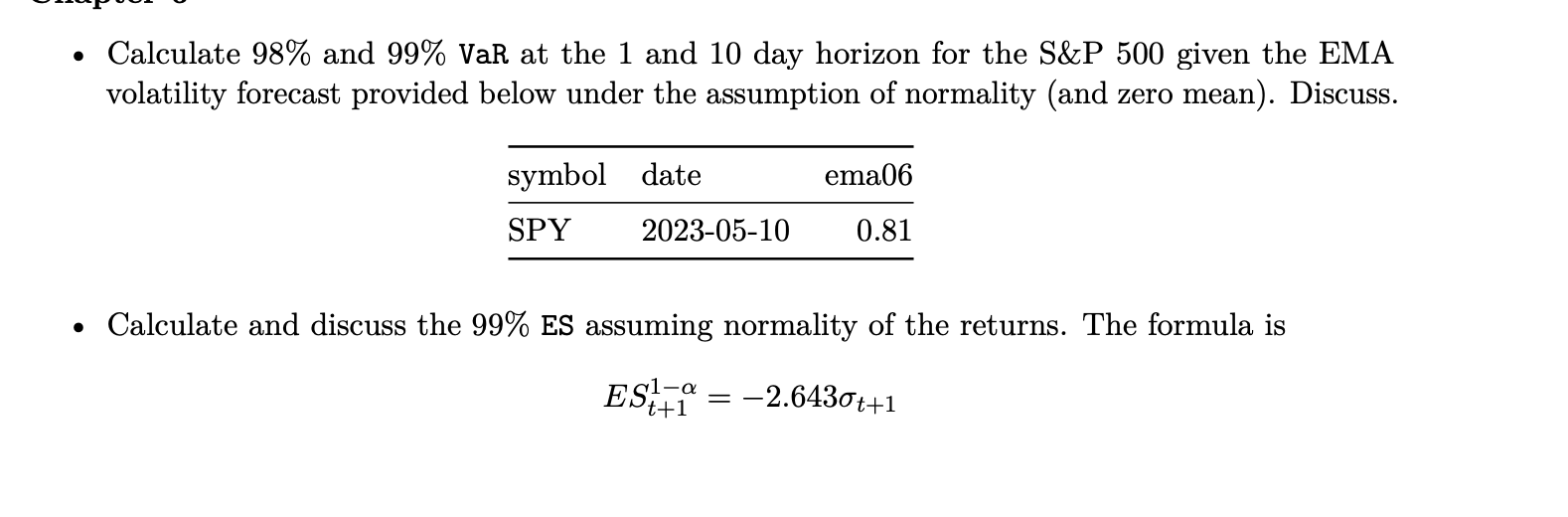

Calculate 98% and 99% VaR at the 1 and 10 day horizon for the S\&P 500 given the EMA volatility forecast provided below under the assumption of normality (and zero mean). Discuss. Calculate and discuss the 99% ES assuming normality of the returns. The formula is ESt+11=2.643t+1

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Markets and Institutions

Authors: Anthony Saunders, Marcia Cornett

6th edition