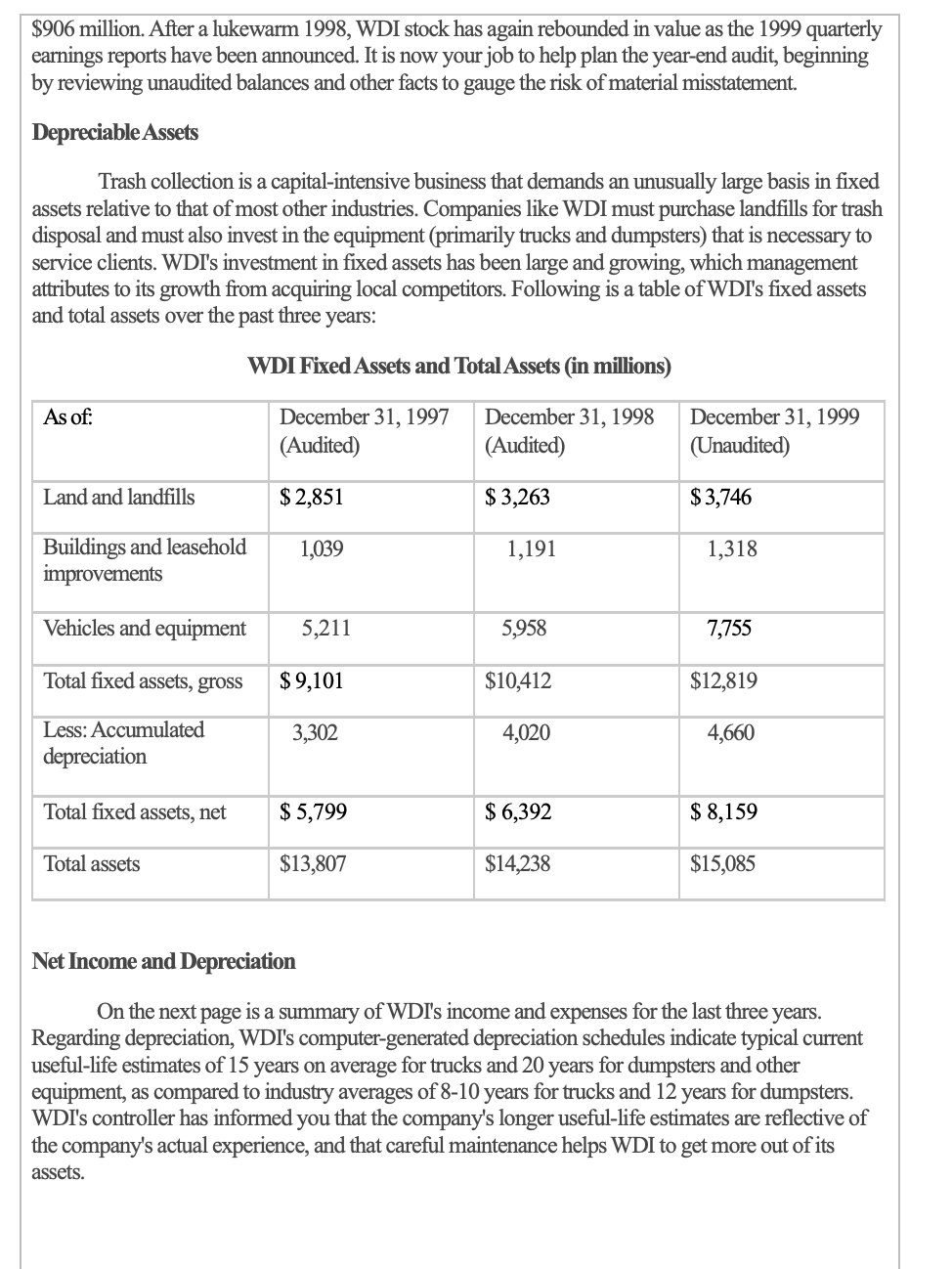

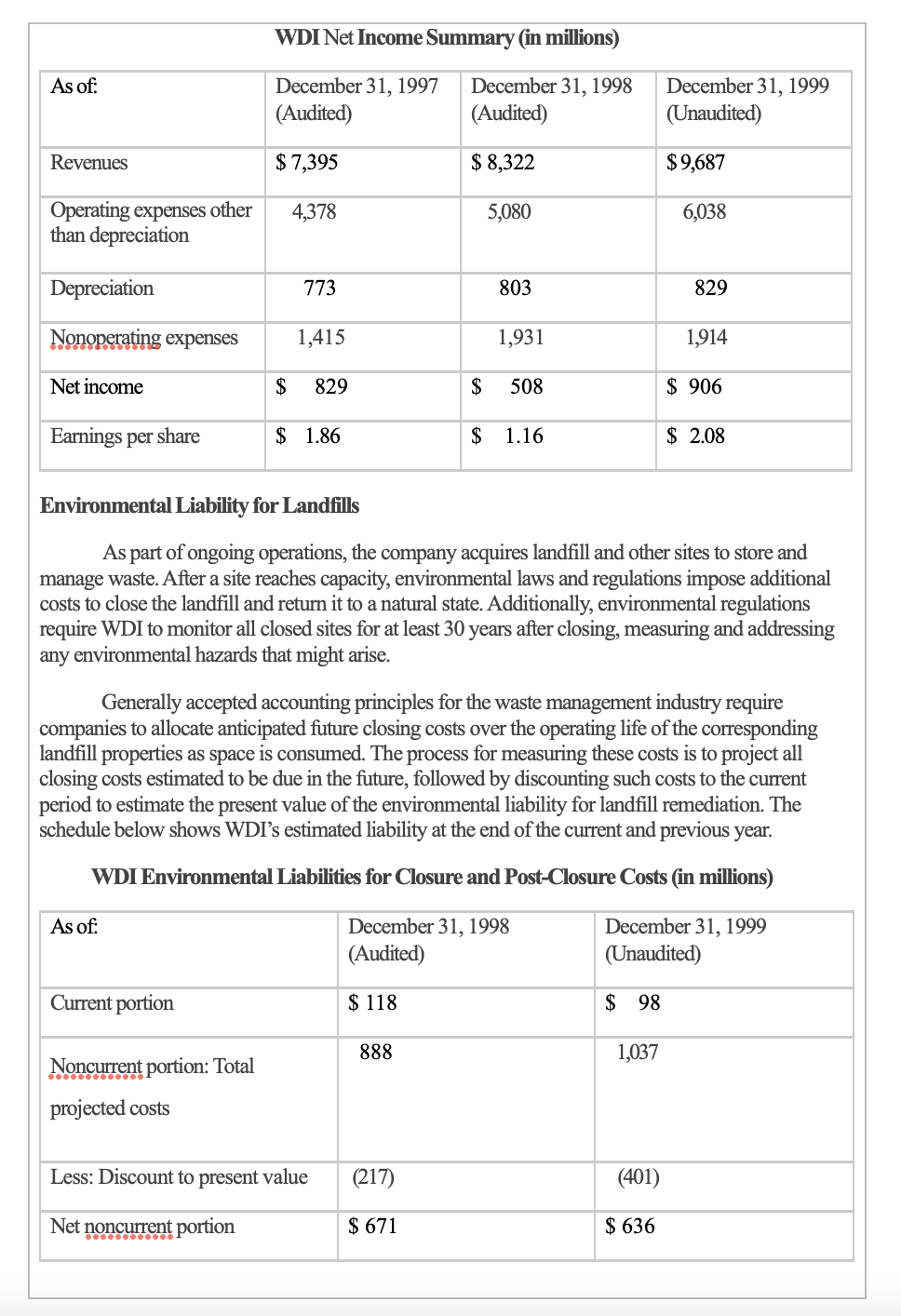

CASE 3: Waste Disposal, Inc. Point value: This case is worth a maximum of 30 points. Maximum solution length: Three double-spaced pages Source This case is adapted from a 2003 American Accounting Association case written by Srinivasan Ragothaman, William Wilcox and Thomas Davies, which in turn is based on the real-life late-1990s accounting scandal involving Waste Management, Inc. and its auditor, Arthur Andersen LLP. The case material is copyrighted by the American Accounting Association, but with permission to reproduce for educational purposes. In addition, certain liberties have been taken with the case and with its requirements for application in this course. Overview Your 1999 audit client is Waste Disposal, Inc. (WDI), a publicly traded company that is a major player in the domestic and international trash collection industry. Much of the company's expansion has come from an aggressive pattern of acquiring over 200 local trash hauling companies, to the point that by the current year (1999), WDI accounted for 20 percent market share of the total U.S. trash collection business. In the late 1990s, WDI's basic business strategy was to acquire smaller "mom and pop" trash collection operations and consolidate them into one giant enterprise. WDI also diversified into related industries such as recycling, water treatment, energy supply and trading, and lawn care. WDI's aggressive growth strategy resulted in ten years of double-digit growth in total assets, accompanied by similar growth in profits and a meteoric increase in the company's stock price. However, last year (1998) was the first year in which net income did not grow, instead falling from $829 million in 1997 to $508 million in 1998 due largely to smaller returns from WDI's most recent acquisitions and from the increased pressure of environmental regulations affecting trash collection, landfills, and toxic wastes. Lower profits also reflected a more competitive environment in the trash collection business, despite WDI's aggressive takeover strategy. Fortunately for WDI, as explained to you by the company's CFO, an effective cost-cutting program has rejuvenated the (unaudited) 1999 profit figures to an all-time high of \$906 million. After a lukewarm 1998, WDI stock has again rebounded in value as the 1999 quarterly earnings reports have been announced. It is now your job to help plan the year-end audit, beginning by reviewing unaudited balances and other facts to gauge the risk of material misstatement. DepreciableAssets Trash collection is a capital-intensive business that demands an unusually large basis in fixed assets relative to that of most other industries. Companies like WDI must purchase landfills for trash disposal and must also invest in the equipment (primarily trucks and dumpsters) that is necessary to service clients. WDI's investment in fixed assets has been large and growing, which management attributes to its growth from acquiring local competitors. Following is a table of WDI's fixed assets and total assets over the past three years: WDI Fixed Assets and Total Assets (in millions) Net Income and Depreciation On the next page is a summary of WDI's income and expenses for the last three years. Regarding depreciation, WDI's computer-generated depreciation schedules