Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Can you please show calculations. A major requirement in managing a fixed-income portfolio using a contingent immunization policy is monitoring the relationship between the current

Can you please show calculations.

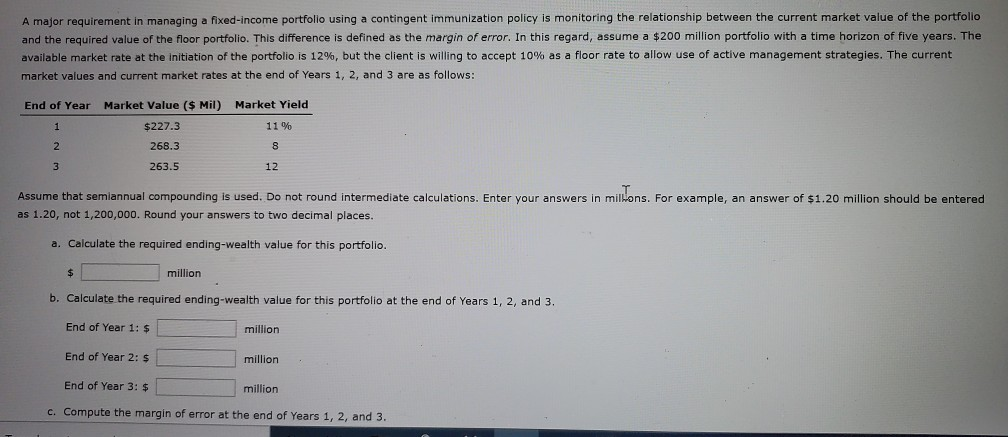

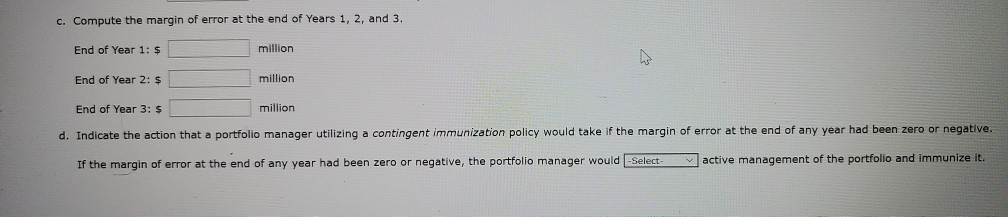

A major requirement in managing a fixed-income portfolio using a contingent immunization policy is monitoring the relationship between the current market value of the portfolio and the required value of the floor portfolio. This difference is defined as the margin of error. In this regard, assume a $200 million portfolio with a time horizon of five years. The available market rate at the initiation of the portfolio is 12%, but the client is willing to accept 10% as a floor rate to allow use of active management strategies. The current market values and current market rates at the end of Years 1, 2, and 3 are as follows: End of Year Market Value ($ Mil) Market Yield $227.3 11 % 268.3 263.5 12 Assume that semiannual compounding is used. Do not round Intermediate calculations. Enter your answers in millons. For example, an answer of $1.20 million should be entered as 1.20, not 1,200,000. Round your answers to two decimal places. a. Calculate the required ending-wealth value for this portfolio. $ million b. Calculate the required ending-wealth value for this portfolio at the end of Years 1, 2, and 3. End of Year 1: $ million End of Year 2: $ million End of Year 3: $ million c. Compute the margin of error at the end of Years 1, 2, and 3. c. Compute the margin of error at the end of Years 1, 2, and 3. End of Year 1: $ million End of Year 2: $ million End of Year 3: $ million d. Indicate the action that a portfolio manager utilizing a contingent immunization policy would take if the margin of error at the end of any year had been zero or negative. If the margin of error at the end of any year had been zero or negative, the portfolio manager would -Select active management of the portfolio and immunize itStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Banking With Integrity The Winners Of The Financial Crisis

Authors: Dr Heiko Spitzeck , Dr Michael Pirson, Dierksme , Dr. Heiko Spitzeck , Prof. Claus Dierksmeier, Dr. Michael Pirson

1st Edition

0230289959,0230346499