Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Can you please explain as much as you can. Thank you! Textbook: Financial Mathematics A comprehensive Treatment by Giuseppe Campolieti page 200, Exercise 5.3 21

Can you please explain as much as you can. Thank you!

Textbook: Financial Mathematics A comprehensive Treatment by Giuseppe Campolieti

page 200, Exercise 5.3

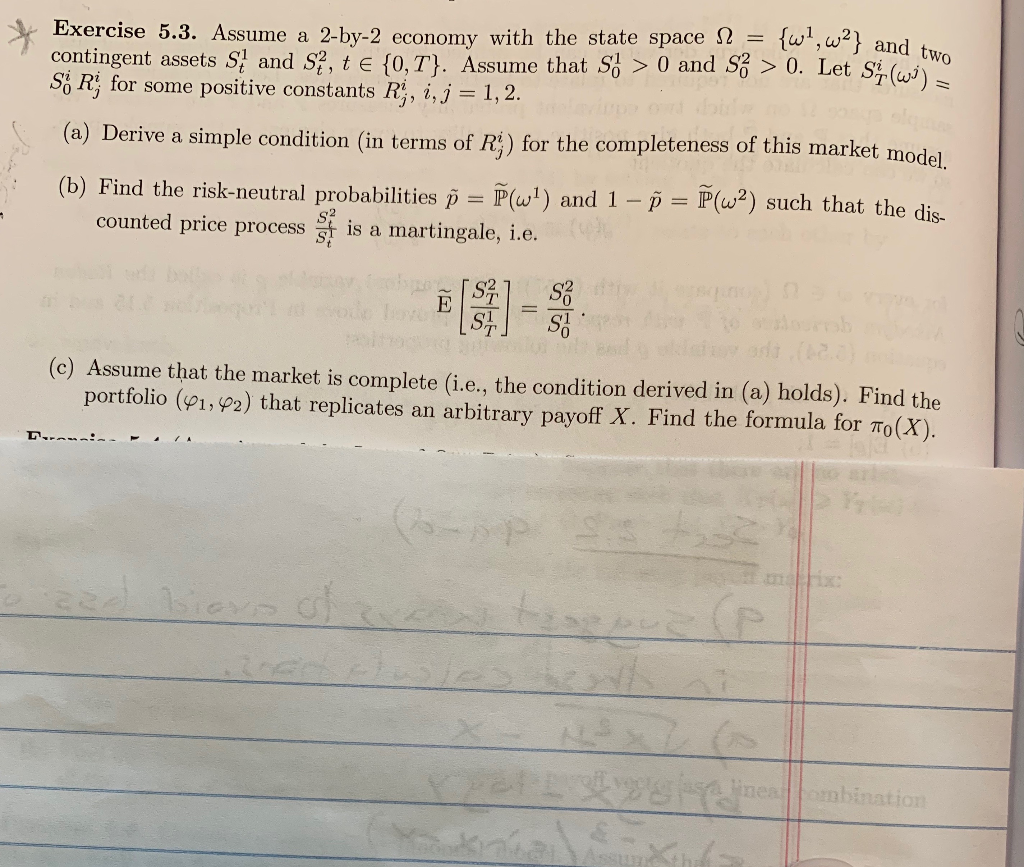

21 and two Exercise 5.3. Assume a 2-by-2 economy with the state space 12 = {w',w2} and + contingent assets S1 and S, te {0,T). Assume that so > 0 and S > 0. Let S (W) - S; R for some positive constants R, i, j = 1,2. (a) Derive a simple condition (in terms of R) for the completeness of this market model ; (b) Find the risk-neutral probabilities = (wl) and 1 - = P(wa) such that the dis- counted price process is a martingale, i.e. (c) Assume that the market is complete (i.e., the condition derived in (a) holds). Find the portfolio (41,42) that replicates an arbitrary payoff X. Find the formula for to(X). ambination 21 and two Exercise 5.3. Assume a 2-by-2 economy with the state space 12 = {w',w2} and + contingent assets S1 and S, te {0,T). Assume that so > 0 and S > 0. Let S (W) - S; R for some positive constants R, i, j = 1,2. (a) Derive a simple condition (in terms of R) for the completeness of this market model ; (b) Find the risk-neutral probabilities = (wl) and 1 - = P(wa) such that the dis- counted price process is a martingale, i.e. (c) Assume that the market is complete (i.e., the condition derived in (a) holds). Find the portfolio (41,42) that replicates an arbitrary payoff X. Find the formula for to(X). ambinationStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Build An Online Retail System For Under $150

Authors: Roger Butterworth

1st Edition

1530170044, 978-1530170043