indicate typical current useful-life estimates of 15 years on average for trucks and 20 years for dumpsters and other equipment, as compared to industry averages of 8-10 years for trucks and 12 years for dumpsters. WDI's controller has informed you that the company's longer useful-life estimates are reflective of the company's actual experience, and that careful maintenance helps WDI to get more out of its assets. Environmental Liability for Landfills As part of ongoing operations, the company acquires landfill and other sites to store and manage waste. After a site reaches capacity, environmental laws and regulations impose additional costs to close the landfill and return it to a natural state. Additionally, environmental regulations require WDI to monitor all closed sites for at least 30 years after closing, measuring and addressing any environmental hazards that might arise. Generally accepted accounting principles for the waste management industry require companies to allocate anticipated future closing costs over the operating life of the corresponding landfill properties as space is consumed. The process for measuring these costs is to project all closing costs estimated to be due in the future, followed by discounting such costs to the current period to estimate the present value of the environmental liability for landfill remediation. The schedule below shows WDI's estimated liability at the end of the current and previous year. WDI Environmental Liabilities for Closure and Post-Closure Costs (in millions) Reclassified gain During 1999, WDI realized a $110 million gain from selling an interest in a business called SM, Inc. In its 1999 unaudited financial statements, the company offset this gain against unrelated operating expenses and adjustments of prior-year estimates. The controller justifies this treatment as an efficient way to avoid cluttering the income statement with a separate line item for the gain on the sale of SM, Inc., given that management does not consider the amount involved to be material to the financial statements taken as a whole, and that the proposed treatment is simply a reclassification, not an increase or decrease in net income. Other observations: - WDI's management owns significant stock in the company from executive stock option awards over the years, and has unexercised options that would become lucrative to exercise only if the WDI stock price increases further. - Both the controller and the chief financial officer of WDI are former members of your audit firm. Your firm has had an excellent working relationship with both of them over the years, and they have hired other auditors from your firm for accounting positions with WDI. - In 1999, WDI secured a new multi-million dollar long-term line of credit to continue its aggressive growth strategy and leverage its operating position. Required: Imagine it is January 2000. In a three-page double-spaced memorandum addressed to "Mark Bradshaw, Partner" (with font and margin restrictions as set forth in the syllabus), summarize the risks you perceive as you contemplate auditing WDI's calendar 1999 financial statements. Be sure to discuss as many risks as you see, i.e., do not simply choose one and devote the entire paper to that risk. Organize your report professionally, as if you were an audit senior assigned to present a planning summary