Answered step by step

Verified Expert Solution

Question

1 Approved Answer

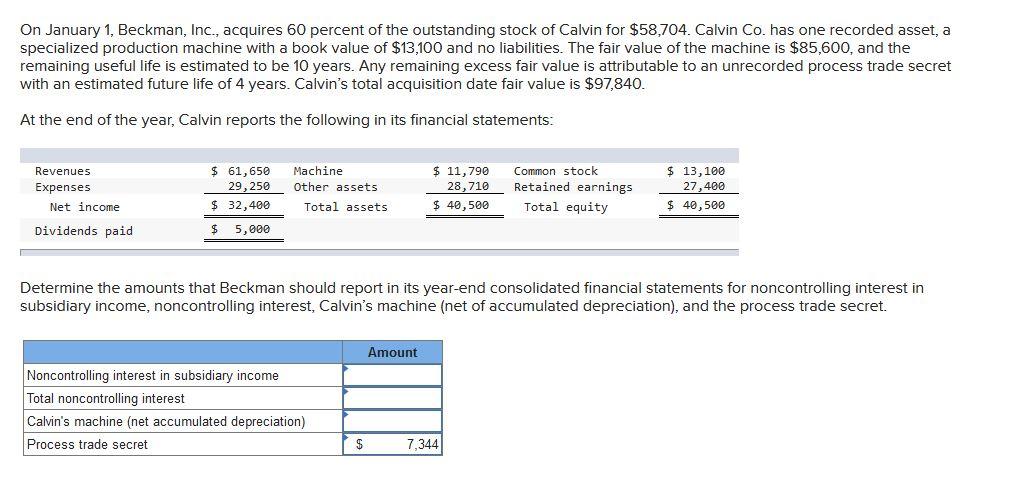

Can you help with this? On January 1, Beckman, Inc., acquires 60 percent of the outstanding stock of Calvin for $58,704. Calvin Co. has one

Can you help with this?

Can you help with this?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting Tools for business decision making

Authors: Paul D. Kimmel, Jerry J. Weygandt, Donald E. Kieso

6th Edition

978-1119191674, 047053477X, 111919167X, 978-0470534779