Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Can you please show me how to get all of these answers? And can you please answer all parts! Thank you! 2. A call option

Can you please show me how to get all of these answers? And can you please answer all parts! Thank you!

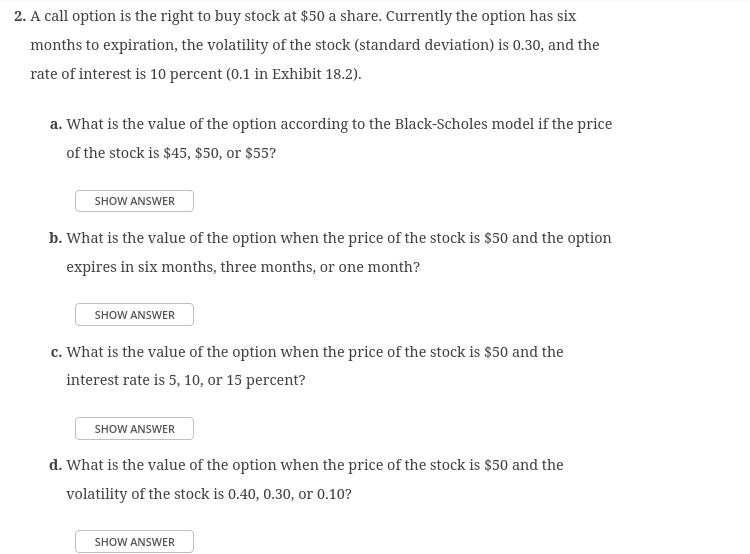

2. A call option is the right to buy stock at $50 a share. Currently the option has six months to expiration, the volatility of the stock (standard deviation) is 0.30 , and the rate of interest is 10 percent (0.1 in Exhibit 18.2). a. What is the value of the option according to the Black-Scholes model if the price of the stock is $45,$50, or $55 ? b. What is the value of the option when the price of the stock is $50 and the option expires in six months, three months, or one month? c. What is the value of the option when the price of the stock is $50 and the interest rate is 5,10 , or 15 percent? d. What is the value of the option when the price of the stock is $50 and the volatility of the stock is 0.40,0.30, or 0.10 ? 2. A call option is the right to buy stock at $50 a share. Currently the option has six months to expiration, the volatility of the stock (standard deviation) is 0.30 , and the rate of interest is 10 percent (0.1 in Exhibit 18.2). a. What is the value of the option according to the Black-Scholes model if the price of the stock is $45,$50, or $55 ? b. What is the value of the option when the price of the stock is $50 and the option expires in six months, three months, or one month? c. What is the value of the option when the price of the stock is $50 and the interest rate is 5,10 , or 15 percent? d. What is the value of the option when the price of the stock is $50 and the volatility of the stock is 0.40,0.30, or 0.10Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Quantitative Analysis for Management

Authors: Barry Render, Ralph M. Stair, Michael E. Hanna, Trevor S. Ha

12th edition

133507335, 978-0133507331