to me, the lead engagement partner for WDI. CASE 3: Waste Disposal, Inc. Point value: This case is worth a maximum of 30 points. Maximum solution length: Three double-spaced pages Source This case is adapted from a 2003 American Accounting Association case written by Srinivasan Ragothaman, William Wilcox and Thomas Davies, which in turn is based on the real-life late-1990s accounting scandal involving Waste Management, Inc. and its auditor, Arthur Andersen LLP. The case material is copyrighted by the American Accounting Association, but with permission to reproduce for educational purposes. In addition, certain liberties have been taken with the case and with its requirements for application in this course. Overview Your 1999 audit client is Waste Disposal, Inc. (WDI), a publicly traded company that is a major player in the domestic and international trash collection industry. Much of the company's expansion has come from an aggressive pattern of acquiring over 200 local trash hauling companies, to the point that by the current year (1999), WDI accounted for 20 percent market share of the total U.S. trash collection business. In the late 1990s, WDI's basic business strategy was to acquire smaller "mom and pop" trash collection operations and consolidate them into one giant enterprise. WDI also diversified into related industries such as recycling, water treatment, energy supply and trading, and lawn care. WDI's aggressive growth strategy resulted in ten years of double-digit growth in total assets, accompanied by similar growth in profits and a meteoric increase in the company's stock price. However, last year (1998) was the first year in which net income did not grow, instead falling from $829 million in 1997 to $508 million in 1998 due largely to smaller returns from WDI's most recent acquisitions and from the increased pressure of environmental regulations affecting trash collection, landfills, and toxic wastes. Lower profits also reflected a more competitive environment in the trash collection business, despite WDI's aggressive takeover strategy. Fortunately for WDI, as explained to you by the company's CFO, an effective cost-cutting program has rejuvenated the (unaudited) 1999 profit figures to an all-time high of \$906 million. After a lukewarm 1998, WDI stock has again rebounded in value as the 1999 quarterly earnings reports have been announced. It is now your job to help plan the year-end audit, beginning by reviewing unaudited balances and other facts to gauge the risk of material misstatement. DepreciableAssets Trash collection is a capital-intensive business that demands an unusually large basis in fixed assets relative to that of most other industries. Companies like WDI must purchase landfills for trash disposal and must also invest in the equipment (primarily trucks and dumpsters) that is necessary to service clients. WDI's investment in fixed assets has been large and growing, which management attributes to its growth from acquiring local competitors. Following is a table of WDI's fixed assets and total assets over the past three years: WDI Fixed Assets and Total Assets (in millions) Net Income and Depreciation On the next page is a summary of WDI's income and expenses for the last three years. Regarding depreciation, WDI's computer-generated depreciation schedules indicate typical current useful-life estimates of 15 years on average for trucks and 20 years for dumpsters and other equipment, as compared to industry averages of 8-10 years for trucks and 12 years for dumpsters. WDI's controller has informed you that the company's longer useful-life estimates are reflective of the company's actual experience, and that careful maintenance helps WDI to get more out of its assets. Environmental Liability for Landfills As part of ongoing operations, the company acquires landfill and other sites to store and manage waste. After a site reaches capacity, environmental laws and regulations impose additional costs to close the landfill and return it to a natural state. Additionally, environmental regulations require WDI to monitor all closed sites for at least 30 years after closing, measuring and addressing any environmental hazards that might arise. Generally accepted accounting principles for the waste management industry require companies to allocate anticipated future closing costs over the operating life of the corresponding landfill properties as space is consumed. The process for measuring these costs is to project all closing costs estimated to be due in the future, followed by discounting such costs to the current period to estimate the present value of the environmental liability for landfill remediation. The schedule below shows WDI's estimated liability at the end of the current and previous year. WDI Environmental Liabilities for Closure and Post-Closure Costs (in millions) Reclassified gain During 1999, WDI realized a $110 million gain from selling an interest in a business called SM, Inc. In its 1999 unaudited financial statements, the company offset this gain against unrelated operating expenses and adjustments of prior-year estimates. The controller justifies this treatment as an efficient way to avoid cluttering the income statement with a separate line item for the gain on the sale of SM, Inc., given that management does not consider the amount involved to be material to the financial statements taken as a whole, and that the proposed treatment is simply a reclassification, not an increase or decrease in net income. Other observations: - WDI's management owns significant stock in the company from executive stock option awards over the years, and has unexercised options that would become lucrative to exercise only if the WDI stock price increases further. - Both the controller and the chief financial officer of WDI are former members of your audit firm. Your firm has had an excellent working relationship with both of them over the years, and they have hired other auditors from your firm for accounting positions with WDI. - In 1999, WDI secured a new multi-million dollar long-term line of credit to continue its aggressive growth strategy and leverage its operating position. Required: Imagine it is January 2000. In a three-page double-spaced memorandum addressed to "Mark Bradshaw, Partner" (with font and margin restrictions as set forth in the syllabus), summarize the risks you perceive as you contemplate auditing WDI's calendar 1999 financial statements. Be sure to discuss as many risks as you see, i.e., do not simply choose one and devote the entire paper to that risk. Organize your report professionally, as if you were an audit senior assigned to present a planning summary to me, the lead engagement partner for WDI